WEEKLY - anti-crypto sentiment + a public company token

also: a zany music contest, and more

Hello everyone! I hope you’re all taking care of yourselves. I’ve had a glorious San Isidro weekend so far (see yesterday’s newsletter for explanation) – folkloric dances, ceramics fairs, vintage car parades and a general wandering around in this glorious city.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

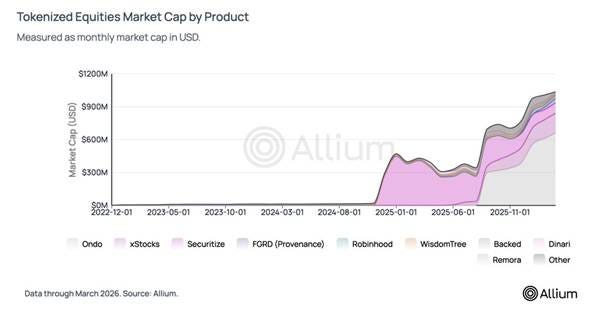

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

In this newsletter:

Why so many hate crypto and why it matters now

A public company issues a token

Weekend: Eurovision

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

Some of the topics discussed in this week’s premium dailies:

Coming up this week: macro data, political moves

Monday mood: Why so many hate crypto and why it matters now

Term of the day: PAC

Macro: the US job market is fine

Macro: US consumer sentiment isn’t

Happiness is in free-fall: why, and what does it mean for markets?

The CLARITY markup: what to watch for

Macro: US inflation warming up

Markets: building steam

Macro: a tightening jobs market

Term of the day I: Trimmed mean

Term of the day II: Sticky inflation

A public company issues a token

Macro: the US PPI shock

Markets: dissonance

Term of the day: PPI

Why does Madrid celebrate San Isidro?

Why so many hate crypto and why it matters now

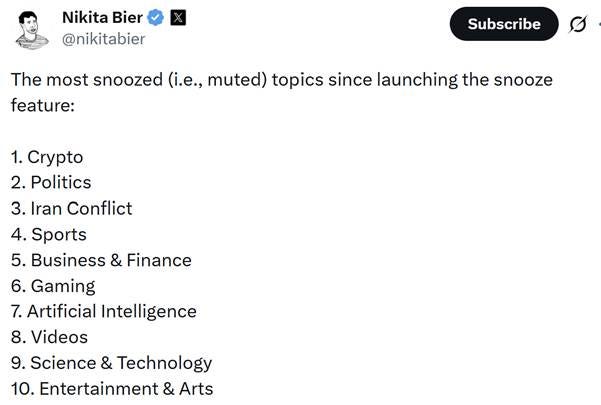

A few weeks ago, X enabled the ability to mute certain topics so related posts wouldn’t show up in our algorithmically generated “For You” feeds.

Nikita Bier, the platform’s Head of Product, recently revealed the most muted topics. The number one spot? Crypto.

(post by @nikitabier on April 30, 2026)

This was a surprise given how long “crypto Twitter” has been a thing, a place for those of us interested in learning more to share ideas and meet like-minded people (sorry, “crypto X” just doesn’t have the same ring to it). We thought we were a meaningful feature of the platform. We even have an established acronym, CT.

Now we have evidence that mainstream X doesn’t like us.

Why is crypto so hated? I have some theories.

On X, it’s easy to blame the unhinged and/or mercenary individuals (and their bots) that flood feeds and comments with ridiculous claims that such and such a token you’ve probably never heard of before is “the future”, “inevitable”, “going to make you rich”. The obvious grift, the embarrassing scams, the painful exploits add to the overall image of crypto being overrun by a cesspool of manipulators.

Even if you were initially intrigued or enchanted by the promise of decentralization, eventually the “ick factor” can wear you down. It would be understandable (while regrettable) if you decided that learning any more about the potential was just not worth your time. Where’s that mute button…

But we can’t just blame the community. We have to dispassionately accept that the technology itself bears some of the responsibility here.

To start with, we have to ask ourselves why crypto attracts so many shady characters and immature manipulators.

Largely, it’s because of the equality of opportunity it offers. On a blockchain, anyone can issue a token and there are as yet, in most jurisdictions, no rules about the disclosures and promises. What’s more, anyone can buy a token, and open access is a candy store for grifters dangling the allure of easy money.

Put differently, the decentralization and efficiency of blockchain-based assets attracts those looking to disintermediate the established system for the sake of fairer access, as well as those that would otherwise be stopped by it for the sake of common sense and investor protection. Crypto attracts plenty of good but also plenty of bad, because of its relative freedom.

Also, there’s the technology itself, what it stands for. It’s a myth that all technology is neutral. Anything created or designed with a purpose in mind has an intent, an “affordance” – the potential action a technology or a device allows a user to perform. Intents are inherently political, and the original design purpose matters even if it evolves radically over time.

And any technology that enables progress also enables darker effects. A lamp lights a room – it also attracts a lot of moths and other insects. A gun can protect a family, and it can kill innocent people. A mobile phone enables both easier communication and more pervasive surveillance. Intents may be noble, but affordances can get hijacked.

And with blockchain technology, not everyone thinks the intent was noble.

Bitcoin, the original blockchain, was created to disintermediate centralized financial control. That’s pretty darn political, and goes some way towards explaining why even smart individuals such as the late Charlie Munger of Berkshire Hathaway called Bitcoin “rat poison”. He was not active on X and therefore not exposed to its seamy side, but he hated the idea of the citadel walls being breached. For someone raised within them, Bitcoin was more than a threat, it was an insult.

In sum, it’s not just the crypto community that mainstream X users reject, even though that may be the trigger. It’s also the technology that attracts that community – and, for many, the uncomfortable disruption that the technology enables.

So, why is this especially relevant now?

In part, it’s because it represents the endurance of resistance to change – with crypto embraced in the highest office in the country with the world’s largest capital markets, it is still not popular, which should trigger some introspection.

But it’s especially significant because of where we are in the political cycle. The timing matters for the industry’s future, with contentious crypto regulation on the table.

Politico published the results of a poll last week highlighting American distrust of crypto.

Now, much of this may be Politico’s particular slant. According to the survey, 45% of Americans say investing in crypto is not worth the risk – this is presented in a triumphant tone, overlooking that the bigger takeaway is that a 55% majority either do think it’s worth it, or don’t have anything against the idea.

Also, according to the poll, nearly half of Americans trust a bank to hold their money more than a crypto platform – I’m stunned it’s not much more, given that US crypto platforms are centralized entities without anything like the federal oversight or guarantees banks have. Even should the CLARITY Act pass, giving crypto platforms a broad legal framework, banks are safer.

Politico argues that this obvious lack of trust (a question of perspective, but anyway) spells danger for politicians that accept money from crypto PACs. Then again, it also acknowledges that only 3% have heard of Fairshake, the largest crypto PAC. Almost a third of respondents think that the oil and gas industry is the largest spender on political influence – it lost that role to crypto and AI a while ago. I see more a lack of interest than a lack of trust.

For now, the idea of giving the crypto industry a regulatory framework has support from senators on both sides of the ideological divide. But, with midterm elections looming, voter sentiment matters even more than usual.

Could senators be thinking about a potential backlash at the polling booth? Or would they be more concerned about PAC influence? We can hope they would take the march of innovation into account and focus on support for clean markets that discourage grift while allowing new types of products to reach a broader range of investors.

I know, politics is politics, but we can hope.

✨ If you find this newsletter interesting or useful, would you mind sharing with friends and colleagues and nudging them to subscribe? I’d appreciate it! ✨

A public company issues a token

Earlier this week, Circle announced a $222 million pre-sale for ARC, the token that will power the firm’s Arc layer-1 blockchain. Allocations went to a who’s-who of tradfi investors: a16z, BlackRock, Apollo Funds, Intercontinental Exchange, Haun Ventures, Standard Chartered Ventures, Japan’s SBI Group and others.

Note that this is a pre-sale in which investors commit funds ahead of token launch – as far as I know, a date has not yet been set for that but it is expected sometime this summer.

I’m not going to get into the ARC tokenomics today (here’s a link to the whitepaper if you’re interested) but in brief: once the Arc blockchain moves to Proof-of-Stake in 2028, the value accrual will mainly stem from validator and staker rewards plus token burns funded by transaction fees, similar to how Ethereum works today.

Meanwhile, the pre-sale puts the total fully diluted valuation of the token’s 10 billion initial supply at $3 billion, or roughly 10% of the parent’s roughly $31 billion market valuation.

Here’s where it gets even more interesting.

As far as I know, this is the first time we’re seeing a major public company issue a token. So, it’s also the first time we’ll be able to see a market valuation for a component of a business that has a market valuation.

For now, the bulk of Circle’s revenue comes from stablecoin issuance, a profitable business with short-term treasury yields above 3.5%. But many analysts have been bearish on Circle’s stablecoin revenue outlook given the likelihood of declining T-bill yields in the face of US rate cuts – for them, the Arc payments network represents diversification of revenue, cushioning Circle’s interest rate sensitivity.

With rate cuts pretty much off the table for this year, there is still a strong case to be made for diversification. Circle moves from being a stablecoin issuer to a payments platform operator, from manager of a product to manager of an infrastructure layer, a very different business but targeting the same market. And, we get to track market expectations of each segment – this is new.

Beyond the fascinating valuation-within-a-valuation, we also will be able to follow public pricing of a stablecoin payment network. As yet there are few, if any, opportunities for investors to participate in such a network’s growth. There have been occasional rumblings about Stripe’s Tempo issuing a token, but so far no substantial rumours.

It’s also a bet on agentic commerce, as Arc is being built to allow AI agents to transact with each other.

Another fascinating twist is the number of heavy tradfi firms that are investing in a token. None of them are strangers to the blockchain world, but it does feel like a starting gun for broad institutional acceptance of the concept of taking stakes in token projects, especially those with institutional utility.

And we get to see the impact this could have on Arc’s competitive advantage. When large institutions have a financial incentive linked to transaction volumes on a platform, they’re more likely to help deliver those transaction volumes. Put differently, ARC holders benefit both from the service, and the service’s economics. This embodies one of the key selling points of native token issuance for onchain applications – those that use the platform get to directly benefit from its success – only, this is happening within a publicly listed company with other revenue sources.

In sum, the ARC token will be a fascinating example of the monetization and valuation potential for onchain business segments for a wide range of companies, both traditional and new. It is for sure more institutional than the initial ICO excitement of a few years ago, but it’s also an intriguing transformation of how companies can fund new projects while incentivizing their use.

If you find Crypto is Macro Now useful, would you mind hitting the like button? ❤ I’m told it feeds the almighty algorithm.

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

It’s the Eurovision Song Contest this weekend, a big deal for those of us on this continent and a spectacle that defies description, it really has to be seen to be believed. There are few occasions in a year when you can get together with friends and, in roughly equal doses, both jump around and cringe, often at the same time.

I’ve watched clips of the entries and am reassured that we will get the expected inconceivable amounts of zaniness with some good tunes and spectacular outfits thrown in to trigger heated debate, and what seems like more violins than usual for some reason. There is music that would have been at home in the past century, plenty that seems to come from the next, and the show apparently opens with an artist called Satoshi from Moldova singing a song about Moldova. I am excited, and am rooting for Croatia which almost certainly means it will do terribly. Although the Portuguese entry is inexplicably growing on me. Albania brings serious “wtf??” game. Finland is the favourite to win, according to Polymarket – bewildering.

The event is known as the Eurovision Song Contest, but the term “Euro” is given some creative liberty. There’s an entry from Australia which is one of the favourites to win, which could cause some confusion. There’s also an entry from Israel, which is why Spain is boycotting this year, not even allowing the event to be shown on TV – don’t get me started on the paternalism and hypocrisy. It’s fine to buy Israel’s chemicals and machinery, and sell it our fashion and cars, but we can’t be seen to be enjoying ourselves in a musical extravaganza with the country’s representatives. Fortunately, we have YouTube.

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.