WEEKLY - US bank deceit vs Hong Kong's DLT embrace

plus: assorted links, muppet music and more

Hi everyone! What a week… a short one for me (oh but so intense!) as I am travelling at the moment and sending this from a coffee shop in Kingston-upon-Thames. Back at my desk on Monday.

✨

If you’re not a subscriber to the premium dailies, I hope you’ll consider becoming one? You’ll get access to market commentary as well as adoption insight and industry trends. Plus, links and music recommendations ‘cos why not…

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

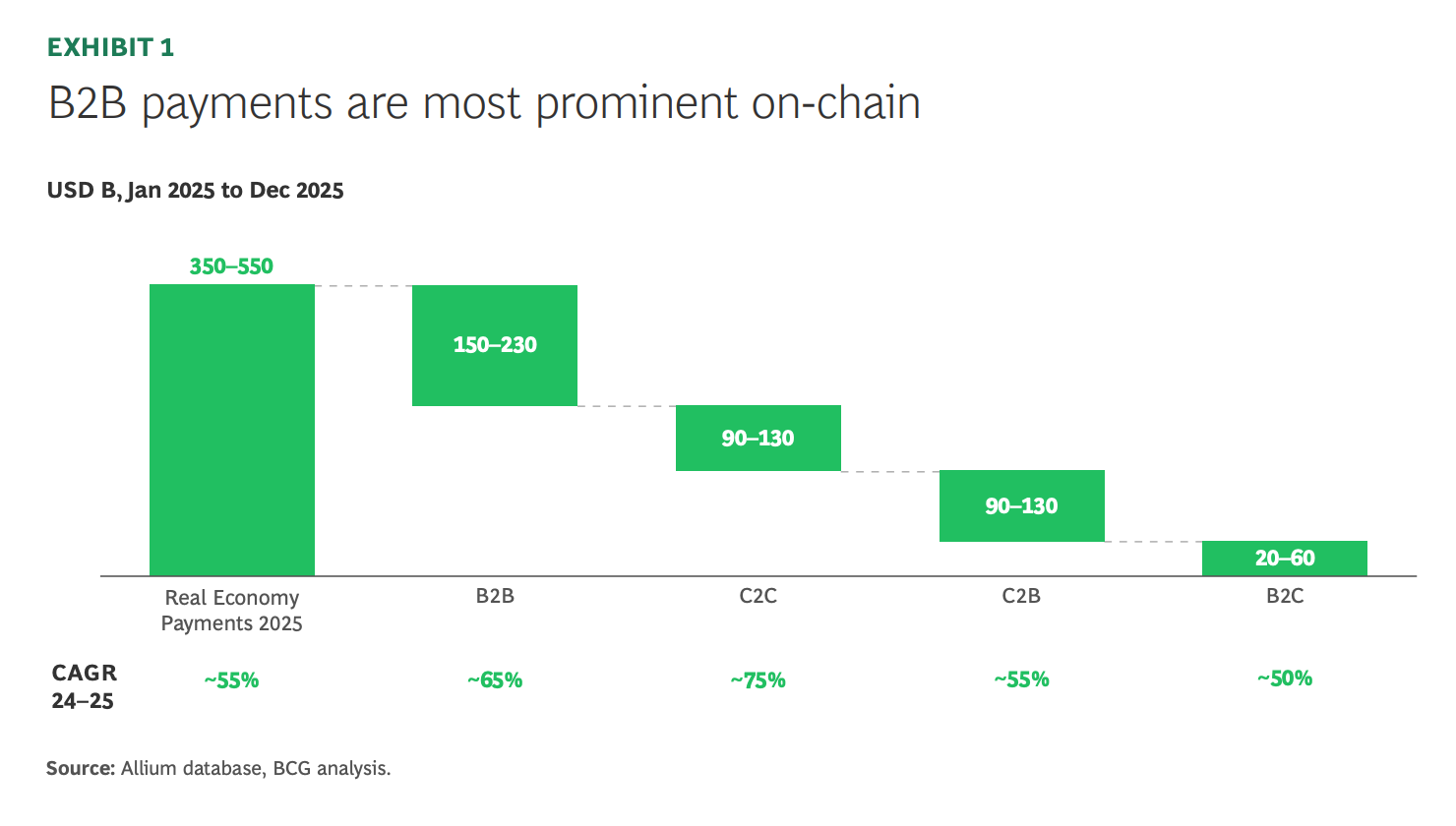

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

In this newsletter:

Stablecoin rewards and bank deceit

Hong Kong banks and DLT innovation

Assorted links: Western civilization, Irish magic, em dashes and an AI narrative less confusing than most

Weekend: Muppets music videos, just because.

✨ Use the discount code MACRO for 20% off! ✨

Some of the topics discussed in this week’s premium dailies:

Coming up this week:

Markets: sentiment turns

BTC: surprising resilience

Macro: China

Roundup: Stablecoins and deposit tokens

Markets: baffling until you step back

Stablecoin rewards and bank deceit

Macro: US CPI

A year ago: a different type of turmoil

Geopolitics, crypto blues, Tether and Bitcoin, and more

Hong Kong banks and DLT innovation

Markets: slippery sentiment

Stablecoin rewards and bank deceit

It finally happened. I’m not easily triggered, but some of the statements heard on stage this week at the American Banking Association (ABA) annual event have moved the gaslighting from irritating to alarming, from insulting to infuriating.

Here’s an excerpt of the opening speech from ABA CEO Rob Nichols:

“Many banks are eager to offer products and services in the digital asset marketplace. What we don’t support is an uneven playing field where new entrants want to offer bank-like products without having to comply with bank-like rules.”

An uneven playing field… Where to even start.

I’ll start by taking a step to the side and clarifying that, for me, the battle is not about whether stablecoins should be able to earn interest. The GENIUS Act makes clear that issuers cannot directly pay interest but leaves the door open for non-issuers to do so by calling them “rewards”. The bank lobbies are scrambling now to include language in the crypto market structure CLARITY Act currently stalled in Congress that would, in their words, “close the loophole” by banning all types of rewards on stablecoins, even those limited to activity rather than balances.

I have concerns about stablecoins being able to earn interest:

One is a race to the bottom as issuers compete to entice users. This would most likely lead to a concentration of volumes in those that pay higher rates, which could destabilize smaller platforms while giving more market power to the large ones. Greater concentration is not ideal for the industry’s resilience.

Also, earning interest will require identification – as with bank deposits, it’s the account that earns according to its balance rather than the stablecoins themselves. Disincentivizing self-custody of stablecoins erodes financial privacy. True, it’d be the users’ choice, but if there are financial reasons to give up privacy, people will generally do so.

Plus, stablecoins are meant to move. If they pay interest, there’s more incentive to stay put. I’d much rather see regulation relaxed to allow an active tokenized money market fund (TMMF) sector develop, with idle stablecoin balances swept into assets that are meant to stay put, and swept out again when needed for action. Unlike in traditional finance, both stablecoins and TMMFs live on the same rails, so this swap can take less than a second. And TMMFs, unlike their traditional counterparts, can earn interest even if held for less than a day.

So, I don’t care about stablecoin interest. I do care about economic stability, which can only be maintained through innovation. And I care very much when a large, extremely profitable and powerful industry blatantly lies to the public in order to maintain its monopolistic privilege.

I’m not anti-bank, not at all – they provide essential services, and I’m very happy with the bank I use here in Spain, with whom I’ve had a decades-long relationship. I’ve worked for banks, I have friends who are bankers, I sometimes teach a blockchain class for bank executives. (That said, I’ve had nothing but nightmare experiences with American banks, JPMorgan Chase in particular, perhaps a story for another time.)

But the anti-innovation stance is unpatriotic, the false assumption that risk is greater outside the banking industry than within is arrogant, and the “protect the little guy” protests of large banks are deceitful. It feels like banks have forgotten why they exist in the first place.

To start with, what does Nichols mean when he complains about the “uneven playing field”? He clearly wants us to conclude that crypto companies are the ones arguing for an unfair advantage, that they want to copy bank business models but with fewer constraints and less oversight. This implies that stablecoins are bank-like products and therefore should have to suffer the same regulatory burden as banks. But – if the definition of a “bank-like product” is one where savers and businesses can park funds – then so should ETF issuers, money market funds and so on. Why should they have to follow the same rules as banks?

Since Nichols is CEO of the ABA, we can assume he knows that banks are not heavily regulated because they take in deposits. It’s because they don’t safeguard the deposits, they lend them out, often to risky ventures. Conflating bank deposits backed by risky debt with assets 100% backed by government debt is deceitful.

(uncanny timing – a screengrab from the Financial Times on Wednesday, March 11)

So are claims that stablecoins could hurt community and regional banks and therefore also local economies and US GDP growth. These claims are largely coming from the same big banks that are aggressively expanding market share by setting up branches in local communities. The big guys are calling for regulation to protect the little guys while stealing their lunch.

This level of competition is not great for communities, nor for American taxpayers. For one, community banks generally pay higher interest on deposits than the big banks, because they have to be more competitive as they don’t have the “too big to fail” bailout (with taxpayers’ money) guarantee. Also, they tend to have deeper ties to the community, based on history and personal relationships. This means that their deposits are relatively sticky – at least until a big bank branch offers more bells and whistles. But community banks do more local lending, while a big bank branch is more likely to take in local deposits and then continue to lend mainly to the large multinationals, private credit firms, etc. If the big banks really wanted to protect “lending into the community”, they’d stay out of community banks’ territory.

I could go on – in fact, I think I will.

Blocking migration into stablecoins is not about maintaining bank capacity to lend at all. Data from the Federal Reserve shows that banks account for less than 30% of total lending into the economy – the rest comes from private credit, insurance firms, mortgage lenders and so on. Banks could lend more but there just isn’t the demand, per the roughly $3 trillion in excess reserves they hold at the Fed.

No, it’s about profit protection. Banks can take in deposits, pay almost nothing on them, and invest that money in loans, government or agency bonds, or park it at the central bank, earning a tidy spread. US banks reported aggregate net income of almost $300 billion in 2025, up 10% from 2024.

What’s more, this profit protection comes at the expense of taxpayers. Depositors lose out on potential earnings on their savings so that bankers can earn higher bonuses, further entrenching the financialization of the US economy. But even more egregious is the bankers’ suggestion of unequal treatment of American savers relative to foreign holders of dollar stablecoins, who will be able to earn yield on their balances (any limitations in the CLARITY Act would only affect US platforms). Where would this yield come from? The interest paid on the government debt that backs dollar stablecoins – interest that is ultimately paid out of public funds, i.e.. taxpayers’ money.

If banks truly want a “level playing field”, they should first look at the unequal protections among banks themselves. Smaller banks with limited FDIC coverage don’t have the same level of protection as the “too big to fail” set, the very same set that is now trying to take away their customers. And if they insist stablecoins can’t earn interest, how about a ban on deposit interest as well? It’s not as if private banks are safer than stablecoins backed by the US government.

Finally (for now, in the interests of time because there’s more, there’s more), a surge in stablecoin demand in the US would not siphon off deposits. It would probably reallocate them, to the detriment of smaller banks. Inflows into stablecoin issuers have to go somewhere – the large ones will use the large banks. And when they buy their reserve assets, the sellers of Treasuries have to put the money somewhere. Again, the large banks pretending to want to protect the small ones is disingenuous.

The bank lobby stance is just plain wrong on so many levels. It’s not so much the stablecoin interest we should care about – it’s the banks’ ham-fisted tactics that hint at a sinister strategy: suppress innovation they can’t control. This is not just about stablecoins, it’s about decentralized finance in general. At the same ABA event mentioned above, an executive actually said on stage:

“Holding payment stablecoins, creating liquidity in that DeFi world, like, that’s part of the crypto roadmap. And that’s not okay.”

Banks cannot be allowed to get away with their unreasonable bullying. If they win any ground here, it will be to the detriment of savers and smaller banks. And they’ll come for DeFi next.

✨ If you find these newsletters at all useful, would you mind sharing them with your friends and colleagues, and nudging them to subscribe? I’d appreciate it! ✨

Hong Kong banks and DLT innovation

From the other side of the world, here’s a different approach to distributed ledgers, blockchains and digital assets.

Hong Kong’s monetary authority (HKMA) has asked the region’s banks to conduct a review of their business model with digital assets in mind.

The circular makes clear it expects banks to re-think structures and operations rather than simply layer new tools over old processes. It also encourages banks to use the HKMA’s Supervisory Incubator for DLT to test new business models at small scale and under supervision.

Contrast this with the focus of US banks on deposit tokens (same activity on new rails).

What’s more, the HKMA request comes as the authority is gearing up to approve the first of the region’s stablecoin licenses by the end of the month – according to the South China Morning Post, these are expected to go to HSBC and a joint venture led by Standard Chartered.

And earlier this month, the HKMA signed a memorandum of understanding with the Shanghai Data Bureau and the National Technology Innovation Centre for Blockchain to explore and promote tokenized trade finance.

So, Hong Kong – a hub of global trade and a gateway into mainland China – is actively encouraging banks to embrace the potential of distributed ledgers and to consider how they can transform business models. It is doing so as two of its large banks are poised to issue approved stablecoins, and as the tokenization of trade finance by two of Asia’s most significant hubs moves into the mainstream.

I’ve written before about the geopolitical role of blockchain and its application – here’s another example of how smaller economic centres can leverage their relative agility to earn positions of greater relevance in the financial landscape of tomorrow, while today’s market leaders struggle with self-imposed constraints.

See also:

No, China is not banning tokenization (Feb 2026)

Hong Kong’s stablecoin geopolitics (Aug 2025)

Project Guardian: blockchain settlement meets global ambition (Mar 2024)

ASSORTED LINKS

(A selection of reads I came across this week that I think are worth sharing, not always about crypto or macro. I try to choose links without a paywall, but when I feel it’s worth making an exception, I specify.)

Francis Fukuyama probes what we mean by “Western civilization”, and points out that it’s not about a shared religion, given the long history of religious wars in Europe. He posits its about removing religion from politics. (What “Western Civilization” Really Means, Persuasion)

An utterly engrossing (and often funny) foray into why “Irish” equates with “magical” and “mystical” in so much of our literature and cultural references, and how this can be problematic. (Fantasy writers are weird about Ireland, Sithara’s Newslettara)

A brave attempt to weave together the various threads on the economic impact of AI, that results in a one of the least confusing narratives I’ve seen so far. Plus, some personal development advice to maximize luck when it shows up. (Schrödinger’s Economy, The Curious Mind)

We carefully scrub them from our writing in case anyone think it was created by an AI agent – and I confess I’ve never used them for personal taste reasons – but this episode of 99% Invisible comes to the defence of the em dash and explains why it became so popular. (The Em Dash, 99% Invisible)

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

For some reason I’m unaware of but a therapist would probably have some thoughts on, I found myself going down a Muppets music video rabbit hole the other day. A bit dated, perhaps, but they were so good. Here are a few of my favourites:

Mahna Mahna

Bohemian Raphsody

Fever, with Rita Moreno and Animal

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.