WEEKLY - securities vs money, TradFi vs DeFi

plus: assorted links, February blues and more

Hi everyone! I hope you’ve all been taking care of yourselves. Uncertainty shot up to a whole new level this morning with the attack on Iran. This does not exactly come as a surprise, and yet we all know that the unpredictable happens in war.

It’s notable that BTC is reflecting risk-off behaviour so far – how long this continues depends on what happens over the next few hours and days. Meanwhile, we have to hold onto the hope that the casualties are minimal, that peace in the Middle East is restored fast, and that the Iranian people can enter a new phase of opportunity.

I’ll write more about the geopolitical implications and what this could mean for markets and crypto on Monday.

👁

Sorry I had to miss last Saturday’s publication – eye surgery Thursday last week and again this past Thursday. Both went well but ouch. Still can’t see straight (so many opportunities for puns here), but I know time will take care of that.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

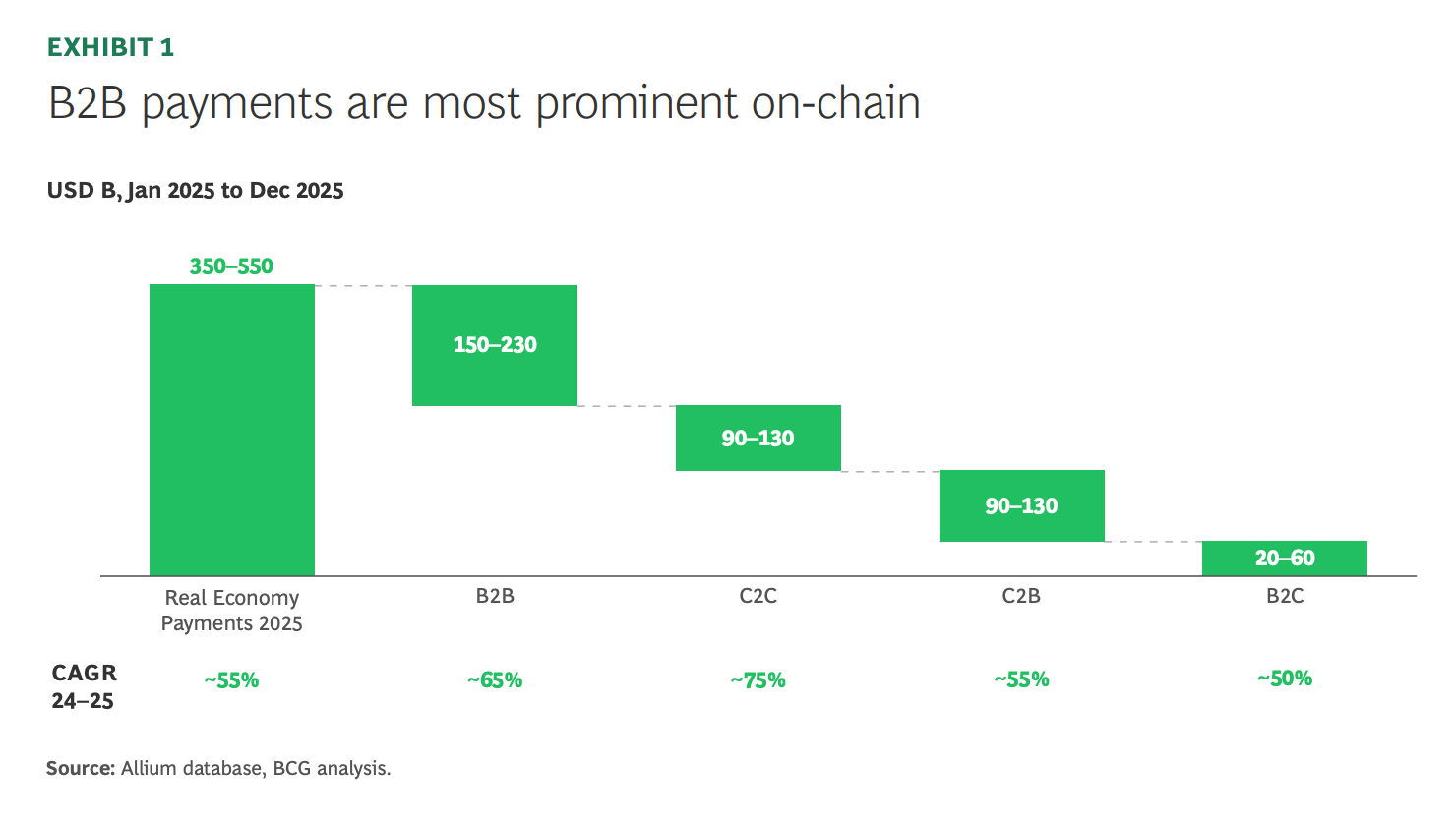

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

My op-ed in American Banker this week (paywall!) looks at how community banks can harness stablecoins to develop new business lines that deepen engagement with their communities, boost economic activity and strengthen bank resilience. “Community banks should grab the opportunities created by stablecoins”

👁

If you’re not a subscriber to the premium dailies, I hope you’ll consider becoming one! You’ll get access to market commentary as well as adoption insight and industry trends. Plus, assorted links and music recommendations ‘cos why not…

In this newsletter:

Tokenized money market funds get more money-like

TradFi embraces DeFi? Not quite.

Assorted links: Optimization vs mattering, the run-up to the Ukraine invasion, portraits, deep reading, making a hit movie, UFOs

Weekend: Goodbye February

✨

If you speak Spanish and are interested in a less frequent, shorter update on developments in the crypto-macro intersection, you can subscribe to Cripto es Macro here.

Some of the topics discussed in this week’s premium dailies:

Coming up this week: US GDP & PCE, Fed minutes, maybe Supreme Court

Digital euro politics

US CPI: too soon to celebrate

Chinese New Year: risk and opportunity

Markets: still risk-off

TradFi embraces DeFi? Not quite.

Markets: tension builds

Coming up this week: politics, Nvidia, wholesale inflation

Monday mood: the CLARITY crunch

The tariff shift: what, why and how

Markets: the reaction

Macro: US economic data

The window of pre-mortem thinking

Macro: a crowdsourced outlook

Markets: simmering rotation

Crypto: a win for liquidity

Tokenized money market funds get more money-like

Meta and stablecoins

Markets: patience and the disconnect

Tokenized money market funds get more money-like

I wrote this week about the SEC guidance on broker-dealer capital requirements for stablecoins – here’s another seemingly small technical regulatory tweak with a potentially huge impact.

The SEC has granted an exemption for WisdomTree’s tokenized money market fund WTGXX that allows it to be traded by an authorized broker-dealer at $1.

This may at first seem like a distinction without a difference since that’s the NAV money market funds (MMFs) aim for anyway.

The big deal is that MMFs usually settle in a primary market transaction – directly with issuers – once a day, with the issuers executing the corresponding adjustment in the portfolio of backing assets, and bearing responsibility for the fund’s liquidity.

Under the exemption, the fund can trade on a secondary platform at a fixed price of $1, with the broker-dealer providing the liquidity. In this case, the broker-dealer will be WisdomTree Securities (with settlement in USDC) so the activity is not leaving the firm’s ecosystem, but this is a step towards externalizing liquidity for MMF issuers.

Why is this a big deal? Because it means the fund can change hands without requiring an underlying the portfolio adjustment, removing an arguably unnecessary point of market friction. And since any sale or purchase of WTGXX does not need to wait for end-of-day pricing, it can trade at any time.

What’s more, since WTGXX accrues yield continually throughout the day – unlike typical MMFs that get returns calculated once a day – investors can use the token for intraday yield.

For now, this is only available to institutional investors, but the firm has plans to roll it out for retail participants later this year.

Here’s why this seemingly small exemption is potentially more meaningful for the stablecoin outlook than any number of adoption or new token launch announcements:

1 – Broader trading hours enables WTGXX to act as a more flexible reserve asset for stablecoins under the GENIUS Act. More flexible reserve assets that can satisfy stablecoin redemptions at any time should reassure regulators concerned about any liquidity impact to the treasury market, with a broker-dealer shouldering some of the timing risk.

2 – WTGXX can provide yield for stablecoins. Idle balances can be swept into a tokenized MMF, and out again when they need to move – a simple, clean way to make the bank lobby objections irrelevant. True, for this to be useful for all stablecoin market participants, more tokenized MMFs will need similar exemptions, and will need to be available to a wider range of holders (not just accredited investors), but that seems to be on the horizon. WisdomTree has shown it can be done.

3 – This move is a step towards money market funds themselves being considered a settlement asset. After all, they are backed by the same reserves as stablecoins – the main differences are their classification as a security, and their restricted trading flexibility. This move from the SEC goes some way towards solving for the latter. And it’s probable that restrictions on access to and transferability of tokenized money market funds will be further relaxed as part of the agency’s preparation for tokenized markets. If the tokens have an assured value of $1, the only reason they can’t be used as “money” is their security classification and the resulting trading restrictions.

This is one of the more meaningful steps I’ve seen in a while. On its own, it won’t be transformative – WTGXX distribution is still heavily concentrated (over 95% of circulating supply is held by five addresses) – but it’s a step towards broader distribution and utility for the fund, and a welcome signpost on the path toward blurring the boundaries between money and securities.

Big reforms are welcome, but it’s the little tweaks that end up having the biggest real impact.

🏵 If you find these newsletters useful, would you mind sharing with friends and colleagues, and nudging them to subscribe? I’d appreciate it! 🏵

TradFi embraces DeFi? Not quite.

I’m starting to feel like my role here is to weekly publish something along the lines of “no, it’s not quite like that”, as pushback against the inevitable breathless hype when a large institution does anything in the crypto arena. I’m also well aware that this makes me not much fun at parties, and it’s a good thing I don’t go to crypto events anymore – but someone has to put things in context, right? For now, it seems that’s me.

You might have noticed that last week, BlackRock’s BUIDL token got listed on decentralized exchange Uniswap. Headlines and posts proclaim this as “It’s happening!!! TradFi embraces DeFi!!!!” and, well, no, that’s not what’s happening at all.

To be fair, “TradFi tentatively embraces a gated and centralized version of DeFi” just doesn’t have the same ring to it – but the nuance matters a ton.

Some detail: last week, Uniswap announced that BUIDL – a tokenized money market fun managed by BlackRock with Securitize running the back-end – could now be traded on an adaptation of UniswapX, a decentralized aggregator that scours all platforms (including Uniswap) to fill swap requests. Basically, a holder can indicate what tokens she wishes to swap her BUIDL for, “fillers” scour the ecosystem to find the best exchange rate, and a smart contract executes the swap.

This is an intriguing development that could bring further liquidity and utility to BUIDL. But it’s not full DeFi, as only whitelisted investors and whitelisted sources can participate.

It’s a start, though. We won’t see institutions embrace full decentralization – they have to comply with KYC, AML and a host of other rules, they have to identify all users of facilitated products, and they have to deny access to those that don’t fulfil the relevant criteria. True DeFi applications, on the other hand, are meant to be “permissionless”, with anyone able to onboard. TradFi is about access; DeFi is about execution.

What’s more, few yield-bearing tokenized securities are available to retail investors, given insane securities laws that requires publicly listed money market funds to jump through pretty much the same hoops as risky securities that actually warrant in-depth disclosures. So, to avoid the costly and time-consuming process, most tokenized versions rely on exemptions that limit their scope to accredited institutional investors. This is not about protecting retail investors, as money market funds are not exactly risky; it’s about minimizing bureaucratic burden.

So, here we have a gated asset passing through a gated adaptation of decentralized technology. It’s an encouraging step forward, and a sign of what the TradFi-DeFi intersection will look like: limited use, but nevertheless testing new types of disintermediated efficiency. From asset managers enabling swaps to banks supporting semi-decentralized lending, the potential to make finance more efficient is enormous.

What’s more, signs have been trickling in for a couple of years now that institutional demand is building. Last year, Anchorage Digital integrated a Uniswap trading API into its institutional wallet. Aave’s Horizon permissioned decentralized lending protocol accepts as collateral institutional tokenized funds from WisdomTree, VanEck, Hamilton Lane, Superstate, Circle and others. As of last April, Apollo’s ACRED tokenized credit fund can be deposited as collateral into a levered lending strategy powered by Morpho smart contracts and curated by Gauntlet. And earlier this week, Apollo and Morpho announced a deeper collaboration to develop institutional applications of decentralized lending markets. I could go on.

But is this what we’re going to get excited about? Traditional finance yet again restricting interesting opportunities for capital formation to those who are already wealthy?

BlackRock, Securitize and Uniswap deserve praise here for pushing the envelope where they can. And BlackRock’s purchase of UNI tokens is a supportive statement.

In other words, several large institutions clearly have the vision and the will to explore DeFi efficiencies; this is exciting. The issue is outdated securities laws. Reforming disclosure rules is one of Chair Atkins’ priorities for his tenure at the SEC – let’s wish him luck on this, it’s important.

Meanwhile, I’m going to continue pushing back on overinflated claims that mask the colossal task ahead and that convey a complacent sense of success when we’ve only just started.

ASSORTED LINKS

(A selection of reads I came across this week that I think are worth sharing, not always about crypto or macro. I try to choose links without a paywall, but when I feel it’s worth making an exception, I specify.)

A thoughtful and moving piece about a world in which optimization is cheap but mattering get expensive, unless we change the questions we ask ourselves and learn to identify “ghost achievement”. (Ghost Achievement, The Curious Mind)

A soberingly detailed account of the runup to the Russian invasion of Ukraine, and of how the CIA and MI6 knew about it but couldn’t get Ukrainian and other European officials to believe them. (A war foretold, The Guardian)

We don’t think much about what goes into a photo portrait, but after reading this, we’ll probably question them differently: Why did the photographer choose this one? Did the subject like it? What image did each wish to portray? Why? (What Does a Photographer Owe the Portrait Subject?, In the Flash)

A podcast link for a change, to an enchanting interview by Mishal Husain (one of the best interviewers out there) with Maggie Kang, creator of K-Pop Demon Hunters, about the motivation, the creative process and the unexpected yet deserved global success of a gorgeous movie. (She Bet on K-Pop. Netflix Got Its Biggest Movie Ever, Bloomberg)

It looks like deep reading is fashionable again, which should be enough to debunk the “we’re all becoming robots” narrative of AI optimization. (The Difficult Novel Is Making Its Comeback, Bloomberg – paywall)

Tyler Cowen reserves judgement on whether UFO sightings are from aliens, but he reasonably urges us to keep an open mind. (The Truth About Aliens Is Hiding in Plain Sight, The Free Press – paywall)

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

Here in Madrid we are finally being blessed with blue skies and gentle temperatures, but I gather from friends in the US that we are among the lucky few. We’ve had soggy weeks, though, in part alleviated by the cathartic and companionable misery of the below video – I share it with you today to celebrate the closure of one of the gloomiest months of the year.

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.