WEEKLY - Stablecoins are not all about dollarization

plus: the price of distrust, assorted links, nostalgia music and more

Hello everyone! Holy cow, what a week… I hope you’re all taking care of yourselves, and appreciating that we live in interesting times.

✨

If you speak Spanish and are interested in a less frequent, shorter update on developments in the crypto-macro intersection, you can subscribe to Cripto es Macro here.

✨

My American Banker op-ed this week (paywall, sorry!) looks at the recent boom in crypto credit card activity, and how it’s a step towards mainstream adoption, but what kind of adoption? What is the goal here? “Crypto cards are booming, but what they mean for the future is unclear”

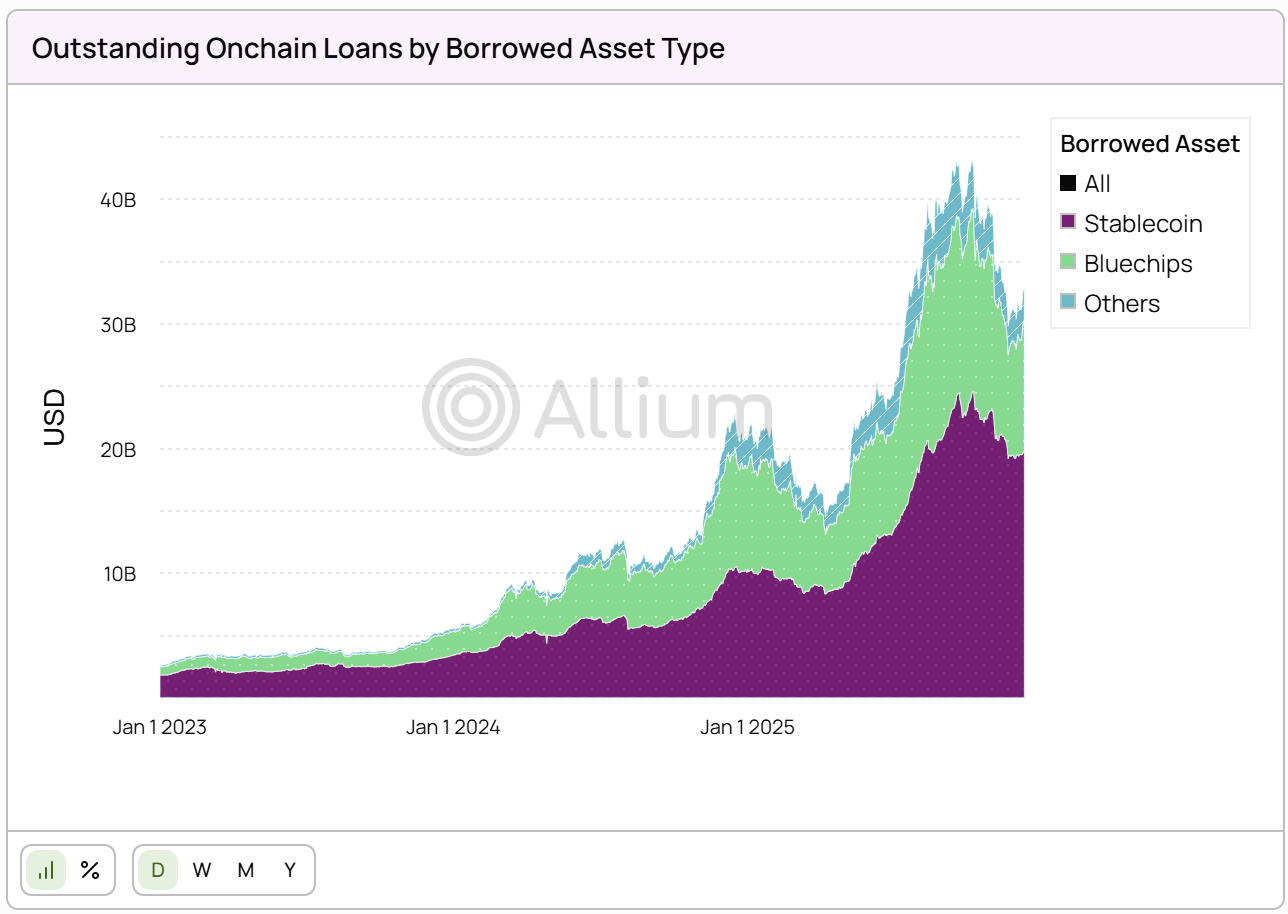

PUBLISHED IN PARTNERSHIP WITH: ✨ALLIUM✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

Our latest whitepaper published with Visa, Stablecoins Beyond Payments: The Onchain Lending Opportunity, examines how banks can access emerging credit markets. Looking at the data, outstanding onchain loans reached over $40Bn this year, with stablecoins making up more than half of borrowed assets.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

In this newsletter:

Stablecoins and geopolitics in Africa and the Middle East

The price of insularity

Assorted links: New Romanticism, film soundtracks, chef’s knives, EU bumbling, spy locations, tourism

Weekend: vintage soundtrack hit videos

If you’re not a subscriber to the premium dailies, I hope you’ll consider becoming one? You’ll get access to market commentary as well as adoption insight and industry trends. Plus, links and music recommendations ‘cos why not…

Some of the topics discussed in this week’s premium dailies:

Coming up this week: diplomacy, Supreme Court hearings, inflation

The script has velocity

Markets: yippy yet? Plus, the distraction effect.

Davos: The circularity of recognition

What the Davos set is afraid of

Markets: be careful out there

Stablecoins and geopolitics in Africa and the ME

Markets: no, BTC hasn’t “decoupled”

The price of insularity

Markets: heavy metal

Macro: steaming ahead

Stablecoins and geopolitics in Africa and the Middle East

A low-key announcement last week was surprisingly overlooked, given the significance of its potential impact. It’s to do with stablecoins, like so many headlines these days. But it’s also about regional and global alliances as well as the big-picture focus on digital tentacles and strategic flow-through.

The story starts with an unbanked population, pre-paid phone minutes and a widespread network of agents; it potentially ends with the dirham as the “reserve currency” of Africa while China cements its dominance in the continent’s mineral extraction and trade.

The key players are M-Pesa and the ADI Foundation, who last week announced a blockchain and stablecoin partnership. The stage is cross-border payments. And China is lurking in the background.

Player 1: M-Pesa

Back in the early 2000s, Safaricom – partly owned by Vodafone and the country’s leading telecommunications network at the time – noticed that people were starting to share pre-paid mobile phone minutes with relatives and also exchange them for goods and services. In 2005, it initiated a pilot with microfinance institution Faulu Kenya that would allow the repayment of microloans in instalments using airtime which could be bought in bulk from participating agents – the idea was to remove the need for borrowers in villages, where most of the loans were disbursed, to have to regularly travel into the city.

After receiving a no-objection letter from the central bank, the pilot pivoted from the exchange of airtime to the distribution of e-money. M-Pesa launched in 2007, offering mobile money accounts to anyone with a Safaricom phone number. Users could go to an agent (often just a hut on the side of the road) and exchange cash for an electronic balance, with deposited funds held in trust at a commercial bank for 1:1 backing (not all “stablecoins” require a blockchain, who knew). At the public launch in 2007, anyone with a Safaricom phone number was able to open a mobile money account.

Growth was astonishingly fast as, at the time, almost 75% of the population did not have a bank account – M-Pesa offered a convenient alternative. (I wrote about this for CoinDesk back in 2017 – how time flies!)

After initial resistance and intense lobbying from the banking industry to get M-Pesa either regulated like a bank or shut down entirely (sound familiar?), official support for the project’s financial inclusion potential eventually encouraged banks to focus on the growth opportunities: more people involved in digital banking, even on a different system, meant a greater need for onramps as well as demand for loans and other banking services. What’s more, M-Pesa changed Kenya’s banking industry for the better, forcing banks to compete by lowering account thresholds, dropping transfer fees and accelerating the development of mobile banking. (I wonder how many US banks are familiar with the M-Pesa case study.)

The growth rapidly seeped into neighbouring nations. In 2008, M-Pesa expanded into Tanzania, a couple of years later into South Africa, and today operates in eight African countries.

An interesting twist is M-Pesa’s rejection and then embrace of “crypto”. Just as banks initially opposed the idea of competition from Safaricom, the telecom operator hated the idea of competition from blockchain networks and moved to have them shut down, rejecting any form of collaboration and denying blockchain businesses access to its network.

But in December, reports emerged that M-Pesa was pivoting on this strategy via a partnership with the Abu-Dhabi based ADI Foundation.

Player 2: the ADI Foundation

Created in 2024 to build compliant digital asset infrastructure for governments, institutions and retail, the ADI Foundation is backed by the digital arm of the second-largest listed entity in the MENA region, International Holding Company (IHC). The head of IHC is Sheikh Tahnoon bin Zayed Al Nahyan, who is also chair of the UAE sovereign wealth fund, its two largest AI companies, the Emirates’ largest bank as well as a few other technology and holding companies. In addition, he’s the UAE’s National Security Advisor as well as its Deputy Ruler and brother to the President. Last March, he was hosted at the White House where he reportedly met with the US Treasury Secretary, the head of the CIA, Jeff Bezos and other global movers – the man has clout. And I should mention that one of his investment firms last year bought $2 billion worth of USD1, the stablecoin issued by World Liberty Financial (controlled by the Trump family), which was then used to buy a stake in Binance. I know, my head is spinning just writing this.

Last month, the ADI Foundation launched the mainnet and token of ADI Chain, a compliance-oriented EVM-compatible layer-2 built on the zkSync stack. A few days later, it signed MoUs with BlackRock, Mastercard and Franklin Templeton to extend use of digital asset infrastructure in the region.

Launch of a dirham-backed stablecoin is expected in coming weeks, to be issued by the Emirates’ largest bank, First Abu Dhabi.

The stage: cross-border payments

Under the terms of the above-mentioned deal, M-Pesa will integrate ADI Chain into its network and facilitate movement of the dirham stablecoin across its 60 million accounts in eight countries. That’s significant potential stablecoin scale, from a mobile money business already deeply entrenched in African money flows.

The advantage? A widely accepted token for cross-border transfers. The African payments landscape is fragmented, with payments to even neighbouring countries often met with the considerable friction of intermediaries and relatively high costs, especially given the illiquid nature of most currencies on the continent.

The dirham, in contrast, is both relatively liquid and stable, given its considerable international flows and its peg to the dollar. Put differently, it is a better “store of value” than local currencies. But it is not yet widely accepted as a settlement currency in sub-Saharan trade.

Could this change? The UAE is the fourth largest foreign investor in the region, and has plans to ramp up its involvement. Could the dirham eventually become a de facto “reserve currency” for the region?

Stablecoins are already widely used in the region – mainly USDT – but there is as yet no widespread network “compliant” enough for official acceptance. ADI Chain hopes to become that network, leveraging the influence and reach of M-Pesa and offering a deeper integration with a global financial centre.

Could it be a threat to USDT use in the region? I doubt it – most current users will probably continue to find dollars preferable to dirhams, and could be wary of the “compliance” angle. But new corporate and even sovereign users could find the ADI option a palatable onramp.

So, the ADI/M-Pesa deal is significant, given the potential volumes and connectivity. But there’s more going on. Stepping back, here we have another example of the geopolitics of stablecoins.

In the background: China

To start with, we have the UAE seeing an opportunity to expand its financial services, plugging into an already extensive network and offering a gateway for businesses on the continent to access new rails and new markets.

It’s ingenious, especially when you consider the UAE’s role in global payments and its work on becoming even more significant as a finance node, leaning in to its inadvertent branding as “the capital of capital”. Given its origins as a trading post and its key geographical location, it has a long history of multi-currency flows, and its ability so far to stay out of the grand power tussle around global trade makes it a relatively trusted partner for most. Some of India’s imports of Russian oil, for instance, are settled in dirhams. Meanwhile, the UAE’s aggressive work on blockchain infrastructure build with regulatory support represents investment in the currency flows of tomorrow.

Until Saudi Arabia joined in mid-2024, the UAE was the only non-Asian member of the mBridge platform, a multi-CBDC initiative developed by its central bank along with those of China, Hong Kong and Thailand. China is the UAE’s largest trading partner, the UAE is China’s largest export market in the Middle East (COSCO has a terminal at Khalifa Port), and there are reportedly more than 15,000 Chinese firms operating in the Emirates. Last March, China’s Cross-Border Interbank Payment System (CIPS) and the UAE Central Bank signed an MoU to enhance cross-border payment cooperation. And in November, the UAE and China completed their first cross-border CBDC payment, not on mBridge but via a separate bilateral platform.

So, the UAE is going full speed ahead on enhancing its global finance role. A significant leg of this lies in developing digital asset infrastructure to be used not just by institutions and individuals in the region, but by sovereigns and businesses anywhere that want to transact with or via the Middle East. Of course, large US institutions will want to participate in this rollout, given the potential volumes on the table. And the door will be open to US participation, especially since the UAE really wants a guaranteed supply of US-made AI chips.

But the UAE is also hedging its bets and leveraging its role as a long-standing anchor between hemispheres. It is deepening its digital payments development with its largest trading partner, China. And at the same time, it is forging paths into the potentially vast field of African cross-border payments via stablecoins and mobile accounts.

Bear in mind that China is by far the largest foreign investor in mining and other resource extraction in sub-Saharan continent, and you can see not just new networks taking shape, but also the long game of how stablecoins and CBDCs can shape the realignment of global power.

Perhaps you thought that stablecoins were all about dollarization?

The price of insularity

Earlier this week, I shared some charts from the World Economic Forum’s Global Risks Report 2026, a document usually timed to coincide with the annual gathering in Davos.

Another survey with similar timing is the annual Edelman Trust Barometer. I’ve covered this regularly over the years as it chillingly records the “on-the-ground” mood which tends to be more relevant for what’s ahead than the worries of the Davos elite. This year’s report is a continuation of the theme, with some interesting variations.

For background, the survey canvasses almost 34,000 respondents across 28 countries, making it a much broader sample than most. Questions focus on opinions of societal institutions: government, business, media and NGOs. Responses are then compared to previous editions to extract trends, and an overarching theme is selected: this year, it’s “insularity”, defined as a reluctance to trust anyone who’s “different”.

As usual, the highest trust score goes to China – that is, Chinese respondents recorded the highest trust levels in their institutions (you may not trust Chinese institutions, but Chinese people do). This year, the top rank is tied with the UAE. Also as usual, Japan, the US, the UK and much of the EU are in the bottom range, signalling overall “distrust”. Developing countries on the whole scored much better than the developed world. Among Western nations, the Netherlands yet again comes out top on the trust barometer.

(chart via the 2026 Edelman Trust Barometer)

Of course, we can quibble about the scores and shriek in surprise at some, but we have to remember that scores are decided by citizens of the involved countries, not by observers, and different cultures have different priorities. It’s the shifts that are more relevant here.

There is some positive news:

Overall trust increased slightly in all institutions except NGOs – this builds on last year’s slight increase, after a few years of depressing results.

(chart via the 2026 Edelman Trust Barometer)

But, on the whole, the takeaway is of a global society entrenched in fragmentation and echo chambers:

We are living in an insular world – 70% of respondents would be “unwilling or hesitant” to trust someone who does not think like them. This is most acute in Japan (90%!) followed by Germany, least an issue in India and the UAE.

Meanwhile, the percent of respondents who get information from sources with a different political leaning has dropped, with significant falls in 20 of the 28 surveyed countries.

And the share of respondents convinced that “foreign actors” spread disinformation rose in all but three of the 26 countries eligible for this question, reaching all-time highs in more than half. That’s unsurprising, but also alarming.

More than a third of employees say they would work less hard if their manager did not share their political beliefs. Identity is more important than getting ahead? That can’t be good for economic growth, nor for employment prospects given the potential alternative of less contentious AI workers.

The same percentage believe the number of foreign companies operating in their country should be reduced.

Low-income respondents have always been less trusting of institutions than high-income respondents – understandable, but the gap between the two groups is widening (from 6 points in 2012 to 15 in the latest report). What’s more, the gap is at its widest in the US (29 points).

Almost 60% of respondents feel some degree of “grievance”.

What does this mean for markets? The message is not just about insularity – it’s also about the unwinding of globalization as we seek comfort in the familiar even if it means less prosperity. This will have consequences for both inflation (as the cost savings from globalization are lost) and growth.

We also have a flashing arrow pointing to deepening political polarization, which always weakens trust in democracy and leads to greater social unrest. We saw that play out in 2025 with violence on the streets in cities around the world – unfortunately, this is likely to increase in 2026, potentially compounded by electoral upsets. Among significant economies, this year brings mid-term elections in the US, general elections in Brazil, Japan, Sweden and Denmark (geopolitically significant), as well as municipal yet potentially high-impact elections in France, Germany and the UK.

The biggest takeaway, however, has to be this: Trust in institutions is universally regarded as essential for the functioning of society – and yet, for a while now, it has been doing poorly in the West, better in the East. Whether you think this is correct or not is irrelevant; what matters is what those on the ground think. And, leaning into this year’s theme of insularity, we can ignore measurements and conclusions we don’t agree with – or, we can ask ourselves in what way could we be wrong. We can also factor in that the world is complex and our personal lens is usually narrow, and accept that firm yet untested assumptions can so easily cloud judgement.

See also:

What the Davos set is afraid of (Jan 2026)

Trust: more than just surveys (Jan 2025)

ASSORTED LINKS

(A selection of reads I came across this week that I think are worth sharing, not always about crypto or macro. I try to choose links without a paywall, but when I feel it’s worth making an exception, I specify.)

Ted Gioia on the New Romanticism, which I am totally here for. It’s about the questioning of the meaning of life, putting the human above the machine, the value of enchantment. An antidote, if you will, to the techno-utopianism we’re drowning in. (25 Propositions about the New Romanticism, The Honest Broker)

Daniel Parris tracks the history of film soundtracks and shares some fascinating charts that show which songs have been most used in films, which movie music hits spent the most time in the charts, and more. Some surprises here, plus you’ll probably be humming “Night Fever” for the rest of the day. (The Rise and Fall of the Hollywood Movie Soundtrack: A Statistical Analysis, Stat Significant)

An oddly compelling insight into the world of flea markets, auctions and chef knives, and a reminder that there is treasure in odd places if you know how to look. (No knives, only cook knives, A Box of Old Knives)

A cathartically scathing summary of the bumblefest that is EU diplomacy. (Borrowed Time, Doomberg – paywall)

One of the many luscious features of the first season of The Night Manager was the locations – apparently the second season, which I have not yet seen but which is at the top of my viewing list, does not disappoint in that respect. Conveniently, even if only to inspire travel daydreams, the Financial Times shared some details of where key sections were shot, in some instances down to the address. (A set-jetter’s guide to: The Night Manager, The Financial Times – paywall)

And speaking of luscious locations, Bloomberg has an article that hits close to home, about the floods of tourists making travel less fun – my city Madrid doesn’t have the issues Barcelona has, but downtown these days is often uncomfortably crowded. Tourism can bring in good money, but often at a painfully high cost to quality of local life. (The World Is Drowning in Tourists. Who Should Pay the Price?, Bloomberg – paywall)

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

Above, in Assorted Links, you’ll find a link to an article about soundtracks that sent me down the rabbit hole of old-school music videos, digging up some absolute gems I hadn’t seen in, oooo, decades. Here are three good ones from that journey down nostalgia lane, but there is so much overflow and I had so much fun doing this, I’ll probably share more in coming weeks:

Stayin’ Alive, by The Bee Gees (from Saturday Night Fever) - The hair! The teeth! And a great beat.

Summer Nights, by John Travolta, Olivia Newton-John et. al. (from Grease) – just sublime, keep an eye on the choreography.

Footloose, by Kenny Loggins (from Footloose) – you know you want to dance to this.

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.