WEEKLY - geopolitics + blockchain, central banks + stablecoins

What do blockchain use cases have to do with geopolitics? Why does the ECB disapprove of stablecoins? plus: assorted links, outrageous fashion and more

Hello everyone! I hope you’re enjoying some blue skies wherever you are – we sadly have rain here in Madrid which goes to prove that, contrary to what I was told, the rain in Spain does NOT stay mainly on the plain.

📽 Yesterday, I had a wonderful chat with John “Alyosha” Johnston, author of the excellent Market Vibes newsletter, on newslettering – you can see the playback here. 📽 “Press Publish” will be taking a break next Friday as it’s a holiday where I live, but you can see previous sessions here. 😊

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

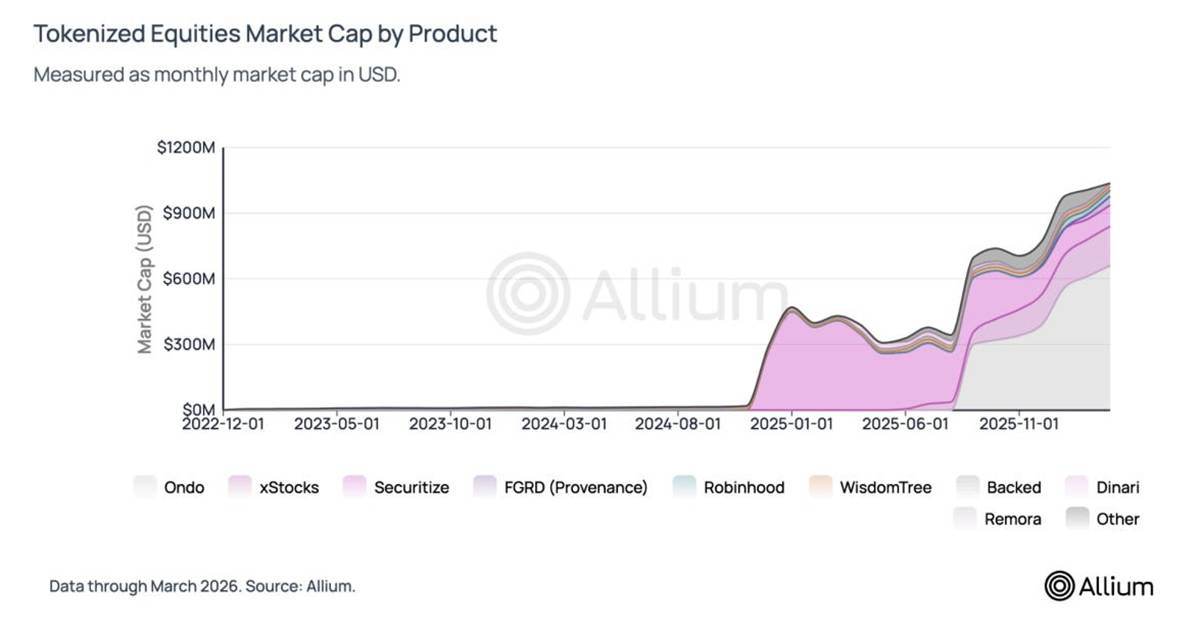

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

In this newsletter:

The geopolitics of blockchain use cases

ECB: stablecoins bad, CBDCs good

Assorted links: technology bias, Twister, universe expansion, making friends, metaphors, music criticism

Weekend: “fashion as art”

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

Some of the topics discussed in this week’s premium dailies:

Coming up this week: US jobs, PMIs and Fedspeak

Monday mood: The geopolitics of blockchain use cases

Markets: what does “help” mean?

The outlook for US sanctions

Term of the day: Teapot refinery

Brazil’s stablecoin separation

Market: maybe momentum

Term of the day: 25-delta skew

The CLARITY Act inches forward

The bigger picture of meme coin lawsuits

Macro: the US jobs market looks resilient

Markets: a peace rally?

Term of the day: backwardation

The overlooked stablecoin pushback

Markets: AI enthusiasm meets a hope for peace

Macro: a jobs boost

ECB: stablecoins bad, CBDCs good

Markets: distortion

Macro: inflation expectations

Term of the day: Desalination

The geopolitics of blockchain use cases

Financial markets, or industry – what plays a greater role in civilizational strength?

Unfortunately, “both” is not a realistic answer as resources require allocation and long-term strategy requires focus.

This question has never been more relevant than now, with shifting geopolitical plates, maturing economies and the rapid expansion of new technologies altering the resource balance. You’ll have noticed the gradually increasing heat of the headlines that march across your attention span – these are the window dressing for the building rumble of a more fundamental tension between two superpowers employing radically different approaches to win influence and resilience.

Of course, I’m talking about the US and China. That they are both large and powerful is without doubt. What can be debated is how their relative strengths will influence the competition ahead.

The US dominates financial markets; China wins on industrial heft. The US is home to the world’s largest financial markets; China is the world’s largest exporter of goods. The US is the world’s largest economy in terms of GDP; China has one of the highest GDP growth rates.

This is the result of conscious choices over the decades: the US cultivated the use of the dollar in global trade settlement which in turn fed liquidity on its capital markets while clear rules supported investor confidence and boosted funding activity. China chose to leverage its considerable labour and natural resources to industrialize, with centralized control turbo-charging the speed and spread of growth.

Now, each is eyeing the other’s competitive strength. The US wants to boost its industrial activity, while China wants to strengthen its financial markets. The US is trying to weaken its reliance on Chinese imports; China wants to move away from depending on dollar networks.

You get the picture. Of course, there’s a crypto-related twist.

Over the past decade, new technologies have marched onto the battlefield for tomorrow’s influence. The US is leading for now in terms of artificial intelligence and chips, but China is catching up fast while charging ahead in robotics and electrification. Both are throwing a lot of money at development, with China drawing on state funding and direction while the US relies more on private markets.

In blockchain applications, the divide between the US and Chinese focus is stark, and cleaves almost perfectly to their relative economic strengths.

Ask an informed American what key uses they see for blockchain technology, and they’ll almost certainly talk about stablecoins, tokenization, new types of derivatives, perhaps even prediction markets – blockchains are for financial markets and facilitating global use of the dollar.

Ask an informed Chinese person, and they’ll bring up industrial uses: distributed databases, supply chain tracking and the like – blockchains are for information efficiency and strengthening corporate cooperation.

While there seems to be a race in the development of AI models, new chip technology, satellite mechanics and more, in blockchain there’s little competition as the US and China are taking radically different approaches to the technology’s application.

Last year, the US passed legislation for stablecoins, and this year just might (maybe, possibly, hopefully) get a legal framework for crypto asset markets. In China, blockchain was named as an official industrial priority as far back as 2018, and by some accounts even earlier.

In the US, blockchain development is left up to the private sector. In 2020, China unveiled a national blockchain.

While US financial giants are dipping their large toes into tokenization of funds and other assets, China is actively discouraging that type of application, directing businesses and regional governments to focus on supply chain tracing, trade finance documentation, data distribution, public services, agriculture financing and more.

In sum, in the US, blockchain means markets, speculation and the transfer of value. In China, it’s associated with industrial development and logistics.

Will this divide last? Or will we see blockchain applications in each region mirror their respective directional shifts?

Put differently, will blockchain technology in the US find applications in industry, and will China increasingly turn to onchain finance?

There have been some isolated instances of Chinese onchain debt issuance – but these have felt more like pilots for CBDC settlement. And China’s digital yuan is part of the push to internationalize the yuan – but it doesn’t run on a blockchain. So, while we are likely to see more onchain financial use cases in China, capital markets will not be the priority.

The US is in a similar situation. There are instances of industrial use, but still isolated for now. Leveraging the efficiencies of blockchain technology generally requires sector-wide coordination. This is a tall order when competition is in the DNA of not just business structures but also the executives that run them. Give up control of data and logistics relationships? Unlikely.

Companies in a state-controlled economy, on the other hand, will be eager to follow official recommendations, especially when wrapped in national interest language. So, we could see some brave US startups and efficiency-seeking corporates experiment with industrial applications – but in the land of finance, capital markets and currency adoption will continue to be the priority.

This strategic fork matters for two key areas of the technological competition that lies ahead: robotics and AI.

Which blockchain strategy will have the advantage? Will dominance in industrial blockchain applications widen China’s robotics edge? Will the US advantage in fintech innovation give an onchain boost to agentic transactions? Where robotics and the agentic economy meet, who will have the upper hand?

Of course, it’s too soon to tell – but a clue lies in the breadth and depth to which blockchain use cases embed themselves in industrial and technology systems in coming years.

ECB: stablecoins bad, CBDCs good

Yesterday, ECB Chief Christine Lagarde gave a speech about stablecoins. Unsurprisingly, she painted them as much riskier for the European economy than the digital euro CBDC her institution is so enthusiastically promoting.

She recognizes that stablecoins have efficiency benefits, but stresses that there are tradeoffs:

There’s the financial stability risk via a failure cascade – should problems at one bank, for instance, weaken confidence in a stablecoin’s backing, a wave of redemptions could accelerate destabilization.

(I’ll add that this is a key weakness in the MiCA regulation, which insists that stablecoin reserves be at least partly held as bank deposits – banks are not as “safe” as government debt, but the EU does not yet have a deep and liquid government debt market. I’ll also suggest that stablecoins could end up smoothing any banking crisis as an alternative transaction mechanism when everything else is freezing up.)

There’s also the inevitable weakening of monetary policy and therefore the ECB’s ability to maintain price stability. If funds migrate to stablecoins, banks will lend less and the passthrough from official interest rates to the economy weakens.

(Lagarde paints as a given an outcome based on the flimsy assumption that stablecoin reserves won’t find their way back into banks, either directly as part of reserves or indirectly as deposits from those selling the reserve securities.)

These tradeoffs, she argues, are not compensated by the short-term gain of better payments and a potentially broader euro reach. The risks outweigh the benefits:

“If we want to strengthen the international appeal of the euro, stablecoins are not an efficient way of doing so.”

The problem, she suggests, isn’t the underlying technology – that is “genuinely transformative”. No, the problem is the involvement of the private sector.

Put simply, only central bank money can be trusted – and therefore, the digital euro checks all the benefit boxes of private stablecoins, without the risk. (Actually, no it doesn’t – stablecoins come with network effects that the digital euro won’t necessarily have, such as participation in DeFi and other yield generating applications.)

The ECB chief’s remarks come as the European stablecoin consortium Qivalis grows to 25 members and continues to make progress towards launch later this year (for more on this, see this excellent report in Blockstories.)

Now these banks are told by their key regulator “I don’t like what you’re doing”, as the regulator sets up a direct competitor to the banks it is tasked with overseeing. It’s not just the push for a CBDC as an alternative to stablecoin digital money; it’s also the issuance of ECB wallets to the retail sector, with no thoughtful debate on whether a central bank should be directly interacting with individuals. And there’s the uncontested assumption that public institutions are better stewards of financial innovation than private entities, so the latter should be discouraged.

This is especially jarring given signs that Lagarde does not understand stablecoins.

Early on in the speech, she falls into a tempting misconception laced with condescension. She says:

“To make a specific type of crypto-asset usable for settlement, the creators of stablecoins anchored them mainly to fiat money, the very system they had originally sought to bypass.”

Here she is lumping all crypto entrepreneurs into the Satoshi Nakamoto bucket, which either displays a wilful ignorance, or a deliberate use of language to imply failure and compromise. Stablecoin creators never “sought to bypass” fiat, their objective was to link the fiat and crypto worlds, and arguably they have succeeded. Obviously, Lagarde is unhappy about that.

Lagarde’s depressing conclusion distils down to this closing remark:

“Our task is not to replicate instruments developed elsewhere, but to build the foundations and the infrastructure that serve our own objectives, so that we can harness the benefits of innovation without importing the fragilities.”

It continues to astonish me that report after report, statistic after statistic conclude that Europe is too conservative when it comes to innovation and development, and yet these loud signals continue to be ignored even as the bloc’s economy loses more talent and funding.

It begs the alarming question of what would stem the trend? What would weaken the bloc’s collective conviction that only increasingly centralized power can ward off risk?

Unfortunately, the usual trigger for a radical change in mindset is a crisis. No one wants that. But until the mindset changes, Europe is increasingly likely to get one.

See more:

EU tokenization and wholesale CBDC (March 2026)

Digital euro politics (Feb 2026)

Digital euro deadlines (Jan 2026)

From Blockstories - Exclusive: Qivalis Gains Momentum with 25 Additional Banks Set to Join (May 2026)

Speech by Christine Lagarde: Stablecoins and the future of money: separating functions from instruments (May 2026)

ASSORTED LINKS

(A selection of reads I came across this week that I think are worth sharing, not about crypto nor macro. I try to choose links without a paywall, but when I feel it’s worth making an exception, I specify.)

A fascinating article about the design of devices, the elusive neutrality of technology, the threat of predictions and the slippery motivations of surveillance. (The eye in your pocket, Aeon)

You’ve played Twister, right? It’s put you in embarrassing situations, right? That can lead to much mirth, right? Here’s a fascinating of the history of the game. (How the Classic American Game of Twister Went From Risqué to Record-Breaking, Smithsonian Magazine)

So, this is wild – the universe is expanding faster than existing models think it should. (Scientists have finally figured out how fast the universe is expanding, WSJ via MSN so no paywall)

I oddly love this data-focused approach to making friends – huge respect for having a goal and finding a way. (Talking to 35 Strangers at the Gym, Thienan Tran – h/t Alphaville)

If you ever feel like going swimming in a sea of metaphors, this is the article for you. (Comparisons as Predictable as the Sunrise, The Pudding)

Thoughts from Ted Gioia on music criticism – the role of feelings, the value of empathy, the importance of study and more. This made me want to rush out and get some books on music appreciation, I feel like I have so much to learn. (My 9 Rules of Criticism, The Honest Broker – paywall)

If you find Crypto is Macro Now useful, would you mind hitting the like button? ❤ I’m told it feeds the almighty algorithm.

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

I used to turn my intellectual nose up at the Met Gala until I realized that fashion is not just signalling, not just personal expression, it’s also art. This year’s theme “Fashion is Art” sure lived up to that and produced some truly breath-taking and also eyebrow-raising confections – sculptures, shapes, sparkles and bucketfuls of fantasy draped on beautiful people in a rarefied setting. Stuff the party, the photo parade is the whole point.

Anyway, in case you missed the spectacle, here are some key examples – love ‘em, hate ‘em, we can’t say they’re not creative.

All of the below are taken from this complete pictorial coverage by Reuters:

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.