WEEKLY - stablecoin risks, DeFi friction

plus: assorted links, world photography and more

Hi everyone! The news flow is getting just insane, and we’re not even three months into the year yet…

However, some perspective: yesterday was the vernal equinox, when the sun starts shining more on the Northern Hemisphere than on the South. It’s refreshing to be reminded that, whatever craziness may be going on in our feeds, the earth and the sun will keep on doing their dance.

🌍

If you’re not a subscriber to the premium dailies, I hope you’ll consider becoming one? You’ll get access to market commentary as well as adoption insight and industry trends. Plus, links and music recommendations ‘cos why not…

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

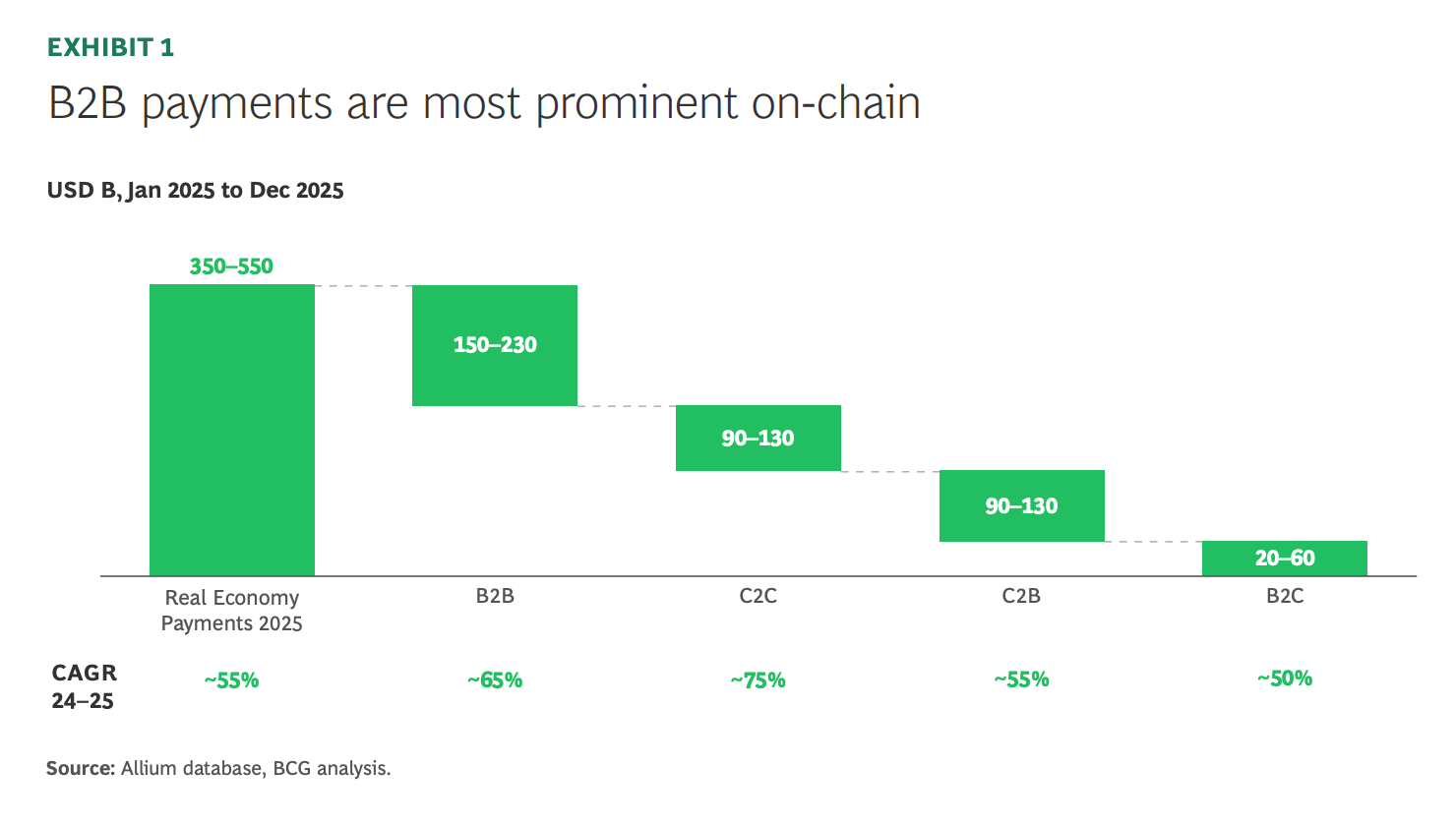

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

In this newsletter:

DeFi: freedom with friction

Overlooked stablecoin risks

Assorted links: The relationship between time and Japanese food, Banksy, AI’s fix for social media, “new” culture, TSA privatization

Weekend: World photography

✨ Use the discount code MACRO for 20% off!

Some of the topics discussed in this week’s premium dailies:

Coming up this week: central banks

Monday mood: conflict complications and crypto

Macro: US inflation, again

Markets: green shoots, but of what?

EU tokenization and wholesale CBDC

Markets: BTC inflows

Macro: inflation data quirks

Overlooked stablecoin risks

Markets: who cares about rates?

The cost of escalation

The Fed’s confusion

Macro: PPI alarms

Markets: hooo boy

DeFi: freedom with friction

Politics and the energy crisis

Markets: the historical view

DeFi: freedom with friction

To what extent should traders be allowed to do what they want with their money?

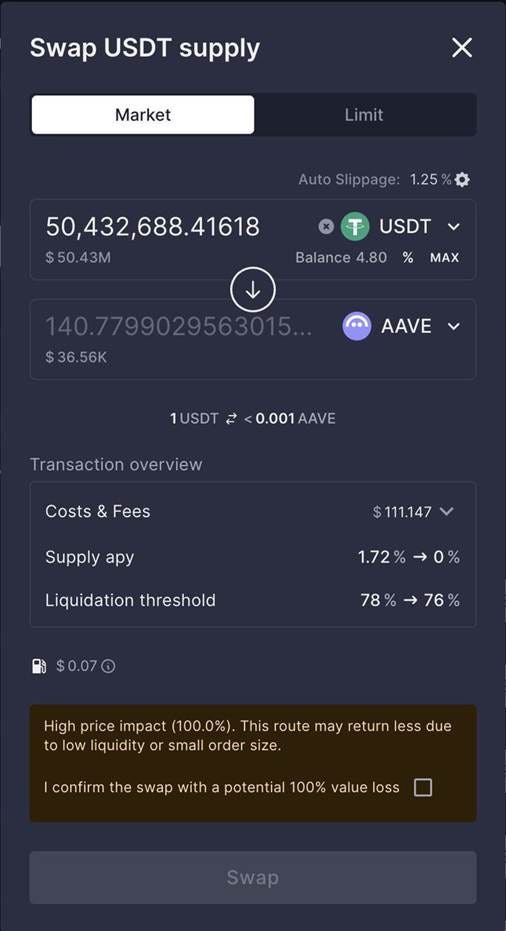

Last week, someone put in a $50 million trade on Aave’s decentralized exchange and ended up with tokens worth around $36,000.

The culprit for the monetary loss was not a mistake; it was apparently due to a lack of liquidity and some confusing engine mechanics. The user wanted to swap aUSDT – a yield-bearing token representing USDT deposited on the Aave platform – for aAAVE, which represents deposited AAVE tokens.

They chose to do so via an integrated front-end for the Aave decentralized engine called CoW Swap, which routes user intents to “solvers” (algorithmic agents or market makers) who find the best quote.

For their ~$50 million in aUSDT tokens, the user was offered aAAVE tokens worth just over $36,200. The front-end issued a warning: “High price impact (99.9%)” and required the user to check a box next to “I confirm the swap with a potential 100% value loss” before proceeding. Inexplicably, the user did that, and the trade was executed.

(image via @aave)

This incident raises the inevitable questions about responsibility. It also highlights a couple of unique and often overlooked features of decentralized finance.

Obviously, this trade was not in the user’s best interest, to say the least. But a controversy is swirling over whether Aave should have blocked it.

Should a bad trade be a decentralized exchange’s responsibility? If so, are we not reconfiguring DeFi to look like TradFi? And if decentralized exchanges have to determine what is a stupid trade or not, what’s to stop that bar shifting over time? We have seen this happen in traditional markets, with risk and potential reward increasingly limited to a select few.

Or, should we let people take responsibility for their financial decisions, however stupid they may be? Obviously, the protective instinct runs deep, especially among regulators. But, throughout history, the evolution of law has been a tussle and a trade-off between protection and freedom.

This is, after all, just a financial trade, and the user would no doubt have found other things to do with their money if this transaction had been blocked – this particular case is not the point. But it highlights our tendency to replicate structures even when given tools to create new ones.

Understandably, we want freedom until we get hurt, then we want protection. And passing on blame not only salves our egos, it also makes regulators happy and lawyers rich. This is something authorities been warning DeFi advocates about for years: don’t come running when things go wrong.

Intriguingly, the affected user is not the one clamouring for a fix here – they haven’t, as far as I know, made themselves public, even though Aave is offering to return the ~$110,000 transaction fee.

So how did we find out?

Public blockchains are transparent. Someone noticed this odd transaction, and word spread.

Were such a weird trade to happen in TradFi, we would only find out if one of the parties to choose to disclose the information. In DeFi, on the other hand, we know almost immediately when something strange happens, and we can dig deeper.

Both Aave and CoW Swap have published post-mortems. Aave focuses on the lack of liquidity, while CoW Swap goes further, pointing to outdated gas limits (which cap onchain transaction fees) that potentially blocked orders that would have slightly reduced the loss, querying why the winning “solver” didn’t use a more optimal transaction sequence, investigating back-filling arbitrage and more. Onchain and in the back-end of the decentralized platforms, there is plenty of data on quotes, routing and execution that can help improve the engine’s performance and user experience.

Also, while a similar trade in TradFi would not be allowed to happen, if by some fluke it did, at least one market participant – probably a market maker – would have to scramble to fill an accounting hole. In this DeFi case, Aave’s engine and its balance sheet were unaffected.

On the flip side, a traditional market participant would probably have broken all sorts of “best interest” rules if it did allow a trade like this to go through. Aave didn’t break any rules, because DeFi is not (yet) regulated. Yet all major DeFi platforms are targeting institutional clients. BlackRock’s BUIDL token is now listed on an adaptation of UniswapX, a decentralized aggregator that scours all platforms (including Uniswap) to fill swap requests. This incident begs the question, however: is DeFi ready for institutions, and are institutions ready for DeFi?

As a result of this incident, Aave is implementing “Aave Shield”, which will block swaps with more than a 25% price impact.

It feels like a good solution. The user could still go ahead with a bad trade by deactivating the shield in their account settings, but the possibility of distracted error is reduced. Maybe “freedom with friction” should become the new ecosystem slogan.

There are still unanswered questions: why did the user do this? Were they drunk? Trying to prevent a position liquidation? Tax loss harvesting? Is it money laundering? Onchain forensics are no doubt already investigating.

But the bigger question has to be: to what extent should users be prevented from bad decisions? And who gets to decide what the boundaries are?

See also:

TradFi embraces DeFi? Not quite. (Feb 2026)

Overlooked stablecoin risks

Earlier this week, I dove into a paper that I’d missed, published last month by the MIT Digital Currency Initiative – “The Hidden Plumbing of Stablecoins Financial and Technological Risks in the GENIUS Act Era”.

It makes some good points about stablecoin risks, which many in the industry dismiss as irrelevant fear-mongering but which have to be taken into account when building an alternative system for global finance.

We’re used to insisting that stablecoins have no risk because they are backed by US Treasuries and related assets, the safest collateral in the world.

But we’re overlooking a bunch of vulnerabilities beyond the control of stablecoin issuers, to do with financial markets and the underlying technology. They may have an extremely low probability of becoming an issue, but they’re not nothing.

Stablecoin reserves have liquidity risk

The GENIUS Act mandates that dollar stablecoins be backed by bank deposits and short-term US Treasuries, which form the backbone of the safest and most liquid capital markets in the world. Given the superior yield of Treasuries over deposits, the bulk of stablecoin reserves are likely to be linked to these securities. The thing is, these settle T+1, which could be an issue in the event of mass stablecoin redemptions.

Bank deposits are more liquid in that they can be distributed immediately in normal conditions – but not if the bank is having solvency issues. Even if the relevant deposits are insured, disbursement in times of stress can be delayed. And the GENIUS Act does not mandate that all bank deposits held as stablecoin reserves be insured (the FDIC covers up to $250,000 per account).

Also, broker-dealers have limits on how many treasuries they can buy in a given time period. If a broker-dealer reaches this limit, perhaps for reasons unrelated to stablecoin demand, issuers may struggle to sell the necessary amount of reserve assets at par, which in turn could exacerbate redemption demand.

What’s more, the Treasury market is not immune from liquidity issues – episodes of market stress can be triggered by a spike in funding needs, a drain of bank reserves or a combination of factors that impede dealers’ ability to buy or sell government securities. A large stablecoin market spooked by issues in the secondary market for Treasuries could lead to a run which would exacerbate Treasury market dysfunction. Were this to happen, presumably the Fed or the US Treasury would step in – but at the cost of global confidence in US government securities.

Stablecoins have technical risk

Beyond reserve risk, stablecoins that run on public blockchains carry a range of technology-related vulnerabilities.

For one, smart contracts can have bugs in the code. These can be present at launch or introduced in upgrades, and can lead to a mismatch between issuer assets and liabilities, broken payment chains, frozen funds and other serious complications.

What’s more, if upgrade credentials become known, smart contracts could also be hacked, leading a loss of confidence and/or funds, triggering a run.

Bridges are another point of vulnerability – these are smart contracts that help stablecoins switch from one blockchain to another. If they do so by burning stablecoins on one blockchain and minting them on another, errors could lead to balance sheet mismatches as well as lost or frozen funds. If they do so by locking up tokens, they could be subject to hacks and theft.

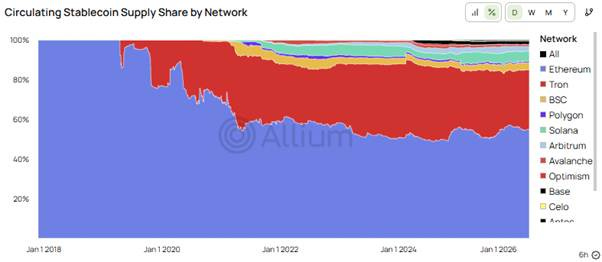

On proof-of-stake (PoS) blockchains such as Ethereum (on which more than half of circulating stablecoin supply runs), validators – the nodes that maintain network consensus – work with block builders who have discretion in ordering transactions, and both earn additional income through prioritization fees. This can affect predictability and transaction costs for users in normal times, and in times of stress could even weaken stablecoin liquidity as some types of transactions get “crowded out”.

(chart via Allium)

Another factor potentially impacting transaction cost and timing is network congestion, which could be the result of an attack via spam transactions or a speculative frenzy leading to a flurry of onchain transfers. Even doubts about a stablecoin’s utility during such times could lead to a run, amplifying the congestion.

Also, there’s some ambiguity around settlement finality, which determines when a trade is complete. In traditional finance, this is a legal and operational concept, determined by governance. On a public blockchain, settlement finality is determined by the underlying code, which could lead to inefficient confusion.

Finally, in traditional finance, responsibilities are clearly defined. With public blockchains, however, operational responsibility is diffuse – who should intervene if something goes wrong, and is that even possible?

--

The paper contains other insights not related to risks but that are nevertheless worth considering (such as whether stablecoin issuers can “capture” public blockchain governance, how stablecoin issuers differ from banks even though both take deposits, and more). The key takeaway, though, is that stablecoins may offer many improvements on traditional money rails, but there are some trade-offs.

In sum, there’s a lot of work to do yet in stablecoin education, especially in convincing large institutions that the risks, however remote, are offset by the benefits – for most, that’s not so obvious just yet. Banks are not helping with their misdirection of fearful attention to threats that aren’t threats (deposit flight, for instance), confusing the issue and weakening their own credibility. So, it will have to be up to stablecoin issuers to work with market regulators on the necessary reassurances and potential fixes. After all, money needs to flow smoothly, and while there are plenty of risks in the current system, at least they’re risks most users are familiar with and can provision for.

See also:

Stablecoin rewards and bank deceit (Mar 2026)

ASSORTED LINKS

(A selection of reads I came across this week that I think are worth sharing, not always about crypto or macro. I try to choose links without a paywall, but when I feel it’s worth making an exception, I specify.)

Sinéad O’Sullivan takes us down a winding exploration of food’s relationship with time. In Japan this is the default, offsetting the monotony of abundance, which is incompatible with the Western method of rating gastronomy (Michelin = consistency/monotony). Plus, how the Japanese diner and counter concept disintermediates the Western restaurant hierarchy, putting production and consumption in close proximity. And more mindbending ideas besides on how our relationship with food affects our perception of time, and vice versa. (Trickle-Down Gastronomy: Japan, But This Time It’s Different)

An exhaustive (and long) report of the Reuters investigation into the identity of street artist Banksy, with compelling evidence and surprising twists. Good journalism. (In Search of Banksy, by Simon Gardner, James Pearson and Blake Morrison)

In an unusually optimistic take, Noah Smith suggests that AI could restore a semblance of sanity to social media. It’s not just hypothesis: he cites research that shows AI fact checking is having an impact on public perception, cooling tempers while educating. (Save us, Digital Cronkite!, Noahpinion)

In what feels like a plea as well as a prediction, Ted Gioia insists that we’re due for a cultural renaissance as more and more of us reject the common denominator “reboot” entertainment available all around us, and actively seek out the “human”, the unique, the new. (The Shock of the Old, The Honest Broker)

As TSA service collapses around the US, leading to missed flights and airport chaos, Trey Dimsdale makes some cogent arguments for privatizing airport security, including a greater incentive for efficiency-seeking innovation, greater accountability, greater insulation from political fights. (Abolish the TSA and Privatize Airport Security Now, Restoring the West)

If you find Crypto is Macro Now at all useful, would you mind hitting the like button down below? ❤ I’m told it feeds the almighty algorithm.

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

It’s been a while since I saw a photography contest that I wanted to share, and I’ve missed the glimpses strong images give you into other worlds, other feelings – but that changed this week when I came across the World Photography Organization’s shortlist for the Sony World Photography Awards 2026. So much to see.

Here are some of my favourites:

by André Tezza

by Rob Van Thienen

by Jubair Ahmed Arnob

by Kyaw Zayar Lin

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.