WEEKLY - stablecoins + the new financial landscape

also: crypto in Iran, assorted links and more

Hi everyone! I hope you’re all well and making sure to step away from screens when you can.

✨

If you’re not a subscriber to the premium dailies, I hope you’ll consider becoming one. You’ll get deeper dives in crypto-macro developments, some market commentary as well as adoption insight and industry trends. Plus, links and music recommendations ‘cos why not…

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

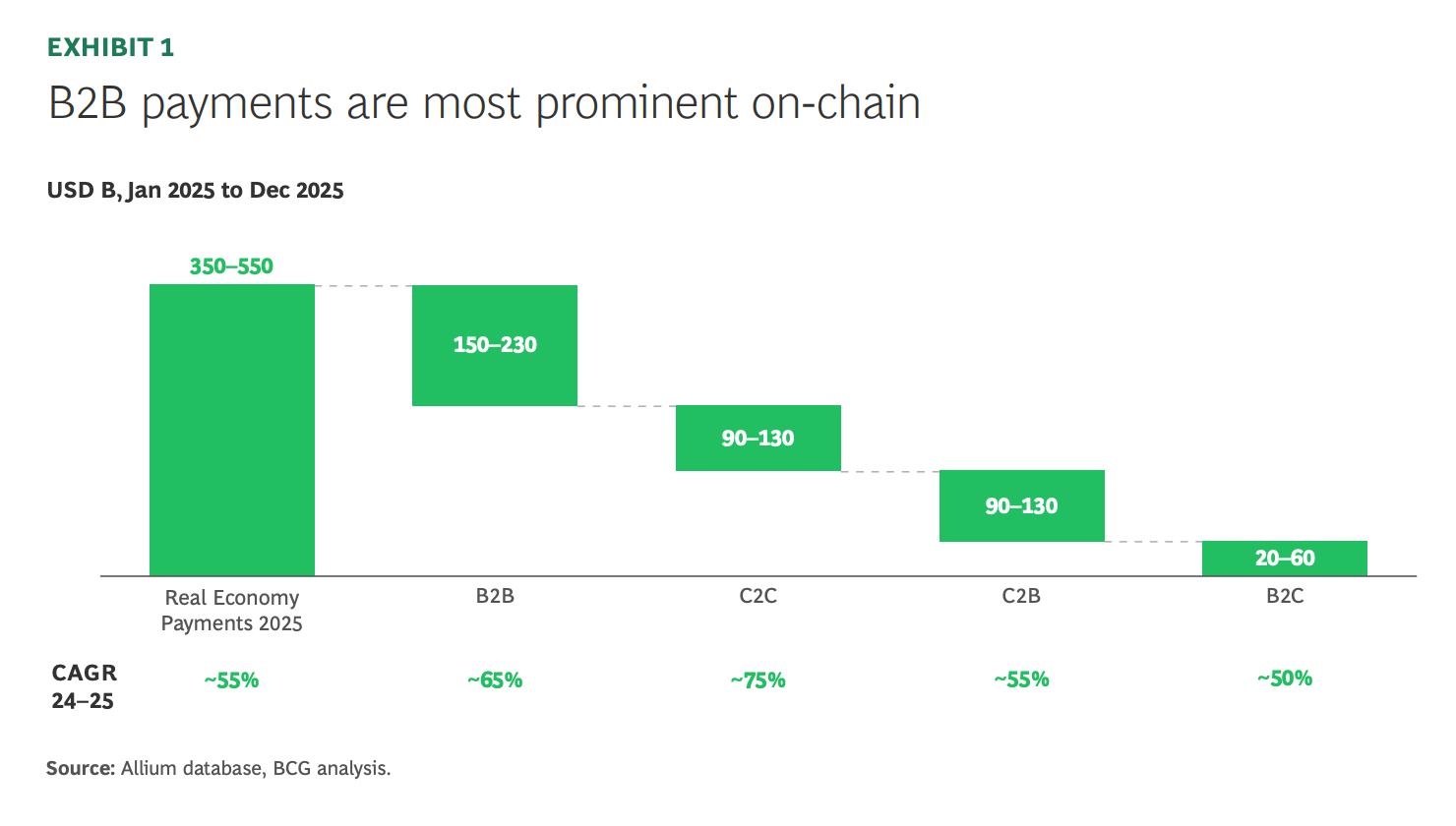

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

✨

My op-ed in American Banker this week (paywall, sorry!) takes a walk through history and at how the origin of stablecoins points to an overlooked vector of growth. “The origin story of stablecoins offers a hint to their future uses”

✨

In this newsletter:

Kraken, the Fed and the new payments landscape

Stablecoin payments: some surprising details

Crypto in Iran

Assorted links: Normality, music streaming, being human, happiness data, video vs audio, over-measuring.

Weekend: shared in hope, some of my favourite Iranian music videos

Some of the topics discussed in this week’s premium dailies:

Coming up this week: China’s political meetings, US jobs + activity, Merz in US

Monday mood: a turning point

Markets: the reaction

Macro: PPI

Crypto in Iran

Markets: the shrug

Markets: BTC and liquidity

Stablecoin liquidity: the risk to banks

Bitcoin adoption

Markets: a momentum shift?

Kraken, the Fed and the new payments landscape

Stablecoin payments: some surprising details

Macro: US jobs

Macro: US services activity

CBDCs: an update - US, EU, China, India, Japan

Markets: slippery oil

Macro: US jobs, ouch

Kraken, the Fed and the new payments landscape

This past week, we saw yet another seemingly tentative regulatory move that masks a huge step towards a new financial system:

Kraken Financial, a Wyoming-chartered bank owned by crypto platform Kraken, has been granted the first Federal Reserve master account awarded to a digital asset bank.

This will enable it to hold reserves at the US central bank and connect directly to core US payment rails without relying on intermediary banks.

The move is temporary for now, granted for a period of one year, and comes with limitations: Kraken can’t earn interest on its Fed balance, nor will it get access to daylight overdraft privileges and overnight borrowing.

The big deal here is that Kraken gets access to bank-quality payment rails with the ultimate security of a central bank backstop, without being a traditional deposit-taking bank. Higher security means cheaper pools of settlement liquidity for stablecoin transfers.

Stepping back, this raises the question of why banks have monopolized top-level payment rails for so long. An obvious answer is that banks are where money is held, so it follows they would originate most payments.

Only, that’s not true anymore. Banks no longer have a monopoly on deposits – these are migrating away from the centre towards more agile fintech services, and towards stablecoin accounts. And banks have never had a monopoly on electronic payments – as far back as the late 19th century, Western Union was able to take advantage of banks’ reluctant attitude towards innovation.

Yet, until now, banks have had a monopoly on Fed access. Today’s payments landscape contains a dizzying array of non-bank digital services, in constant evolution. But virtually all electronic payments have to touch bank credit at some stage of their journey.

This may be “traditional”, but the institutional marriage between payments and credit introduces fragility.

Banks rely on intraday and overnight credit with each other for settlement. And history has shown that, at times of systemic stress due to loan defaults and collapsing credit structures, payment networks can freeze. Even outside a widespread banking crisis, issues with any one institution can create payments mayhem as network participants are reluctant to enter into even short-term settlement commitments.

Now, however, the Federal Reserve is contemplating opening the quality-payments door to institutions that don’t lend. At all.

Put differently, this is a move to separate the payments function of financial institutions from the lending function. Of course, if banks no longer control the payments system, they lose economic power – no wonder the lobbies are up in arms over this.

It’s a gutsy and insightful move from the top bank regulator, which will not only boost stablecoin liquidity and calm concerns about run risks; it will also move the US towards a financial network less reliant on bank lending and more reliant on government debt.

In case any of you are thinking that the one-year timeframe means the Fed is not serious about this move, let’s remember Governor Chris Waller has been talking about the idea of “Skinny Fed Master Accounts” for some time. And that the Bank of England has proposed something similar: allowing “systemic” stablecoin issuers central bank access. I doubt this is a coincidence.

The approval of the Kraken master account is no doubt the first of several – keep an eye out for similar recognition of Anchorage and Custodia’s applications, there are probably others out there I’ve lost track of.

Bottom line, the structure of global payments is changing. Stablecoins are a key part of the redesign. And it feels like the shift is accelerating.

See also:

Crypto: a win for liquidity (Feb 2026)

✨ If you find this newsletters interesting, would you mind sharing with friends and colleagues and nudging them to subscribe? I’d appreciate it! ✨

Stablecoin payments: some surprising details

Whatever you thought you understood about stablecoin payments, a new report is out that will probably change some of your assumptions. Compiled and written by Allium (sponsors of this newsletter, but that’s not why I’m highlighting it), the report breaks down stablecoin use case, geographies, networks and volumes, with several surprises.

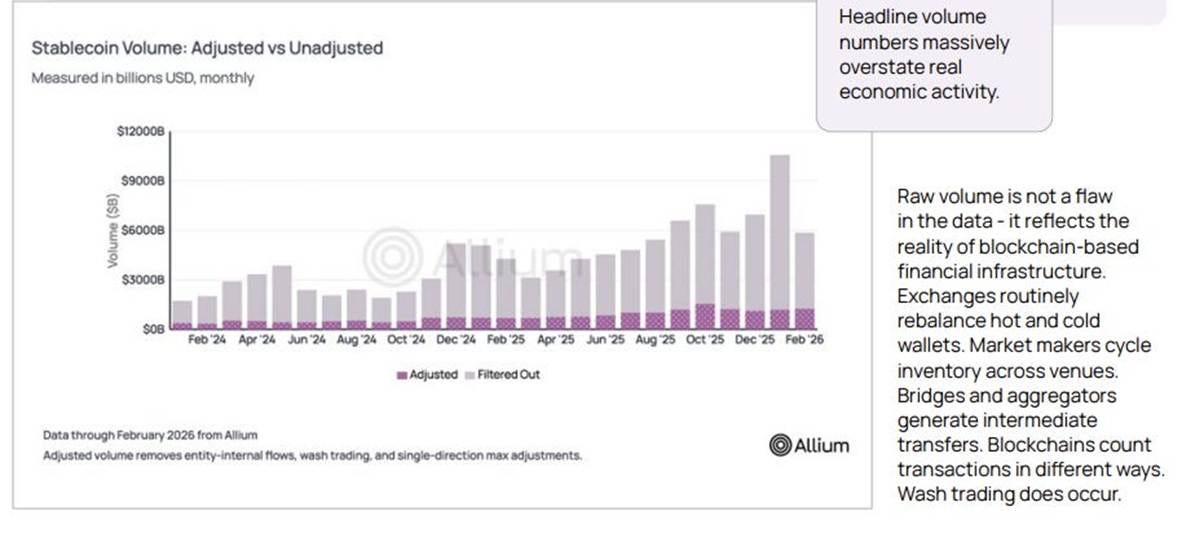

One is just how much work is needed to tidy up blockchain data. Anyone can see aggregate moves of onchain assets, but the raw data does not discriminate between useful (transfers between entities) and irrelevant (transfers between addresses held by the same entity) information. However, pattern parsing, label heuristics and rigorous filtering can extract the economically significant transactions.

(all charts in this section by Allium)

This filtering shows almost 90% growth in “real” stablecoin activity (adjusted monthly transfer volume) over the past year.

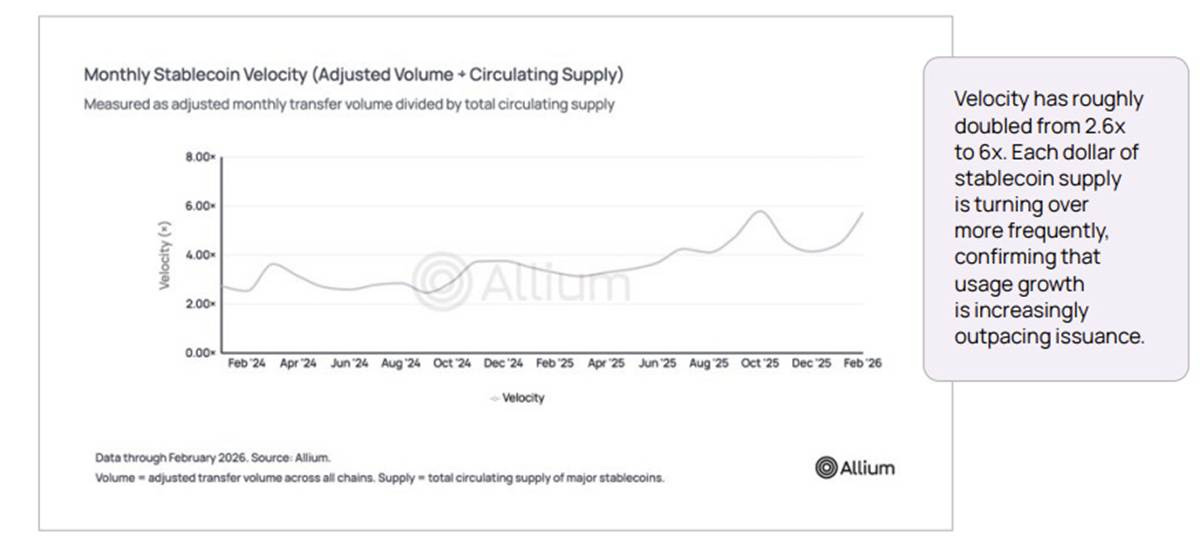

Comparing the growth in adjusted transfer volume growth to that of circulating supply, we see that velocity (the number of times each stablecoin moves in a given month) is increasing, suggesting a deepening utility.

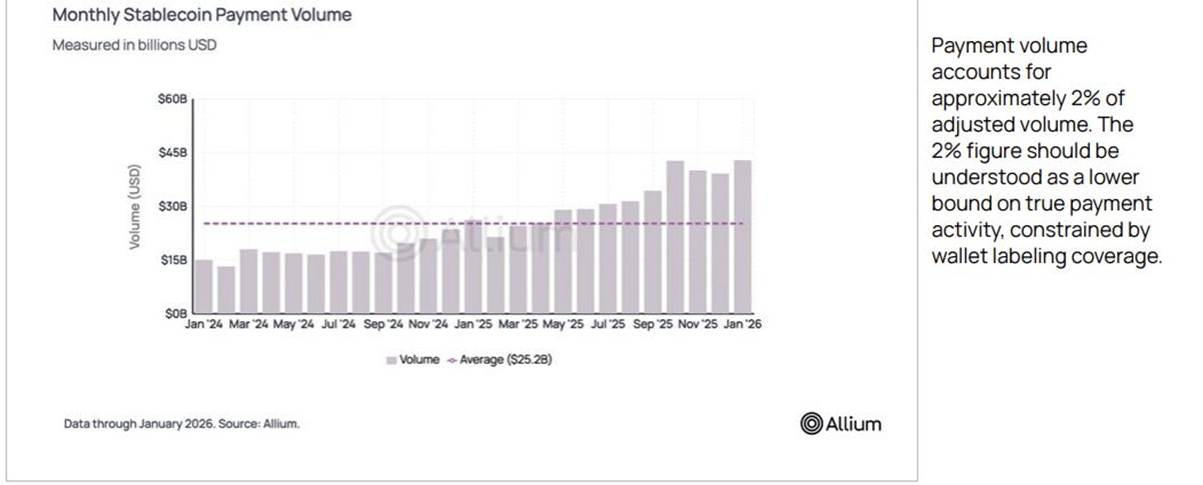

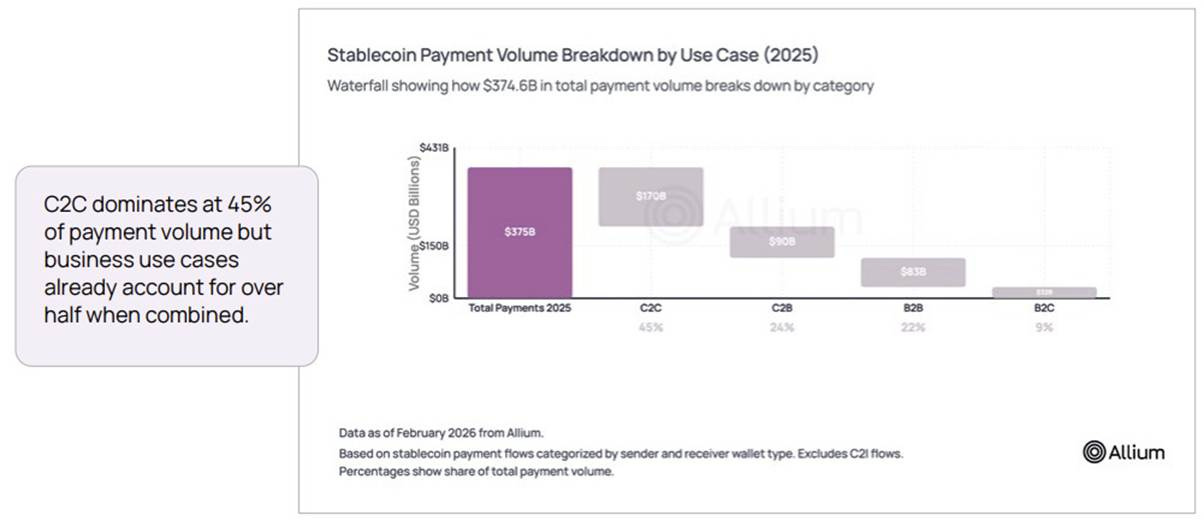

Further filtering shows that the volume of stablecoin transfers for payments is around 2% of the total, with the rest presumably for crypto trading settlement. What’s more, this segment has shown persistent growth over the past couple of years, reinforcing the deepening utility.

This data can be further filtered into payment categories: surprisingly, consumer-to-consumer (C2C) transfers account for the largest channel, up 53% last year – I would have thought it would be business-to-business (B2B) for cross-border commerce. That category came in third, but still up 87% in 2025. Interesting to see that consumer-to-business (C2B) stablecoin payments jumped over 130% last year.

Another big surprise: stablecoin payments are not mainly for cross-border activity. There’s some of that, but most transfers (over 80%) stay local, with the APAC region accounting for the most volume. What’s more, cross-border flows have declined as a percentage of the total, from 44% at the start of 2024 to just over 25% at the end of 2025. This further confirms a deepening of utility.

The report contains many, many more insights than I can share here – it’s worth a read. My big takeaway is the profile of those using stablecoins for payments is more complex than most realize: it’s not just about cross-border, and it’s not just about B2B. What’s more, different users will have different reasons for preferring stablecoins over traditional payment rails, and we will see these reasons continue to evolve as services mature and diversify.

Crypto in Iran

In times of war, it is a challenge to “follow the money”, and yet the task can reveal much about how finance works in times of stress. The challenge also applies to crypto movements, despite the supposedly transparent nature of onchain transactions. Yet forensics can extract enough data to draw some conclusions as to the utility of crypto for those outside the protection of “traditional finance”.

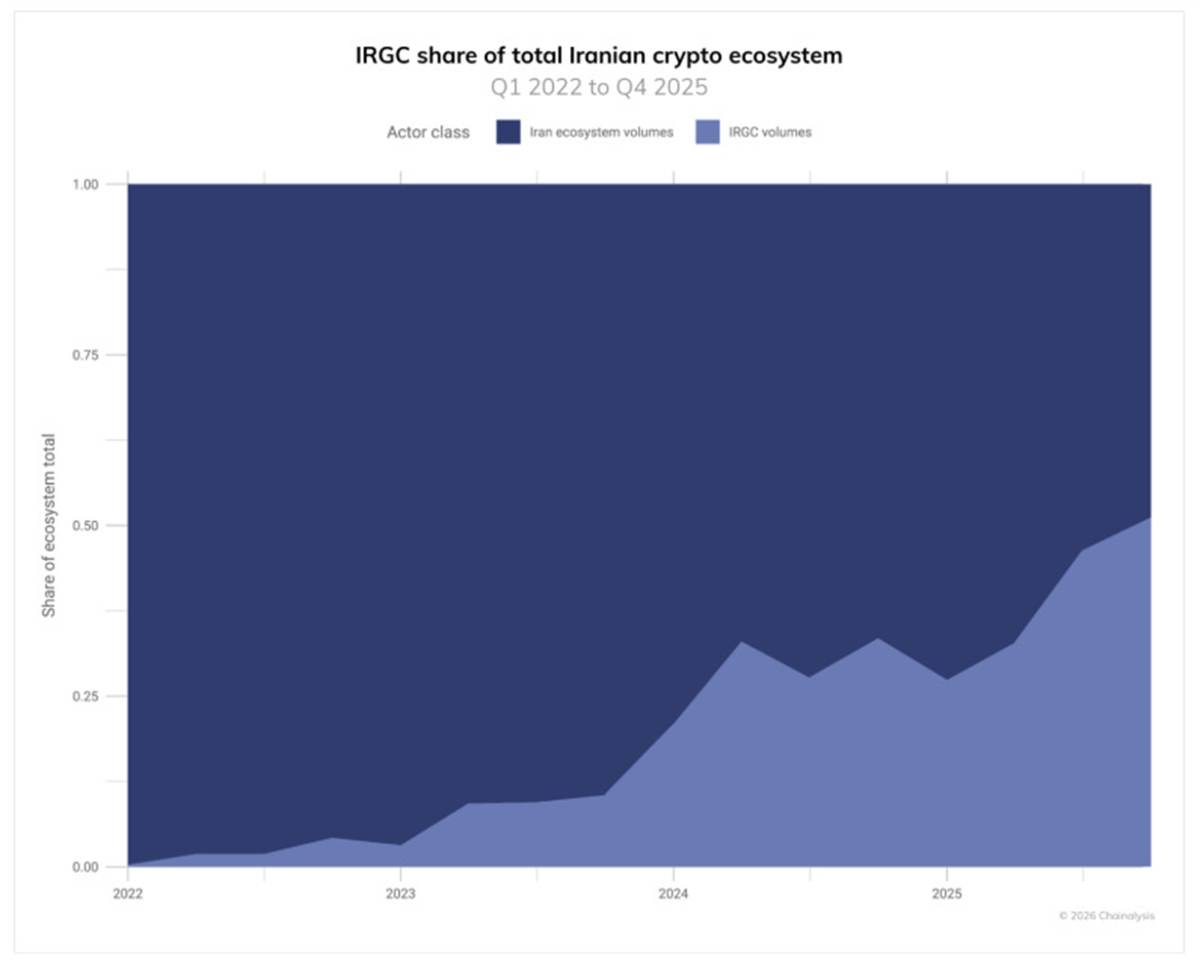

One obvious use case is for sanctions evasion. According to Chainalysis, onchain transactions attributed to the Islamic Revolutionary Guard Corps (IRGC) have surged over the past couple of years, and now account for more than half of crypto activity in Iran – what’s more, this is probably a low estimate given that the sum only includes addresses known to be associated with the force.

(chart via Chainalysis)

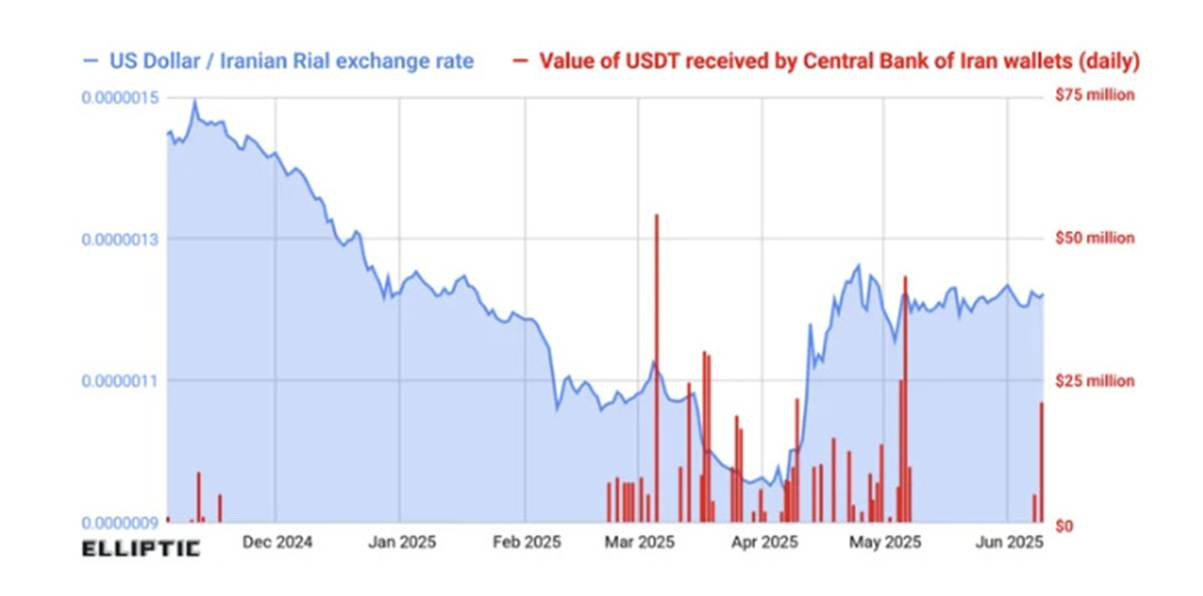

And Elliptic recently reported that the Central Bank of Iran accumulated over $500 billion worth of USDT over the first half of last year, presumably to finance trade and to support the plummeting currency (it seems to have helped).

(chart via Elliptic)

The other obvious use case is as a sovereign store of value, protection against a weakening currency whose value against the US dollar has more than halved over the past year, and that is worth roughly 15% what it was five years ago.

What’s more, Bitcoin is one of the only stores of value that is easy to transport, important in the face of expected unrest and the possible need to flee.

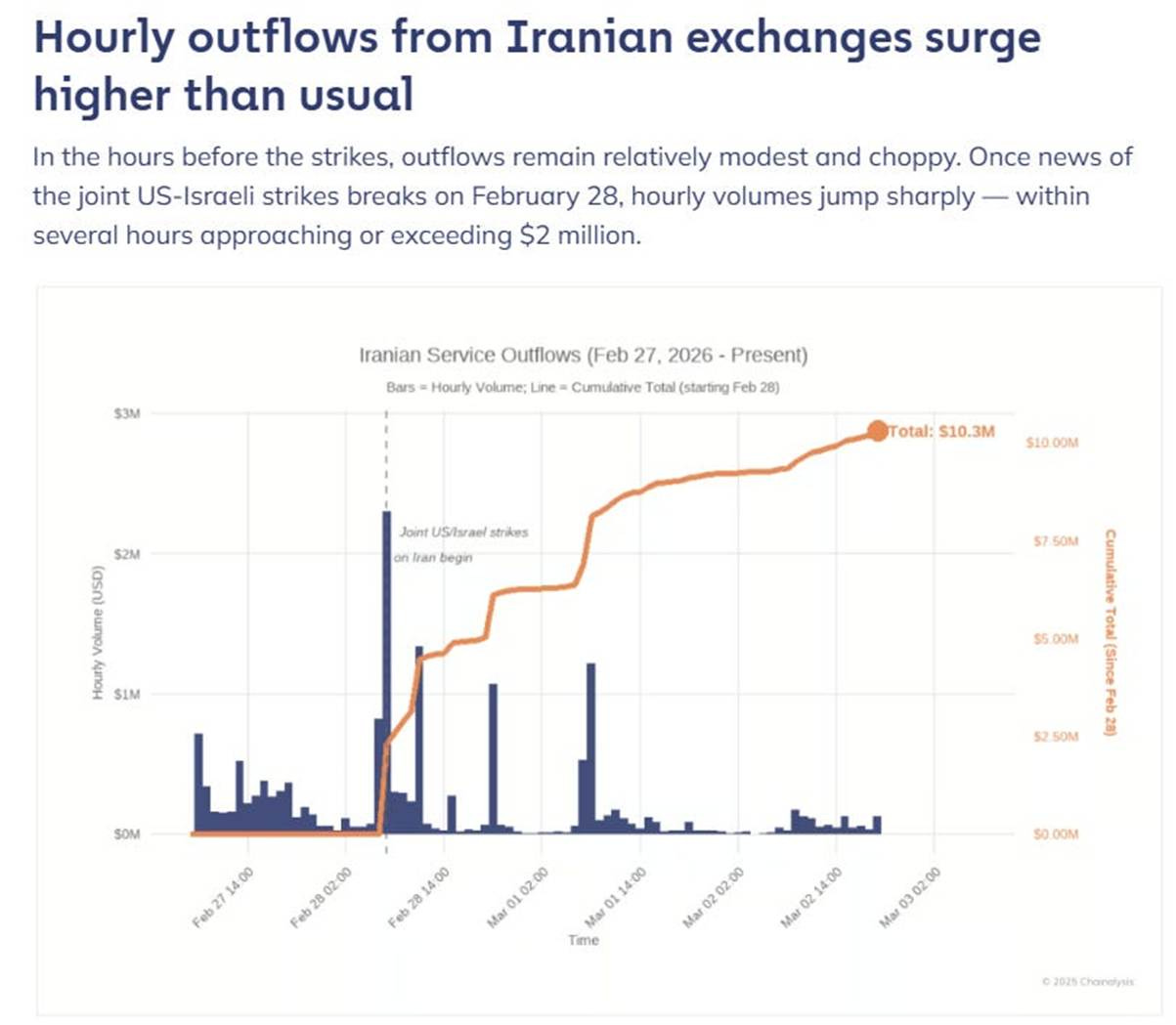

Indeed, onchain data shows a surge in outflows of Bitcoin from Iranian platforms in the hours following the airstrikes last Saturday.

(chart via Chainalysis)

The bulk of these went to “other wallets”, many of which are most likely self-hosted wallets as Iranians took custody of their assets for greater security. But “other wallets” could also mean new wallets created by the exchanges to shuffle holdings for security purposes – this would explain the large size of some of the transfers.

(chart via Chainalysis)

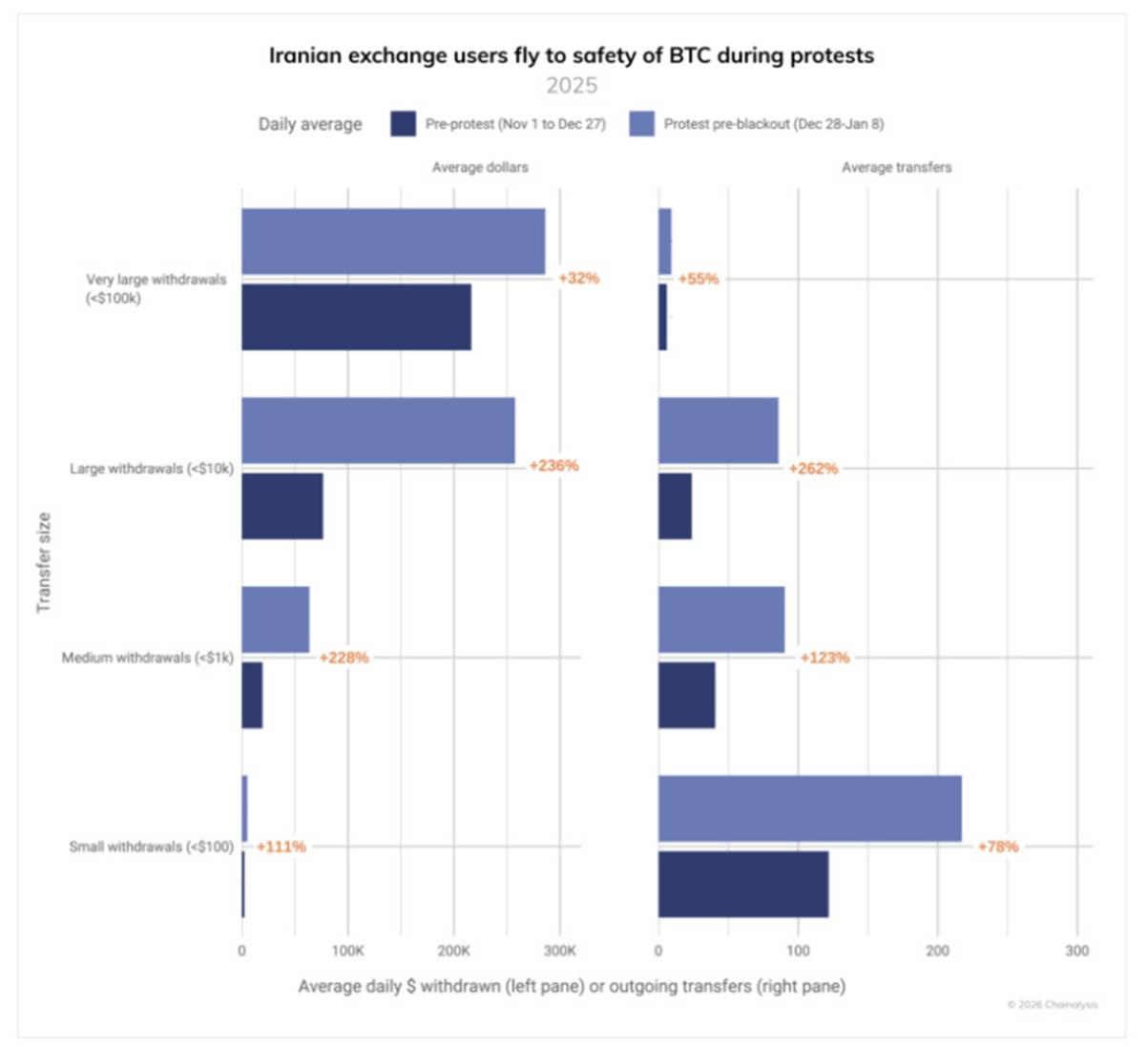

Looking at the surge in withdrawals at the start of the protests, Chainalysis shows that most outgoing transfers have been small – this is most likely retail users protecting their savings.

(chart via Chainalysis)

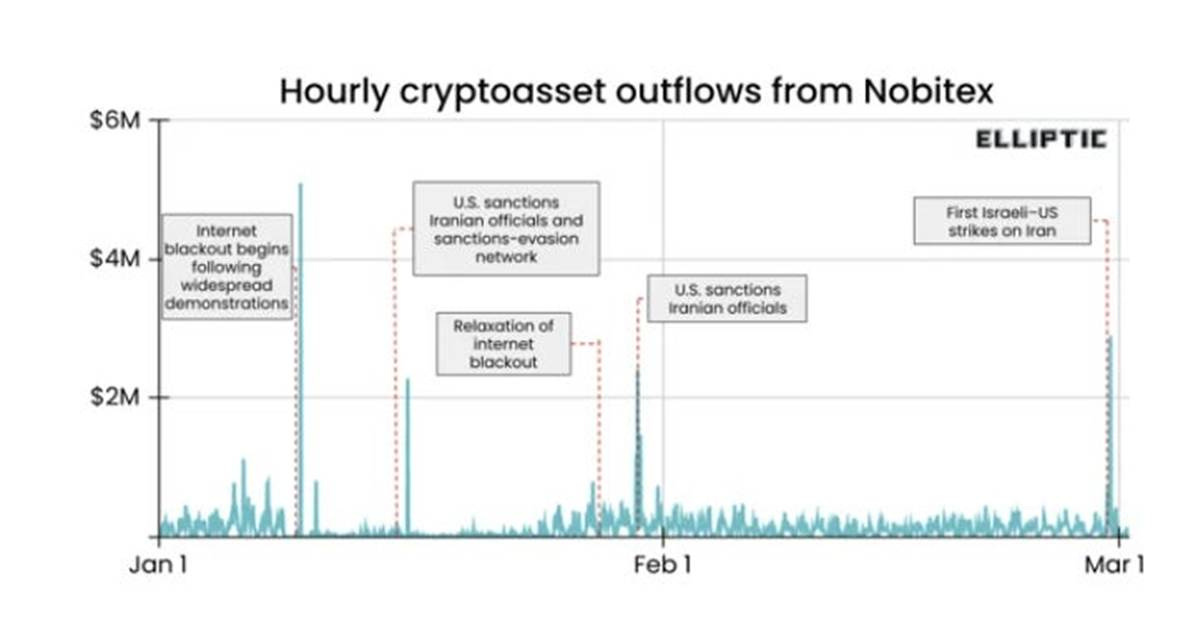

Intriguingly, it turns out that internet blackouts don’t necessarily stop crypto activity. The below chart by Elliptic shows hourly outflows from Nobitex, Iran’s largest crypto exchange – they spiked after disruptive events but didn’t flatline when online access was restricted. Perhaps some connections are kept open? Note the surges after the US sanctioned certain Iranian officials. Or perhaps there are “guerrilla” workarounds – most transfers during the blackout were small.

(chart via Elliptic)

In sum, for the “crypto is useless” crowd, here is further evidence that crypto is an alternative system. In some regions, this is not just useful, it’s existential. We can’t deny it is often used to avoid international law. But even more often, it gives financial sanctuary to civilians caught up in punitive circumstances not of their choosing. And while many in privileged financial circumstances may not approve of its use, attempts to stop it from acting as an alternative have time and time again proved futile.

ASSORTED LINKS

(A selection of reads I came across this week that I think are worth sharing, not always about crypto or macro. I try to choose links without a paywall, but when I feel it’s worth making an exception, I specify.)

Rodrigo Brancatelli on the barbell of American culture and how “normal” isn’t normal anymore. (They Killed Normal and Called It Progress, Found Object)

Joel Gouveia on how, even aside from how punitive the system is for artists, the economics of music streaming just don’t work. (The Death of Spotify: Why Streaming is Minutes Away From Being Obsolete, The Artist Economy)

Ted Gioia dives into the amazing story of how Zen and the Art of Motorcycle Maintenance was written, its philosophy of quality and what that says about being human in a machine world. (The Real Story Behind ‘Zen and the Art of Motorcycle Maintenance’, The Honest Broker)

What makes us happy? Many of us have read the literature, seen the diagrams, heard the anecdotes. But few have tried to plug happiness findings into the bigger societal picture, and even fewer have done so via a charming interactive graphic. (Happy map, by The Pudding)

Anil Dash warns that the “corruption” of video content – the lack of privacy via tracking, the potential for censorship via concentrated platform ownership, the clickbait scramble for eyeballs – will destroy podcasting’s open and listener-first neutrality. Why (Apple’s Move to video could endanger podcasting’s superpower, Anil Dash)

A podcast recommendation: in this Plain English episode, Derek Thompson and C. Thi Nguyen talk about the perils of over-measuring, and how goals can detract from purpose. (How Metrics Make Us Miserable, Plain English)

HAVE A GREAT WEEKEND

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

Shared in the fervent hope the war is over soon, here are some of my favourite reminders of the rich Iranian music scene:

A moving multi-artist rendition of the Baraye anthem

Quirky and catchy, by Eendo

I’ve shared this one before, but in case you missed it – Khooneye Ma, by Marjan Farsad

If you find Crypto is Macro Now useful, would you mind hitting the like button? ❤ I’m told it feeds the almighty algorithm.

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.