WEEKLY – stablecoins vs credit, the Bliss trade and more

Plus: assorted links, a music video and more

Hello everyone! I hope you’re all doing well and adjusting to the change in season, wherever you are. The flowers here tell us it’s still spring, but the temperature seems to think it’s summer.

You’re reading the free weekly send of the premium daily Crypto is Macro Now, where I re-share a couple of the week’s posts and add some non-crypto and non-macro links since it’s the weekend. 🌼

On Thursday, I was a guest on Steven Ehrlich’s Bits & Bips: The Interview show, you can see the playback here (weirdly, they got my title wrong, I haven’t been Head of Market Insights at Genesis Trading for a long time).

Production note: It’s Memorial Day in the US on Monday, and since most of you will be taking the day off, so will the daily premium newsletter. ☀ I’ll share the usual Monday features on Tuesday.

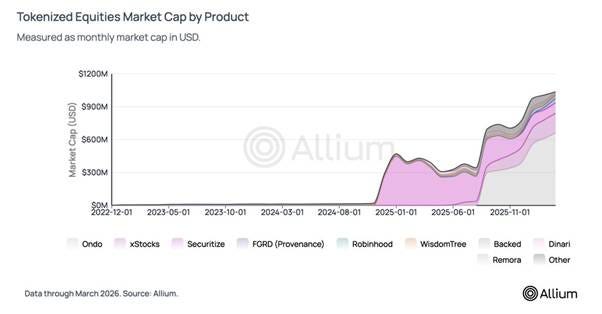

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

In this newsletter:

Stablecoins: separating payments from credit

What the Bliss Trade has to do with crypto

Assorted links: wokeism, niceness, cultural heritage, book signalling, art plunder

Weekend: Cultural heritage

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

Some of the topics discussed in this week’s premium dailies:

Coming up this week: PMI, primaries, Nvidia, G7

Monday mood: Politics, moral foundations and crypto duality

Markets: getting nervous

Innovation exemption? Some questions

Markets: if it moves…

Term of the day: Inflation-linked bonds

What the Bliss Trade has to do with crypto

Term of the day: Monetize the debt

Stablecoins: separating payments from credit

Markets: What are investors thinking?

Term of the day: Cantillon Effect

Stablecoins, banks and innovation

Macro: stagflationary pressure gets stronger

Term of the day: PMI

Stablecoins: separating payments from credit

The push to change the nature of US banking continues.

On Tuesday, President Trump signed a bombshell of an Executive Order that aims to remove access barriers to financial innovation. But, ultimately, it’s about much more than signalling support for the digital assets ecosystem.

The President asked the US central bank’s Board of Governors and the heads of all Federal financial regulators (there are five: CFPB, SEC, CFTC, NCUA, FDIC, OCC) to, within 90 days:

“conduct a review of existing regulations, guidance, supervisory practices, and application processes to identify those that could be updated to facilitate innovation, and competition to financial products and services for fintech firms, particularly those that are small and emerging.” (my emphasis)

Excellent, let’s bring more fintech firms into the regulatory fold, arguably a win-win for everyone except the incumbent institutions terrified of competition.

But the more transformative part of the EO was further down, in Section 4. There, Trump asked the Federal Reserve to, within 120 days:

“conduct a comprehensive evaluation of the legal, regulatory, and policy framework governing access to Reserve Bank payment accounts and payment services by uninsured depository institutions and non-bank financial companies, including those engaged in digital assets and other novel financial activities.” (my emphasis)

Trump has asked the central bank to come up with ways to allow non-banks, including stablecoin issuers, to access central bank payment systems.

This is huge, and not just because it signals full institutional acceptance that digital asset rails will form an integral part of the US (and therefore the global) financial system going forward.

It’s a big deal because of what it means for the concept of banking.

Banks and payments

You’ve probably heard the joke about the bank robber who, when asked why he robbed banks, answered: “Because that’s where the money is.”

The same can be said for why banks handle our payments. It’s where our money is usually kept, and so it makes sense that payments originate from our bank accounts.

What is less intuitive is the marriage between payments and lending. This is not just about final payment settlement between banks relying on intraday and overnight credit; it’s also the centuries-old practice of taking funds deposited for safekeeping and convenience, and lending most of them out to a range of borrowers. Put differently, the payments we route through banks rely on a web of promises.

Obviously, the payments landscape has diversified and spread over the decades, diluting direct bank participation while extending the plumbing. But virtually all electronic payments touch bank credit at some stage of their journey.

This generally works fine. But history has shown that payment networks can freeze at times of systemic stress. Even outside a widespread banking crisis, issues with any one institution can create mayhem as network participants are reluctant to enter into even short-term settlement commitments.

Stablecoins, running on a separate settlement network, remove the reliance of payments on bank networks. As we saw in March 2023, this does not mean stablecoins would be immune to any fallout from a banking crisis, but the settlement of stablecoin payments does not depend on the traditional financial system.

Only, banks have insisted that their payments settlement is “better” despite more limited operating hours and, in most cases, higher costs. And you know, they have a point. Their payment settlement is technically “better” because it counts on the ultimate liquidity backstop, the central bank. In times of stress, the central bank will step in and make sure payments settle.

(I’ve written before about how the banks’ monopoly on Fed payment rails leads to what Dan Awrey calls a Reverse Gresham’s Law, where reliance on “good money” means bad payments, and the spreading use of good payments means more reliance on “bad money”, as in money not backed by central bank access.)

Stablecoins, of course, operate outside of this protective oversight and could suffer from network glitches, bank-related redemption issues, or other problems the central bank doesn’t have to care about.

If stablecoin issuers get access to federal reserve payments services, however, then they also get access to that coveted central bank liquidity backstop. Their payment services become as reliable as those of banks, and they are likely to be cheaper and faster.

Plus, access to the federal reserve payment system would improve the operating margins of digital asset firms by reducing settlement costs – it turns out that working with the central bank is cheaper than working with commercial banks.

Perhaps more significant, it would also establish a basis for a payment network that did not rely on the solvency of bank loans. Stepping back and zooming out, this could potentially enhance the resilience of the US economy. In the event of another banking crisis, payments could continue to flow unimpeded through non-bank institutions.

Competition

It’s worth pointing out that the United States is, today, the only G7 country that limits central bank payment rails access to banks. The UK opened up access in 2017, Japan in 2022, the EU last year, Canada earlier this year. It’s also not a stretch to guess why the US is so far behind – yes, it’s the collective banking lobby and its bleats about the threat to the US economy should their monopoly be eroded.

Banks are, of course, going to fight Trump’s EO tooth and nail. They have already lost their monopoly on deposits. Now they stand to lose their monopoly on Fed-level payment rails. For the sake of innovation, I hope they lose this fight, largely because they deserve to for resisting consumer-facing improvements to their service that might erode margins, and because the lobbies have been outright lying about the risk this migration away from the centre poses to bank lending. (See also this excellent essay by Omid Malekan.)

Of course, the break will never be total – banks are convenient and familiar and will long continue to be the dominant gatekeepers to financial services. But competition is hammering at the door.

And it seems like the Administration is no longer going to be subtle about its assault on the bank chokehold. Here’s another excerpt from the EO:

“The Federal Government must update regulations to allow integration of digital assets and innovative technology into traditional financial services and payment systems. The Federal Government must also remove overly burdensome and fragmented regulations and supervisory practices that form barriers to entry and primarily benefit incumbent financial services firms.” (my emphasis)

I’ve speculated before that the SEC is using support for onchain marketplaces as a petri dish in which to re-write securities law, updating it for the modern era without a vicious fight for every amendment to wording drawn up in the era before computers.

It looks like the banking regulators will be doing the same: using digital assets as a banking regulation workaround. Let the disruptors in through the side door, and watch the market decide.

See also:

Stablecoins and the new Gresham’s Law (Feb 2026)

Stablecoin rewards and bank deceit (March 2026)

Kraken, the Fed and the new payments landscape (March 2026)

🌿 If you’re not a subscriber to the premium daily Crypto is Macro Now, I hope you’ll consider becoming one! You’ll get ~daily commentary on how crypto is impacting the macro landscape, and vice versa - plus links, charts, and some fun stuff because why not. 🌿

What the Bliss Trade has to do with crypto

I’m kicking myself for having missed this Financial Times op-ed when it first came out a couple of weeks ago, but it’s still relevant: Gita Gopinath, Harvard economics professor and former chief economist of the IMF, lays out why the US stock market continues to dance underneath storm clouds, and what this means for the global outlook.

She introduces the catchy term “Bliss trade”, which she defines as a belief in market resilience underwritten by “big lasting state support”.

The key word here is “lasting”. The TACO (Trump Always Chickens Out) trade, she points out, is certainly a factor in the market assumption that stock market trouble will soon pass.

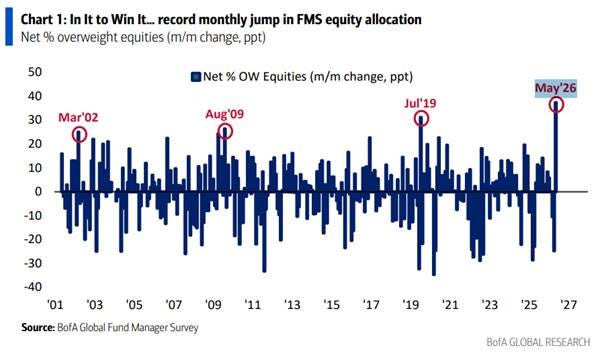

Indeed, the Bank of America Global Fund Manager Survey released this week showed a record increase in equity allocations and a big cut in cash levels, fuelled by the assumption that the Iran War is pretty much over and that looming inflation and higher yields won’t be a problem.

(chart via @MikeZaccardi)

Fine. But TACO depends on the whims of the President and can’t be extended beyond his term.

The Bliss trade can, as it transcends politics. It is now structural. Parties across the ideological spectrum now favour more spending, and any politician arguing for less knows they will either not get elected or soon find themselves out of a job.

What’s more, actions in recent years have shown that the spending, support, bailouts, whatever you want to call it, does not have to be targeted nor limited:

During the pandemic, advanced economy government support averaged 25% of GDP, and boosted consumer and business finances for several years.

When Russia invaded Ukraine in 2022 and triggered an energy price surge, European governments spent 2.5% of GDP on broad price-supressing measures, when fully compensating the bottom 40% of households for the cost increase would have cost 0.9% of GDP.

The recent climb in energy prices as a result of the Hormuz closure has reactivated subsidies and tax measures in Germany, Spain and Italy.

Gopinath recognizes that supporting citizens and businesses in a crisis is a worthy public goal – but she worries that this support has become large and lasting rather than targeted and temporary, weakening governments’ fiscal position.

And, once given, this support can’t be taken away without backlash. This, of course, creates a moral hazard and quasi-permanent risk-on behaviour – pile in while you can, lever up as much as possible, as your losses will be capped while your upside isn’t.

All that rings true. Where I differ from Gopinath’s conclusion is in the progression from here. She insists that the Bliss trade is fragile because governments are going to run into fiscal constraints. Put differently, markets may be pricing in insurance states can no longer afford to provide.

We have to remember that she is the former Deputy Managing Director and Chief Economist of the IMF, which has fiscal sustainability as one of its main goals. And, arguably, the institution has wielded considerable global influence when it comes to using development loans to incentivize certain policy changes.

This perhaps conditions the institution, and its former officials, to assume that fiscal sustainability is an option for political parties eager to hold on to power. It’s not. Put differently, officials have seen that stimulus works, and the consequences – inflation, stressed bond markets and increasingly entrenched expectations of a backstop – are more palatable than an economic collapse or, just as bad for some leaders, an election defeat.

Sure, eventually investors will start to worry about debt sustainability, pushing global yields up – but that can largely be absorbed by the vast pools of capital that need to park somewhere. Government debt may be getting riskier, but that doesn’t mean it won’t find investors.

We’ve seen in the past how episodes of stimulus can send crypto prices soaring. The pandemic-triggered flood of money into markets pushed BTC up almost 20x between March 2020 and April 2021. We’ve also seen how most traders steer using the rear-view mirror – over the past few years I’ve had so many debates with those convinced the “bazooka” would spring into action again should the economy show signs of slowing. I argued and still believe that future support will take other forms, but the debate itself highlights the assumption, correct I think, that governments can never go back to letting markets crash and citizens hit real poverty.

And no matter the form of the official support, the result is higher government debt, which will require more money printing. By extension, this means more currency debasement, and therefore also more interest in hard assets such as Bitcoin.

This may not manifest as a surge in the BTC price – much depends on the swings of sentiment and the nature of the stimulus signals. Plus, investors these days have so many speculative assets to choose from should they want to lever up a risk-on trade.

Rather, it’s more likely that the debasement effect will predominate over time, supporting periods of momentum swings. Put differently, going forward Bitcoin offers something for long-term investors looking for a debasement hedge, as well as something for short-term traders betting on demand acceleration.

✨ If you find this newsletter interesting, or even if you just like my excellent taste in music and gifs, would you mind sharing it with friends and colleagues, and nudging them to subscribe? I’d appreciate it! ✨

ASSORTED LINKS

(A selection of reads I came across this week that I think are worth sharing, not about crypto nor macro. I try to choose links without a paywall, but when I feel it’s worth making an exception, I specify.)

Below, I write more on the Croatian entry to last weekend’s Eurovision Song Contest – here I share a powerful essay by Delphine Chui in Restoring the West that highlights the value in cultural remembrance, however uncomfortable it may make some people. (Croatia’s Eurovision Entry Broke Through Europe’s Cultural Amnesia, Restoring the West)

“Healthy societies should preserve memory honestly, without collapsing into either self-hatred or tribal grievance. Europe does not need historical amnesia disguised as tolerance, nor does it need endless civilizational resentment masquerading as pride. It needs cultural confidence grounded in truth and continuity, which means acknowledging the complexities of European history while still allowing Europeans to honor their ancestors, traditions, symbols, and faith without apology. There is also something profoundly important about younger Europeans rediscovering their own cultural inheritance without immediately filtering it through either nationalist resentment or progressive shame.”

Abigail Monti opens our eyes to the signalling of books, both to us and from us. What makes you choose one book over another? What do you want the world to know about your choices, and why? For the uninitiated like me, TBR means “to be read”. (The Longer I Work in Publishing, the More I’m Convinced It’s Sorcery, Psychology, and Guesswork, Unsolicited Manuscript)

Tyler Cowen presents evidence that wokeism was just a passing phase – but asks, what did that phase really represent? And what does its passing mean for the underlying drivers? (Wokeness Has Peaked. What Followed Is Worse, The Free Press)

Laura Kennedy rips apart the expectation of “niceness” which particularly affects women who don’t want to disappoint. (The Nicest Woman You Know Probably Resents You, Peak Notions)

A riveting story – an excerpt from a new book – about legacy and art and theft and provenance, ranging from the Cambodia jungle to Manhattan via Mayfair. (Chasing the Man Who Stole the Godsv, Bloomberg – paywall)

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

Last week, I mentioned the Eurovision Song Contest and that I was rooting for Croatia. Predictably, its entry did not do well – I assumed it was because it was too stylish, too harmonious, too original, too Croatian. I confess I was unaware of the cultural criticism, that the reminder of abuses during Ottoman rule was Islamophobic. That makes me even more frustrated that the group LELEK didn’t do better as it’s high time we stop pretending history was not forged through courage and fear, subjugation and victory, atrocities and heroism, identity and bonding. And survival.

Above, I shared a link to a powerful piece in Restoring the West that highlights the importance of remembering our cultural history.

Below, I share the original video of the Croatian entry: Andromeda, by LELEK.

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.