WEEKLY - stablecoins + sanctions, BTC + safe havens

plus: assorted links, nostalgia, and more

Hello everyone! I hope you’re all doing well, and doing a better job than I am of keeping track of the days of the week…

📽 After a break, I’m picking up “Press Publish” again! Next Friday, June 19th, come join me for a live chat with Izabella Kaminska, author of The Peg and The Blind Spot, about newslettering, media, too much information and more. More details below! 📽

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

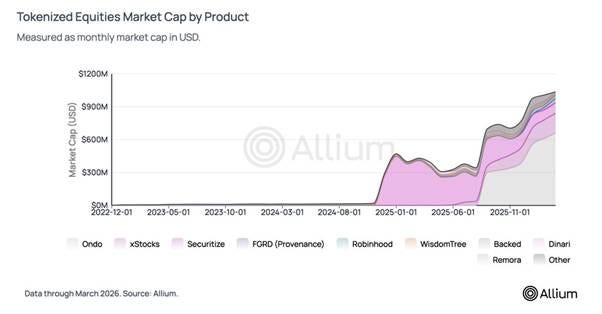

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

In this newsletter:

Stablecoins and sanctions evasion

No, Bitcoin has not “failed” as a safe haven

Assorted links: The World Cup, economic development, top living US musicians, the value of attitude, the search for self.

Weekend: bring-bring and yip-yip

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

✨Press Publish with Izabella Kaminska✨

Come and join me and long-time journalist, finance expert and independent thinker Izabella Kaminska next Friday June 19th, at 3pm UK time/10am ET for a live chat about why and how she does what she does: how she manages to produce not one but two excellent newsletters (The Peg and The Blind Spot) while also writing for mainstream media, speaking at events, and juggling a ton of other stuff besides. We’ll touch on her long media career, where she thinks the industry is heading, how she handles the firehose of information, what works for her and what doesn’t, what advice she’d give her younger self, and more.

Again, Friday June 19th, at 3pm UK time/10am ET: https://open.substack.com/live-stream/239917?utm_source=live-stream-scheduled-upsell

Some of the topics discussed in this week’s premium dailies:

Coming up this week: inflation, politics, geopolitics

Monday mood: No, Bitcoin has not “failed” as a safe haven

Macro: job perks

Markets: nerves up

Nigeria’s CBDC: next steps and lessons learned

Term of the day: PAPSS

Macro: the consumer expectations question

Stablecoins and sanctions evasion

Term of the day: Neomercantilism

Market convergence: What’s in a price?

Term of the day: oracle

Macro: US CPI grumbles and yawns

From the Pacific to Wall Street: tokenized sovereign debt

Term of the day: Brady bonds

Macro: US wholesale inflation

Stablecoins and sanctions evasion

In 1966, psychologist Abraham Maslow wrote:

“I suppose it is tempting, if the only tool you have is a hammer, to treat everything as if it were a nail.”

Tempting indeed, to the extent that it becomes instinctive, we don’t even recognize the situational bias at work.

It’s directly applicable to the construction of finance today. If you’ve ever wondered why regulators keep on adding layers to the Bank Secrecy Act – giving banks even more unproductive paperwork and sunk costs in the fruitless pursuit of proof of money laundering – well, Maslow has your answer: adding controls is the only thing regulators can do. So they do it, a lot. And if the action is not producing the desired result, it’s obviously because they’re not doing enough of it.

The same applies to sanctions. They have proven effective in the past, but targets find workarounds which makes sanctions less effective in the future. Yesterday, the EU presented its 21st sanctions package against Russia. I’ll say that again, the 21st. The first 20 didn’t achieve the objective of convincing Putin that he should withdraw his forces from Ukraine, but the 21st should do the trick, right? And let’s remember that the loudly telegraphed threat of sanctions didn’t stop the invasion in the first place.

The futility becomes almost farcical when it comes to sanctioning crypto exchanges and even stablecoins. I’ve written about this before so I won’t repeat myself at length here, other than to say: sanctions on any activity carried out on a global, decentralized network will fail. The only reasonable explanation I can think of for going through the motions is: “it’s all that we can do, so it’s what we’ll do”. Our hammer hopes that the target will behave like a nail.

Given the flurry of related news items over the past week, it’s time for an update.

One example of futile sanctions I’ve written about before is those on the issuers and supporting platforms of the Russian A7A5 stablecoin, and from the EU on the stablecoin itself.

Last week, blockchain cybersecurity firm CertiK published its 2026 Stablecoin Threat Intelligence Report which devotes roughly half of its 22 pages to A7A5. Summarizing:

In 2025, A7A5 processed more than $110 billion in onchain transactions.

It accounts for almost half of the non-USD stablecoin market.

This is despite an absence of independent reserve attestations.

Its ecosystem has direct links to ransomware from known attacks, as well as significant amounts of North Korean hacking proceeds.

The number of holders more than doubled between February 2025 and May 2026, to ~29,000, with no discernible dent from any sanctions event.

(chart via CertiK – roughly 99% of A7A5 addresses are on Tron)

The Russian Central Bank has formally recognized A7A5 as a digital asset under the country’s legal framework.

Russian Foreign Minister Sergey Lavrov has invited all African nations to join A7, the stablecoin’s sanctioned network – it currently has offices in Nigeria and Zimbabwe, is recruiting for an office in Togo, and is reportedly in talks with Madagascar.

The story gets weirder: yesterday, UK high school student Alexander Browder – the son of investor and Putin antagonist Bill Browder – was put on a “no entry” list by Russia because of a report he published in March on A7A5’s use in illicit finance. This has been inflated in western media (fed by Alexander’s social media posts) as full “sanctions”, but whatever – he joins his father in being blocked from travelling to Russia.

One spin I’ve seen is that this is Russia’s way of getting back at his father, as if Alexander’s limited vacation options would impact their lifestyles that much. Oddly, it feels more like one big publicity stunt: the Browders get more attention on their anti-Putin cause, and Russia gets more potential users of A7A5. And the more western sanctions target a specific token while it keeps on growing, the more problematic regimes will think “hmm, we can do that too”.

But the ineffectual use of the hammer continues.

The sanctions package proposed by the EU yesterday includes 31 more Russian banks as well as 20 crypto platforms, banks and oil traders outside of Russia, for helping Russians evade sanctions. According to Reuters, 11 crypto platforms are named (the list has not yet been published).

There’s more: for the first time, the EU is considering a full third-country ban for digital asset services – if a country is suspected of harbouring a crypto exchange that works with sanctioned Russian entities, all crypto platforms in that country will be blocked from using EU services and rails. The UAE and Türkiye may have a thing or two to say about this.

Last week, the US Treasury sanctioned Iran’s largest crypto exchange Nobitex along with three others (Bitpin, Ramzinex and Wallex) operating in the country, as well as certain related and well-connected individuals – a Reuters report last month flagged that Nobitex was founded by two brothers belonging to one of the most influential dynasties in the Islamic Republic, a family with close ties to Iran’s Supreme Leader. Crypto is important in Iran. According to blockchain forensics firm Chainalysis, the Iranian crypto ecosystem processed roughly $7.8 billion in 2025, with IRGC-related address accounting for over 50% of total value received.

The previous week, US Treasury Secretary Scott Bessent announced that the US has seized approximately $1 billion of Iran’s crypto assets. I’m not sure how that was done – Bessent went on to talk about how his team “just outright grabbed the wallets” which, yeah, it doesn’t work like that. And I don’t think he realizes how much statements like that push more people onto rails that are “out of reach”.

And the week before that, the Wall Street Journal reported that the Iranian regime was moving “billions” worth of crypto assets through Binance, which Binance’s CEO has vehemently denied – he insists that Binance does not work with sanctioned entities or individuals, and the transactions mentioned in the report happened before the relevant sanctions list was published. This highlights a fundamental problem: for individuals and entities to be blocked, they need to be named. And once they are named, activity can relatively easily move to a family member or a related entity. Compliance programs don’t usually check for company provenance, just that a company is not on any entity lists.

This effectively makes sanctions a game of whack-a-mole which, in the fast-moving world of blockchain applications and assets, hobbles the strategy from the outset. Forensics firms are performing valuable work in tracing flows and labelling addresses – but blockchain science is not exact (mis-labelling is a thing), and will always be a step or two behind.

But what is unfortunately often overlooked in the “stablecoins facilitate crime” whining is that the transactions are traceable. This can fuel future action, even if too late. More importantly, it can sketch out networks. Any law enforcement officer will tell you that information is the ultimate tool for combating crime, and that knowing who is doing business with who can direct attention to the source and the nodes of distribution. Maps matter, and when it comes to money laundering via traditional financial rails, complete ones adjusted in real time don’t exist. Onchain, they can.

A separate issue is to what extent sanctions evasion is bad. We can agree that crime is bad – but who gets to decide what gets included in that definition? A doctor in Isfahan who pays for penicillin shipped across the border from Azerbaijan with USDT via Nobitex, is she committing a crime? The EU has even gone as far as sanctioning European individuals for being too pro-Russia – whether you agree or not with what they say, were they committing a crime?

The moral question of what even is crime goes beyond the individual. In an interview with the Financial Times last December, ECB Chief Christine Lagarde presented a clear use case for the digital euro:

“You know, there is a very strange situation at the moment where people can be barred from access to any financing because of a decision made on the other side of the pond. There’s the case of the International Criminal Court judges at the moment who have no access to finance. If we had a digital euro in place, that person could use financing in whichever way he wants and should, because he would not be deprived of his financial sovereignty himself.” (my emphasis)

Essentially, she is saying that sanctioned individuals should be able to have access to alternative financial rails, unless of course it’s the EU doing the sanctioning. Reading between the lines, there’s a chance she’s wondering if the EU itself might ever be on the receiving end of the hammer. Would it necessarily be guilty of committing a crime?

I don’t want to get too far off topic here, but I did want to make the point that sanctions on blockchain applications won’t work. And that’s not necessarily always bad. But it is complex.

The repercussions of this are bigger than most realize. Over the years, the power of sanctions has meant fewer boots on the ground, fewer human lives at risk. Sanctions have been a tool of peace, even if innocent people get punished at times. Removing their efficacy makes the world a more dangerous place, not just because the funding of really bad things moves further out of reach, but also because a new hammer will be needed.

Then again, better information could make that new hammer more surgical and therefore less risky. Blockchains are transparent, movements can be traced, and while the data will never be perfect, it’s a lot more granular and harder to disguise than in today’s opaque, fragmented system.

See also:

Russian stablecoins in Africa (Apr 2026)

Sanctions on a stablecoin (Oct 2025)

The dark side of crypto (Jun 2025)

No, Bitcoin has not “failed” as a safe haven

It’s to be expected, I guess. When Bitcoin’s price does not behave as people assume it should, the obvious conclusion is that Bitcoin has “failed”. Over the past week, when both crypto and stocks were going down, I had a couple of journalists reach out for comment on whether Bitcoin could still be considered a “safe haven”. And I’ve seen more than a few headlines stressing its failure as such.

Expected, but still frustrating. We’ve seen the same reaction to every other BTC price slump, going back to when it was around $3,000 and media started paying attention. The repetitive chorus has generally been along the lines of: Bitcoin has obviously failed as a safe haven, it’s not much of a store of value, it’s a terrible payments network and doesn’t even do well as a speculative asset now that there are so many others with actual fundamentals.

And I get it, I used to work for media back in the day (but not as a journalist) and so I understand the need to come up with stories that will get clicks. And people do love 1) articles about crypto prices, and 2) proclamations of the end of a controversial asset class. Put them together and you’ll get traffic.

But this approach just perpetuates the dumbing-down of information and diverts any actual thought about what the relevant terms mean.

So, allow me.

First of all, what do we mean by “safe haven” investment? According to Investopedia, it’s an asset that “can hold or lose less value while other investments, like stocks, fall”. I’ll quibble with that definition further down, but let’s take it at face value for now.

Bitcoin has not failed at this – it has grossly underperformed a rising market, but we have not yet had the opportunity to see what it does when stocks fall, because they keep going up.

Of course, there have been bad days in equities. The Friday before last, for instance – Nasdaq dropped more than 4%, so did BTC. But by Monday, it had walked back most of what it lost, while Nasdaq hadn’t. In March, Nasdaq lost 4.4% while BTC gained 1.8%. After last year’s Liberation Day, Nasdaq had lost 9.3% by the close of business the following Monday. BTC was down 7.1% over the same period. In the first two weeks of March 2023, as markets were rocked by an unfolding banking crisis, Nasdaq was down 2.3%, BTC was up 4.6%. What about that month as a turbulent whole? Nasdaq eked out a gain of 6.8%. BTC was up 23%.

And yet people still insist it is not a safe haven?

This is in part because the firehose of news has made most of us short-term in our thinking. BTC is down while stocks are down so therefore it has failed, even though safe havens are not supposed to be short-term bets, just as most portfolio allocations are not supposed to follow day-to-day or even month-to-month moves.

It’s also because the firehose demands quick public reactions which leaves us reaching for easy yet superficial conclusions. When Bitcoin goes down along with other assets, it obviously can’t be a safe haven. That shows a lack of understanding of what “safe haven” means, even according to the traditional definition of “loses less value”.

But let’s ditch the traditional definition and, for the sake of argument ask what “safe” and “haven” actually mean outside of investment adviser jargon.

Safe doesn’t necessarily mean a steady price; it can mean protected from seizure or cancellation or dilution – that can’t be said of either stocks or bonds.

Haven doesn’t necessarily only mean refuge from portfolio losses; it also means a safe space, or an asset that can protect both wealth and access to economic activity – a refuge from the weaponization of finance, unfortunately relevant to a widening group of people (and how sure are you that you’ll never be one of them?).

So, seriously, has Bitcoin failed as a safe haven? No, it hasn’t, whichever definition you choose to latch on to.

It’s underperformed, yes, and I believe there could be more downside ahead if stocks turn ugly. I also don’t think it should be used as a portfolio “safe haven” as it is usually buffeted by several simultaneous narratives and we can never be sure which will predominate. We could even see periods where BTC gets hit more than equities, but we can also play around with the calendar window to prove a broader point: the goal posts are distorted.

Bitcoin is not supposed to go up when stocks go down. That’s a crazy assumption. Bitcoin isn’t supposed to do anything other than obey the rules of its algorithm, as it has no CEO or marketing team to tell us what it even is.

And as long as Bitcoin does that, it hasn’t failed.

ASSORTED LINKS

(A selection of reads I came across this week that I think are worth sharing, not about crypto nor macro. I try to choose links without a paywall, but when I feel it’s worth making an exception, I specify.)

The FIFA World Cup 2026 is upon us, and in this well-reasoned report, uber-forecaster Joachim Klement of Panmure Liberum predicts that Netherlands will win. Details aside, it’s a fun read, even if (like me) you’re not really into soccer. That said, I would be into Spain winning. (FIFA World Cup Predictions 2026, Panmure Liberum)

“It has become a tradition among banks to make these forecasts to show that economists have a sense of humour (they don’t) and can actually forecast things that matter. They can’t. Or rather, most of them can’t.”

It’s astonishingly rare to read some grounded advice aimed at young people on how to exit the anxiety trap and side-step the rat race, that also works wonders for old people (cough, who me?) that are also trying to stress less, slow down and appreciate the rhythm of each day. But, unsurprisingly, Jasmine Sun delivers, in a well-written tribute to attitude. (The old world is dying, Jasmine’s Substack)

The best explanation I’ve seen on why China’s and India’s economic development took different paths – it’s partly top-down centralized decisions, but we often fail to appreciate the role of ingrained social structure. Human capital matters a lot. (Why China got rich and India didn’t, David Oks)

New York Times readers unsurprisingly pushed back on the journal’s recent list – curated from music industry recommendations – of the top living American songwriters. To their credit, they then canvassed the public, and published the results. (The Reader Top 100, New York Times – paywall)

Packy McCormick starts out by asking the question: “If new technology is so great, why are so many people unhappy?” – and ends up talking about what the search for meaning has to do with learning how to be yourself. Much less hand-wavy than my description may make it sound, the piece is a worthy read that will probably change your mind about some big things, even if you only get as far as the paywall which is a generous ways down. (Riding the Leopard, Not Boring – paywall)

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

This morning, on the way to the grocery story, my husband and I were reminiscing about our favourite toys from when we were kids. His was a set of interconnecting Lego-like bricks with which you could build castles. Mine was an old Fisher Price telephone, with wheels, a dial, an attached bright red receiver and a string with which you could pull it along and a bell would ting (yes, I’m that old). I have no idea why, but that’s the toy I remember most fondly.

Young people today would probably look at that and have no idea what it was.

We then moved on to reminiscing about the brilliant Muppets sketch with aliens identifying a phone – not from its shape, but from its sound. Which got me thinking: the sound is the generational bridge. The shape of phones may change, and their function may have evolved well beyond communication, but bring-bring still means that someone wants to talk to you, right?

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.