WEEKLY - the shocks of the week

Germany, geopolitics, macro, crypto and more...

Hello everyone! I hope you’re doing well!

You’re reading the free weekly Crypto is Macro Now, where I reshare/update a couple of posts from the past few days, and include something from outside the crypto/macro sphere that is currently inspiring me (it’s a fascinating world out there).

If you’re not a subscriber to the premium daily, I do hope you’ll consider becoming one! For $12/month, you’ll get ~daily commentary on how crypto is impacting the macro landscape, and vice versa. I talk about adoption, regulation, tokenization, stablecoins, CBDCs, market infrastructure shifts and more, as well as the economy and investment narratives.

Feel free to share this with friends and colleagues, and if you like this newsletter, do please hit the ❤ button at the bottom – I’m told it feeds the almighty algorithm.

I did some talking this week:

On Wednesday, I was a guest on Scott Melker’s Wolf of All Streets Show, you can see that here.

I also had a fun chat with Maggie Lake for her excellent Talking Markets show – appropriately for the discussion below, it opened with “Are we in a new era?”. You can watch that here.

On the latest episode of Bits & Bips, James Seyffart and I talk to Steve Hou and Steven Erlich about strategic crypto reserves, macro mayhem, and more. You can listen here (Spotify link), or watch here.

Yesterday, I was interviewed on CNBC’s Crypto World about the Strategic Reserve and BTC’s strange reaction.

And last night I was invited on to Bloomberg’s show The Close to discuss the Reserve in the context of the Crypto Summit – I’m on at around minute 49.

In this newsletter:

Tectonic plates are shifting

The German shock

The market reaction

What now?

Some of the topics discussed in this week’s dailies:

Upcoming: What to keep an eye on this week

Many layers of error

The jolt that got real

Markets and new jitters

The trade war

The kinetic war

GDP models flashing red

But it’s not as bad as it seems

What does all this mean for crypto?

Tectonic plates are shifting

The German shock

The market reaction

What now?

SBR: A nice surprise

The gathering

The market doesn’t care

Tectonic plates are shifting

Since the inauguration of Donald Trump’s second term as US president just a month and a half ago, we’ve had more signs than we can reasonably handle that the global order is changing. But this week, the pace feels like it kicked into turbo drive.

We have the imposition by the United States of hefty tariffs on its three largest trading partners, kicking off the broadest trade war in almost 100 years. Or maybe not. Or maybe yes.

We have a post on Wednesday by the Chinese Embassy in the US, echoed in the official briefing on the just-ended National People’s Congress, that said China was ready for “a tariff war, a trade war or any other type of war”, and would “fight till the end”. An astonishingly blunt statement by any account.

(post by @ChineseEmbinUS)

We also have the US decision to suspend intelligence sharing with Ukraine, and to ban other Five Eyes members – specifically the UK – from doing so. This is an even more blatant “hanging them out to dry” than the pause in hardware shipments, as without insight into Russian movements and target locations, Ukraine forces are effectively shooting blind with limited ammunition.

And there’s the not-so-subtle flex from French President Emmanuel Macron in the form of an offer to extend its “nuclear security umbrella” to Europe. According to the Federation of American Scientists, France has around 290 warheads, which would make it the fourth largest nuclear power in the world behind Russia, the US and China.

Macron also said he will convene a meeting next week of European army leaders willing to send peacekeeping troops to Ukraine should there be a deal with Russia – I don’t know who would be on that list. Russia, meanwhile, has rejected the idea.

Meanwhile, EU leaders gathered on Thursday in an emergency summit to discuss a coordinated approach to defence including joint borrowing of up to €150 billion (~$160 billion) and fiscal flexibility for individual nations to potentially add another €650 billion to that funding. All 27 member states agreed to examine the proposals, and there was a show of fighting spirit in talk about winning the “arms race”. Ambitious, vague and controversial, but an astonishing pivot nevertheless.

And, embellishing all of the above with a decisive flourish, Germany has upended decades of history to embark on a new phase of industrial and military expansion.

The German shock

Late on Tuesday, the incoming chancellor Friedrich Merz announced that the outgoing government will vote to amend the country’s constitution to relax debt limits and allow the borrowing of up to €900 billion (~$971 billion) to fund defence and infrastructure investment.

It’s impossible to overstate the significance of this move, which is all the more astonishing given that Merz campaigned on opposition to fiscal expansion. The news is a material turning point for the country which has been facing economic stagnation and domestic unrest with no clear solution in sight, given the political paralysis resulting from deepening polarization.

The proposal has to be approved by the outgoing government before March 25 as right-wing AfD, which is against fiscal expansion, will hold enough sway in the new legislature to block such a move. A possible glitch is that the backing centrist coalition will need the cooperation of the declining-in-relevance Green party, who are reportedly upset that the announcement did not promise carbon neutrality.

Assuming that gets smoothed over, this is extremely good news for Germany, at least in the short-term. It will hopefully put a floor under the industrial decline of the past decade while strengthening local manufacturing for local consumption at a time of rising trade barriers. It should inject both funds and urgency into reforming the energy grid and transport infrastructure. It will also jolt leaders out of their fear of debt and politically motivated limits on investment, and its example just might be the incentive the European Union needs to actually do something about its paralyzing regulation and preference for the status quo.

There is a big caveat, however, and that is the deepening political tension.

Almost half of Germany’s youth voted for parties on the far left or the far right – both extremes are not happy about the militarization. The next elections are years away, but unless the investment triggers an astonishing economic recovery, the AfD will most likely win a controlling position in government, possibly carrying out its threat to take Germany out of the European Union.

And within Europe, rifts are widening. Resentment at the creep of centralization, seen by many countries as a power grab, could further weaken the bloc’s ability to implement necessary reforms and present a credible threat deterrence. Hungary has said it won’t block increased defence spending, but its stance so far has been to veto direct aid to Ukraine. There are moves under way to get around Hungary’s block, which would no doubt further antagonize the US and Russia – but this would need all other nations to agree, and Hungary does have allies.

The market reaction

Markets are understandably freaked out.

The yield on Germany’s 10-year bund jumped by 30 basis points on Wednesday, the most since the aftermath of the fall of the Berlin Wall in 1989.

(German 10-year bund yield, chart via TradingView)

This is not necessarily the work of bond vigilantes protesting the debt increase. For one, Germany’s debt is still low by global standards. Even after the spike, yields are still under 3%, also low by global standards. Just two weeks ago, Bloomberg reported that investors were urging Germany to issue more bonds – and there is likely to be demand for what’s coming, at least at first, and especially if it turns around the waning economic outlook.

True, there’s no doubt some reaction to the unexpected scale of the coming flood. But it’s also possibly the result of the sudden attractiveness of German industrial equities triggering some portfolio rotation. And it’s an acknowledgement that Thursday’s ECB rate cut could be the last for a while.

The euro has surged against the US dollar, reaching its highest valuation since the US election and upending the “American exceptionalism narrative”.

(EUR/USD chart via TradingView)

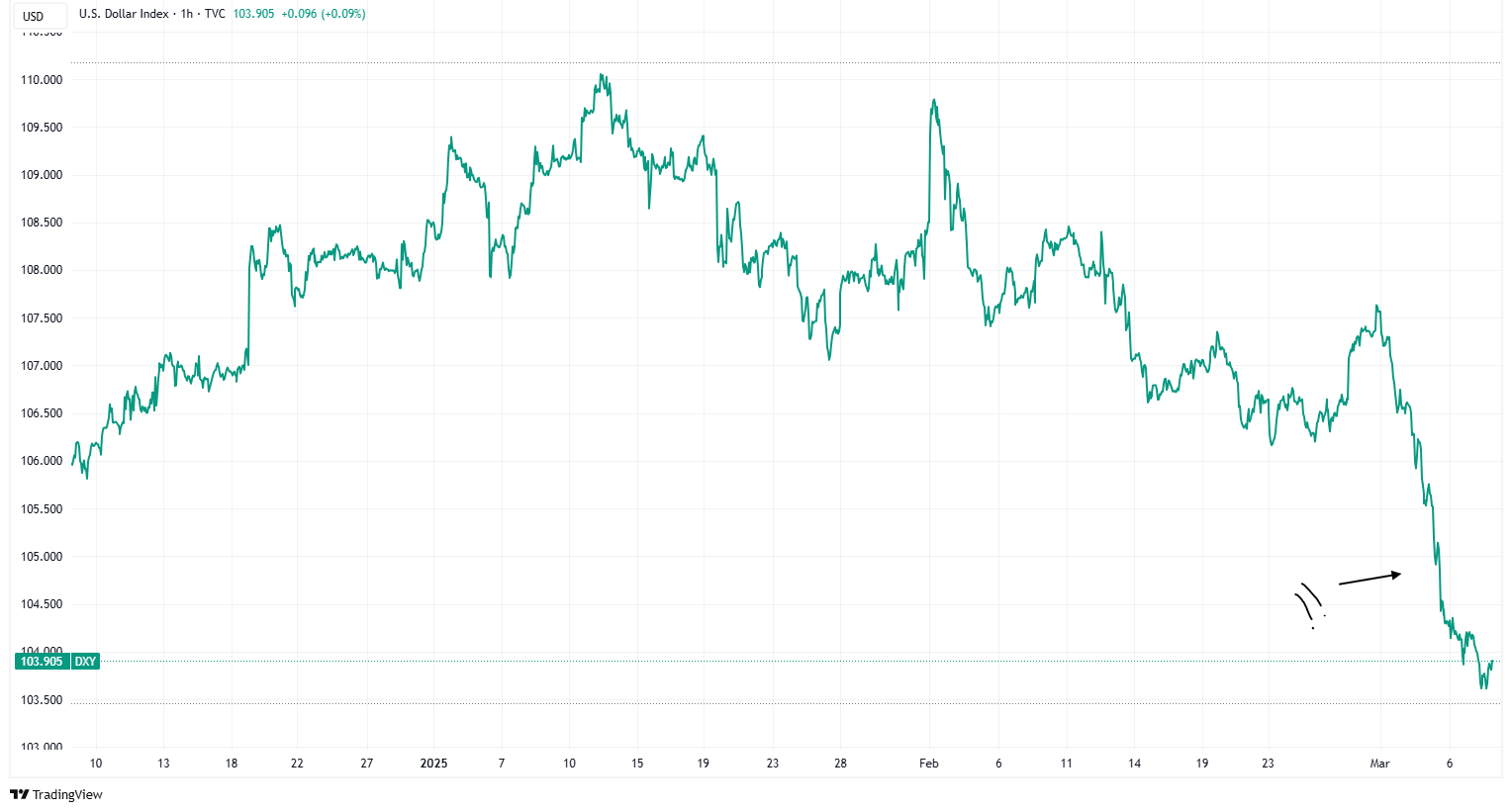

And just when you’d think all the talk of war would send the world scurrying into safe havens such as the US dollar, it’s falling against not just the euro but also against other major anchors such as the yen and the Swiss franc.

(DXY dollar index chart via TradingView)

US equities don’t yet know what to make of this, especially since it comes at a time of acute tariff uncertainty. A lower USD is good for the US manufacturing outlook, but it tends to be inflationary as imports – already groaning under actual or threatened tariffs – get more expensive.

(S&P 500 chart via TradingView)

Meanwhile, the US bond market seems to be ignoring the inflation threat, instead choosing to focus on a greater likelihood of rate cuts given signs of a slowing economy. Friday’s US employment report didn’t deliver any notable shocks, yet the slight uptick in the unemployment rate and the narrow negative miss (151,000 jobs added in February, vs 160,000 expected) were taken as bad news by a market primed for worry.

In sum, macro jitters are crisp, news is coming thick and fast, and none of us fully understand the ramifications of what we’ve seen so far this week, especially since safe haven indicators – gold, US government bonds and BTC – are not yet reflecting the escalating talk of war.

BTC is holding up relatively well, perhaps in part because of the dollar weakness, but also due to confirmation of an official Strategic Bitcoin Reserve – this was disappointing for many, but overall positive in that it enshrines its store of value characteristics without requiring the additional commitment of US public funds. That it’s not doing better underscores how macro concerns still weigh heavy on crypto assets.

(BTC/USD chart via TradingView)

What now?

In a world so used to focusing on monetary and economic indicators, so primed for signs of greater liquidity, so unfamiliar with deep geopolitical swings, I worry that we’re overlooking bigger risks. Even if they’re remote, they shouldn’t be ignored.

I’m in favour of more defence spending for Europe, it’s about time, and it will lead to stronger civilian infrastructure as well as faster development of new home-grown technologies.

I’m also appreciative of the drastic moves needed to shake Europe out of its lethargy and paralysis.

But, we don’t yet know what Europe’s new focus on defence expenditure will do to welfare budgets or inflation. This will matter as higher consumer borrowing costs start to reflect the higher yields, when protest can be registered at the ballot box. Support for right-wing parties across Europe is surging, a trend that could accelerate should current leaders continue to talk about making sacrifices for a war most Europeans sadly but understandably got tired of a while ago.

What we do know is that a well-armed nation is more likely to flex muscle.

We also know that the US is no longer the power it once was – even its Secretary of State Marco Rubio recently acknowledged we are now living in a “multipolar world”. The withdrawal of the US from long-standing allegiances and associations, at a time it is urging allies to be more self-sufficient, may boost American manufacturing – but at the cost of its global influence. We don’t know what the impact of this will be on smaller nations previously reliant on the US umbrella, nor on other powers eager to step into perceived gaps.

Regular readers will know I’ve been flagging geopolitical shifts for some time, as I believe crypto is not just a haven and a protector of individual agency as politics gets crazy – it’s also a new tool in the box for nations navigating shifting alliances. It’s not hard to conclude that we’re no longer sleepwalking, we’re actively rushing into a world in which this is will become uncomfortably relevant.

These are scary times, which are difficult for most but which always produce opportunities, especially for those focused on adapting to the likely landscape when the dust settles, which it always does. And while fear centralizes, its corollary – lack of trust – does the opposite. This battle, between centralization and decentralization, will be the tussle of the first half of this century, and will impact governments, social structures, economic outlooks and adoption of new technologies.

There’s a Persian saying I cherish: “They can pull the carpet out from underneath your feet. But you can also learn to dance on a moving carpet.”

We certainly can. And we’ll need some tools, good friends and plenty of internal resilience to help us do that.

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

With politics and the economy feeling increasingly unhinged and with our feeds getting distractingly noisy, it’s refreshing to be reminded that the world is magical. What’s more, it marches to its own rhythm, and while us destructive humans can get in the way, nature will do its thing.

Today, I want to share with you some of the striking images from the 2025 World Nature Photography Awards, in the hopes of adding even more beauty to your weekend. The whole selection is worth a look, but here are the four that most moved me:

by Marusha Puhek

by Tom Nickels

by Marcio Esteves Cabral

by Ael Kermarec

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade.