WEEKLY – manipulation, Sony’s blockchain

Plus: assorted links, Spanish music and more

Hello everyone! I hope you’re all doing well, and enjoying a summery change of pace.

You’re reading the free weekly send of the premium daily Crypto is Macro Now, where I re-share a couple of the week’s posts and add some non-crypto and non-macro links since it’s the weekend. 🌼

If you’re not a subscriber to the premium daily, I do hope you’ll consider becoming one! For $12/month, you’ll get ~daily commentary on how crypto is impacting the macro landscape, and vice versa. I talk about adoption, regulation, tokenization, stablecoins, CBDCs, market infrastructure shifts and more, as well as the economy and investment narratives.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

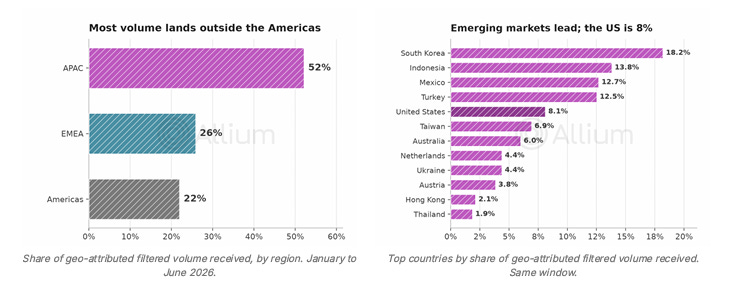

Where are stablecoins most used?

Allium filters stablecoin volumes for non-economic actions such as inter-group transfers – it turns out that most is outside the US, with 52% in Asia-Pacific and 26% in Europe, the Middle East and Africa.

The leading destinations are South Korea, Indonesia, Mexico and Turkey, places with currency pressure, active remittance corridors, or both.

→ For more, download Allium’s State of Onchain Finance report: https://allium.so/reports/state-of-onchain-finance-q2-26

In this newsletter:

Manipulation and the Chat Control lever

Sony’s stablecoin: the bigger implications

Assorted links: Liberalism, Brand Scotland, epic orality, AI and the tax base,

Weekend: the music of Spain – send good vibes to New York, please

Podcasts

If you missed this week’s livestream, you can catch it here:

Monetary Forces, with Izabella Kaminska – we discussed SWIFT, Sony, monetary aggregates and how stablecoins impact the money supply.

COMING UP:

✨ Monetary Forces: come join us next Tuesday, when Izabella Kaminska and I pick at the key headlines that paint the picture of how technology is changing finance.

👉 Tuesday, July 21 @ 10am EST / 4pm CEST / 3pm BST – livestream link: https://open.substack.com/live-stream/284760

Some of the topics discussed in this week’s premium dailies:

Coming up this week: US macro, Fed speeches

Monday musings: manipulation and the Chat Control lever

Term of the day: Directive vs regulation

Sony’s stablecoin: the bigger implications

Term of the day: De novo entity

Markets: yikes

How stablecoins create money

Macro: CPI cooling

Why DTCC’s tokenization test matters

Term of the day: DTCC

Markets: over-confidence again

Visa’s stablecoin platform: more of the same?

Markets: ominous rumblings

Podcast recommendations

Manipulation and the Chat Control lever

Social media manipulation can come from unexpected directions.

I’ve been writing quite a bit recently about alarming examples of government trespass, as it is a meaningful part of my “why crypto matters” thesis. But it’s not the only one, and I’m now concerned that our sensitivity to threats is itself becoming a veil. Put differently, seeing monsters around every corner could blind us to the ones that are really there.

So, I’m going to write about government trespass yet again, but from a “not what it seems” angle. Bear with me.

The measure that triggered this line of thought is a temporary exemption to European privacy laws known as Chat Control 1.0, which allows platform providers to voluntarily scan messages for signs of child sexual abuse material (CSAM). It expired in April, but last week the European Parliament held a distorted vote to reactivate it until April 2028. Even though the majority of MEPs voted against the reactivation, it was approved. There’s a lot of nuance here, which I’ll explain below.

It’ll come as no surprise that I follow many accounts focused on protecting freedom of speech and digital privacy, so as I’m sure you can imagine, my feed was furious.

But there’s a whiff of manipulation there. The frustration is justified, the concern is real – but the “democracy is dead” accusations of government shenanigans to push through an unpopular measure feel designed to trigger our emotions and make us feel under attack, rather than keep us informed of the bigger fight at hand.

You’re probably wondering what MEPs have against suppressing the distribution of CSAM, and you’re probably wondering how the European Parliament can move forward with a measure most of its members voted against. It’s complex. And it’s important.

Some background:

In 2002, the EU adopted the ePrivacy directive (on Monday I shared an explanation of EU institutions and terminology). This protects the content of emails, messages and calls from interception or surveillance, with exceptions for law enforcement. It requires user consent or anonymization for the processing of metadata. It (unsuccessfully!) bans unsolicited spam. And, yes, it’s responsible for those annoying “Accept cookie” windows that plague our online existence. But at least it officially recognized our right to define our own online domains.

In 2021, the EU adopted a temporary exemption to the directive. This exemption is known as Chat Control 1.0, and it allows tech platforms to voluntarily detect, report, and remove known CSAM in private messages.

In 2022, European Commission proposed a permanent exemption: Chat Control 2.0. More on this below, but suffice to say for now that it’s controversial, which is one reason it has progressed so slowly through the convoluted legislative process. After five rounds of negotiation between the European Parliament and the Council with the Commission mediating, there is no sign of the parties being even close to an agreement.

The Commission had proposed extending the temporary exemption, but in March, the European Parliament rejected this idea. The temporary exemption expired in April.

Then, on July 2nd, the Council voted in favour of the extension – essentially, one of the EU’s two legislative bodies said yes while the other had said no. This means the proposal goes back to Parliament for what is known as a “second reading”, which triggers another vote but under different rules.

On Tuesday of last week, the European Parliament voted to apply the “Urgent Procedure” to the proposal. This fast-tracks the vote, bypassing normal debate time and committee scrutiny.

The proposal vote took place two days later. It was again split, with 314 voting to reject the extension, 276 voting in favour and 17 abstaining. Under normal circumstances, the proposal would be blocked. But second reading rules require a minimum of 361 votes to reject – although the proposal is still more opposed than supported, it goes through, because not enough rejected.

Many are reasonably screaming that this makes little sense in a democracy – they’re right, but the rules are the rules and they were not broken here. The second reading requirement of an absolute majority to oppose (rather than a simple majority) was designed to unblock impasses and force a compromise – a not unreasonable goal, even if we can disagree with how it’s achieved.

Where the “foul play” cries get loudest, however, is around the timing. Last week was the last full parliamentary session before the summer recess, and 113 MEPs were absent (over 15%, a problem to discuss another day). The accusations suggest that the rush was a deliberate strategy to make sure fewer MEPs were available to register their opposition.

This feels hollow. It’s more likely the urgency has another explanation – those concerned about the distribution of CSAM wanted scanning allowed again before the summer break.

So, despite the horrified reaction from many, nothing untoward happened last week, democracy is still intact, and digital privacy is still available for those who use end-to-end encryption (exempted from the exemption) – and, hopefully, some evil people will have their names forwarded to the relevant authorities.

But…

A bigger concern is that a similar manoeuvre will one day force through Chat Control 2.0.

The current version of the new proposal would not only make the exemption permanent, it would remove the “voluntary” aspect. Platform providers would be required to scan and provide regular assessments, despite an absence of any proven efficacy. According to reported European Commission figures, Chat Control 1.0 provided just over a third of abuse reports in 2024. German police found that roughly 50% of alerts were not relevant while 40% of investigations targeted minors.

We can all agree that the availability of CSAM online is horrific, and those responsible should be punished to the maximum extent allowed by law, at the very least. But those of us familiar with banking regulation know how the pursuit of crime can erode liberties when taken to extreme, liberties we don’t get back even though the crime is not suppressed. The relatively high error rates promise to make life miserable for innocent people. And the easy availability of mass surveillance as a crime prevention tool prevents exploration of more targeted approaches.

It gets worse: Chat Control 2.0 proposes a way around encryption by allowing client-side scanning – messages and other content are scanned on users’ devices before they are sent. It’s not hard to see how, once allowed, the scope could be expanded to include certain types of speech. And this is even before we think about the security risks.

Mercifully, opposition to Chat Control 2.0 is strong, for now. But “don’t you care about the children?” is a powerful lever that will no doubt be used against those protesting the incursion into citizens’ privacy without due process. And, as last week showed, there are ways to push through controversial moves.

Still, we should be wary of manipulation on the other side as well. Being made aware of risks to our privacy is one thing; letting hysteria distract our focus is another. And it may have the pernicious effect of leaving us feeling more helpless than we are.

🌻 If you enjoy this newsletter, I hope you’ll consider sharing it with friends and colleagues and nudging them to subscribe? I’d appreciate it! 🌻

Sony’s stablecoin: the bigger implications

Last week, Sony got conditional approval from the OCC for a national trust bank in the US for the express purpose of issuing and managing a dollar stablecoin, with target launch in 2027.

This is not just “another stablecoin” story, not at all. It goes much deeper, on three levels:

1) Sony continues to expand our understanding of stablecoin business models.

Here we have a consumer-facing company issuing its own stablecoin, via a financial subsidiary.

Of course, one effective use case could be internal treasury transfers, with obvious advantages for a sprawling multinational with plenty of cross-border transactions between and within divisions.

But Sony has a vast, seriously vast user community. PlayStation alone has roughly 132 million monthly active users. And then there’s the movies, the streaming services, the music labels, all of which involve (or can involve) digital purchases of some kind. And the conglomerate has a fully licensed consumer-facing online bank in Japan

No wonder Sony has been active in blockchain-based exploration for years: tokenization, NFT issuance, application development, metaverse experiences and more.

By introducing a stablecoin into its onchain and offchain worlds, Sony can offer an engaged community new types of transactions in familiar environments, and expand the reach of and connectivity between Sony properties.

Another twist: unlike most other stablecoin issuers, Sony has its own blockchain, Soneium, co-developed with Singapore-based blockchain infrastructure firm Startale Group and launched last year. As far as I know, Sony has not specified that Soneium will be the new stablecoin’s chain, but there are strategic synergies.

The thing is, Soneium already has a stablecoin, Startale USD (USDSC), which launched in December 2025. Its total market cap is tiny (less than $5 million) but steady and with reasonable turnover.

Why will Sony’s stablecoin do better? For one, there’s the obvious brand-name recognition. Pretty much everyone has heard of Sony, and the name brings trust. Plus, there will no doubt be considerable publicity surrounding the launch, which should generate interest. And we can expect some degree of in-house marketing across the Sony empire.

Also, and I think this is more significant than many realize, it will be issued under the GENIUS Act. That also brings some reassurance, especially to American users – USDSC is issued under Singapore’s stablecoin regime.

So, Sony’s stablecoin is unlikely to be just about treasury transfers or payments, although those use cases will no doubt feature. The intersection of consumer experiences and payments promises to be one that will deliver digital applications that change our understanding of terms such as “audience”, “transaction” and even “property”.

2) The concession also reveals an intriguing interpretation of banking law.

The charter is granted to Sony’s US subsidiary Connectia Trust.

When Connectia applied for its charter last October, the Independent Community Bankers of America (ICBA) objected.

Not a surprise, the lobby group generally opposes anything to do with stablecoins, but this particular objection was intriguing in that it alleged that issuing retail-facing stablecoins is beyond the scope of the charter.

The GENIUS Act specifically empowers national trust banks to do that, but the ICBA raises a point: national trust banks are not empowered to offer retail-facing services. The provisional concession of Connectia’s charter shows that the OCC does not find that relevant.

Another objection raised by the ICBA is that the OCC overstepped its authority in its 2021 interpretive letter broadening the scope of national trust banks. Again, the banking regulator did not pay this much attention, further expanding the scope earlier this year.

An additional twist: No US entertainment company that owns a bank, because the Bank Holding Company Act forbids it. But Sony is based in Japan, where there are no such barriers.

This implies that Sony will be able to issue stablecoins to enhance the utility and profitability of its global entertainment properties, with most of the benefits presumably flowing to the head office in Japan. Disney, a US company, can’t do that – unless there’s a legal workaround that would enable Disney to issue a stablecoin. Perhaps, I’m not a lawyer. But it is striking that it is easier for foreign non-financial conglomerates to issue stablecoins in the US, essentially taking deposits and offering financial services while boosting innovation, engagement and profit, than it is for a US non-financial conglomerate.

3) Despite the spread of stablecoin regulation in key economies, jurisdiction still matters.

The move is also interesting given that Japan, Sony’s home country, was the first major economy to pass stablecoin legislation back in 2022. Even under the GENIUS Act, Sony’s stablecoin could launch in Japan but circulate in the US if its reserve structure and operating conditions were sufficiently similar to those set out in the US law.

But Sony chose the US as its launch jurisdiction.

It’s worth thinking about why it did so. The potential size of the US market for the Sony stablecoin is no doubt the main consideration.

But I expect there’s also the confidence that the US will continue to be more innovation-forward than most other countries.

Japan may have been first, but as far as I know, it only has two authorized stablecoins in circulation, only one of which is issued by a trust bank (SBI Shinsei Trust Bank, part of financial conglomerate SBI Holdings). What’s more, SBI Shinsei submitted its application in early March 2025, and the stablecoin only launched last month. The Japanese authorities are being careful.

There’s a lesson in here for regulators around the world focusing on caution over innovation: safety is important, but being too careful brings an opportunity cost, especially significant in a new field in which shaping consumer habits creates moats.

See also:

Sony’s stablecoin: some interesting threads (Dec 2025)

Sony’s blockchain backlash (Jan 2025)

Sony’s crypto exchange: the convergence? (July 2024)

ASSORTED LINKS

(A selection of reads I came across this week that I think are worth sharing, not about crypto nor macro. I try to choose links without a paywall, but when I feel it’s worth making an exception, I specify.)

Marlene Laruelle argues that we can’t fix the “crisis of liberalism” without first asking where it went wrong, why, and what we want it to be. Thought-provoking for sure, but what throws me is the framing of liberalism as something to be “fixed”, like a corporate culture or a political party. It’s a philosophy, which rarely conform to formulas rigid enough to be “reformed”, and which don’t have a central authority let alone a “marketing team” to communicate the changes. That said, it is a useful examination of why liberalism lost its lustre. (Liberalism, Heal Thyself, Persuasion)

We know that AI is coming for jobs – but what will it do to the structure of work? Derek Thompson looks at how income distribution is changing as AI makes it easier for people to work for themselves. Great for opportunity and probably life satisfaction – but there are social downsides as more of us become isolated solo-preneurs, and economic ones as the US tax base changes. (It’s the Best Time Ever to Become a Millionaire by Working Alone, Derek Thompson – paywall)

One of the many uplifting memories from this World Cup will of course be the impact Scotland made on the US, not so much via their game as via the enthusiasm and charm of the fans. Ed West gives us a brief history of Brand Scotland, and how the Americans have fallen for it to the extent that the day the Scots left Boston in June was a day of mourning. (The triumph of Brand Scotland, The Wrong Side of History)

I’m undecided on whether or not to see Christopher Nolan’s “The Odyssey” – I was leaning towards no, but Ted Gioia’s account of the power of the story and its “orality” (meant to be heard) has me intrigued, not just for the images the spoken word can conjure, but also for the resulting music. (What You Won’t Learn About the Odyssey from a Movie, The Honest Broker – paywall)

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

Don’t worry, no football photos today, although it is a pretty big football weekend for us in Spain.

Instead, in the hopes that you’ll join me in sending plenty of good vibes over to our team in New York, here are some iconic Spanish musicians:

Paco Lucía – Entre Dos Aguas

Jarabe de Palo – La Flaca

Joaquín Sabina – 19 Días y 500 noches

C. Tangana and Antonio Carmona – Me Maten

Rosalía – Despechá

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.