WEEKLY – shifting reserves, stablecoins’ impact on Treasuries

Plus: assorted links, gorgeous images and more

Hello everyone! I hope June is treating you gently so far and that the market drop isn’t too painful for you…

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

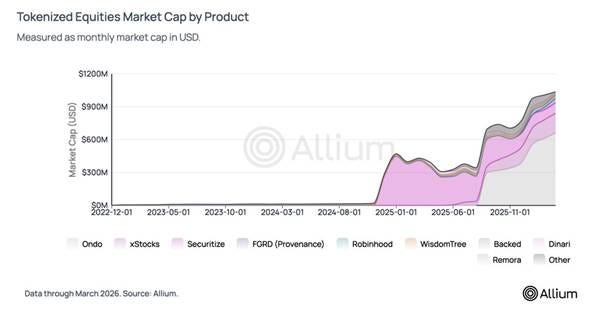

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

In this newsletter:

The changing shape of reserves

Stablecoins and Treasuries: which affects which?

Assorted links: AI and writing, AI and humanity, dysfunctional politics, books and movies, corporate kitchen gossip

Weekend: stunning nature photography

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

Some of the topics discussed in this week’s premium dailies:

Coming up this week

Monday mood: The hijacking of the sovereign

Term of the day: OECD

The CFTC and perpetual motion

Term of the day: perpetual futures

Markets: structural weakness

Stablecoins and Treasuries: which affects which?

Term of the day: endogeneity

Markets: it’s all relative

Macro: US jobs are doing OK

The changing shape of reserves

Markets: mining the data

Term of the day: realized profit/loss

How tokenized deposits could compete with stablecoins

Term of the day: Balkanized

Recommended podcast episodes

The changing shape of reserves

One of the recurring themes I write about in this newsletter is the changing monetary structure of global finance. This compelling topic draws on the politics of stablecoins, deposit tokens and other onchain representations of money-like assets. It also covers the geopolitical use of CBDCs, the looming threat of capital controls and other methods to more directly influence how money is used. And it touches on the changing role of the US dollar in global finance: the weaponization of access, the emergence of alternatives and what that suggests for reserve balances going forward. Ultimately, all this is changing our understanding of what money is.

I could write volumes on this (and probably will, so stay tuned), but given today’s limitations of time and space, I want to focus on two pieces of news I’ve seen this week that are ringing a shiny bell.

The weight of gold

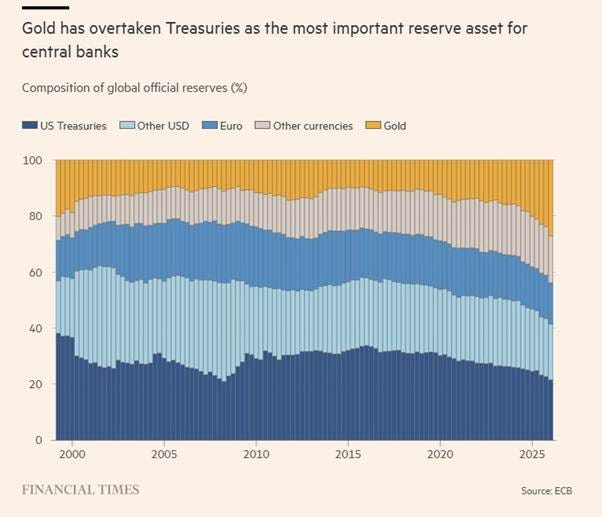

One is an article in the Financial Times that highlights data from a European Central Bank report showing that the weight of gold in global central bank reserves (27%) has overtaken that of US treasuries (22%) – the implicit suggestion is that US government debt is no longer seen as the world’s “safest asset”.

(chart via the Financial Times)

I’ll get to the implications, but first some caveats to the FT chart.

First, the total weight of dollar assets still surpasses that of gold – add in the “other USD” category and you’re up to 42%. So, faith in the dollar is still strong.

Also, the increase in the weight of gold in reserves is largely influenced by the surge in the metal’s price in 2025. The ECB did the math: revaluing gold reserves at the end-2024 gold price brings the weight down to 20%, below that of the more stable US Treasuries (see chart further down).

But still, whatever the reason, the weight of gold in central bank reserves is going up, and that of the US dollar is coming down.

My interest was piqued here because of what this says about reserve currencies. The dollar settles the bulk of global trade. But its weight as a reserve asset is declining, while that of gold is increasing. We’re so used to conflating reserve currencies with reserve assets that it will take a while for the idea that they can be separate to sink in. Gold could become the world’s reserve asset without being its reserve currency.

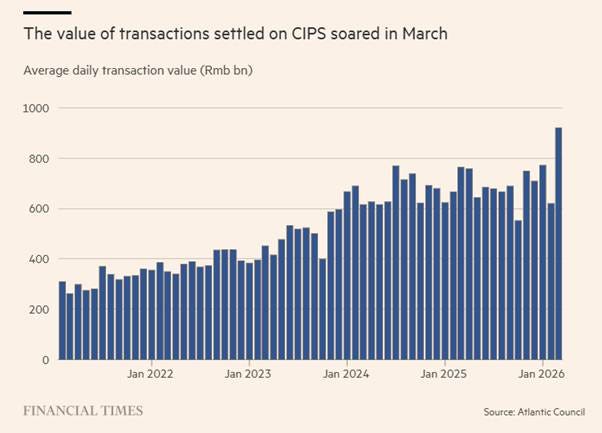

This is especially relevant given the fragmentation in not just global trade but also payment systems. SWIFT still dominates the coordination of cross-border bank transfers, but use of China’s alternative CIPS system is growing.

(chart via the Financial Times)

Earlier this year, India said it would use the upcoming BRICS summit in New Delhi to propose a platform linking the group members’ digital currencies. Russia is expected to launch its CBDC in September.

This week, Macau’s monetary authority announced that 11 of its banks have joined CBDC connector mBridge, built by the central banks of China, Hong Kong, Thailand and the UAE, with Saudi Arabia joining the club in 2024.

And while a February report from Allium showed that cross-border stablecoin flows were still modest, use of onchain tokens instead of the traditional system is likely to grow as the onramps and rails expand and as sanctions and other forms of weaponizing dollar access become a more frequent feature of global trade.

(chart via Allium, sponsors of this newsletter but that’s not why I’m sharing this)

In sum, the shifting balance of assets in central bank reserves suggests an evolving view of diversification.

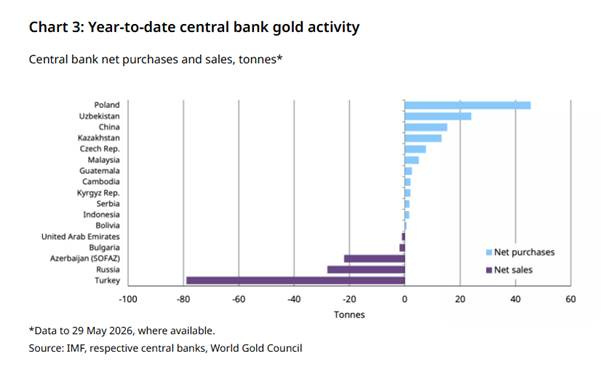

It’s not just about holding value, it’s also about utility. For many countries, especially those fearing sanctions or asset seizures, gold has a more resilient reserve utility than the dollar. The ECB report points out that the central banks most active in gold purchases tend to be in or near conflict regions. Indeed, a report out earlier this week from the World Gold Council shows that the top central bank buyers so far this year have been Poland, Uzbekistan, China and Kazakhstan.

(chart via the World Gold Organization)

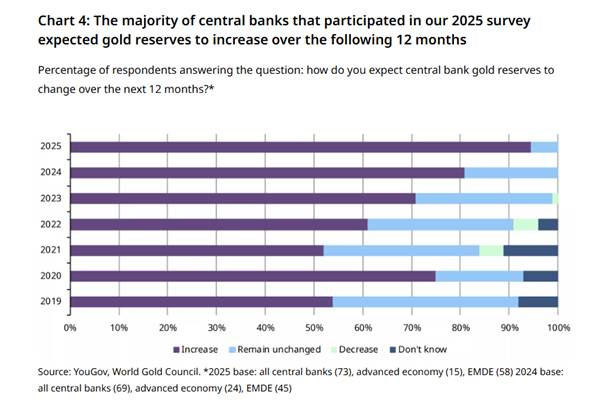

And in a 2025 survey, almost 95% of central banks surveyed for the report say they expect their gold reserves to increase over the next 12 months, up from just over 80% in 2024.

(chart via the World Gold Organization)

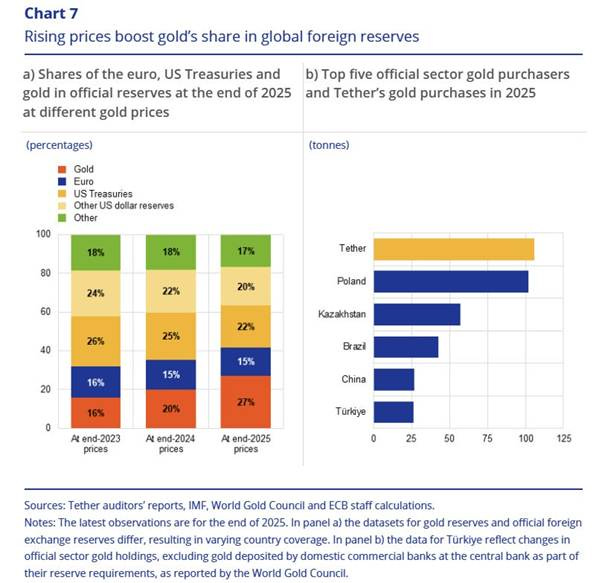

But the ECB does not approve. It argues that gold makes a terrible central bank reserve asset, given its volatility, its lack of remuneration, and the cost of its storage. Also:

“More importantly, the supply of gold is not fully elastic and does not adjust seamlessly to shifts in international demand for liquidity.”

A very central banker thing to say.

And here’s an interesting detail: the report singles out Tether as an even larger buyer of gold in 2025 than Poland, the top hoarder among central banks.

(chart via the ECB)

Tether’s CEO Paolo Ardoino did say earlier this year in an interview for Bloomberg that his firm was becoming a “gold central bank”. Given that it is the world’s largest stablecoin issuer, that stablecoins are muscling in on fiat money rails, and that ECB Chief Christine Lagarde often highlights dollar stablecoins as a threat to the euro and to her institution’s monetary sovereignty, you can imagine how much this must have ruffled feathers.

At least threatened central bankers can take comfort from the fact that you can spend fiat currency but you can’t spend gold.

This segues nicely into the next item from this week that caught my attention.

Tether and gold

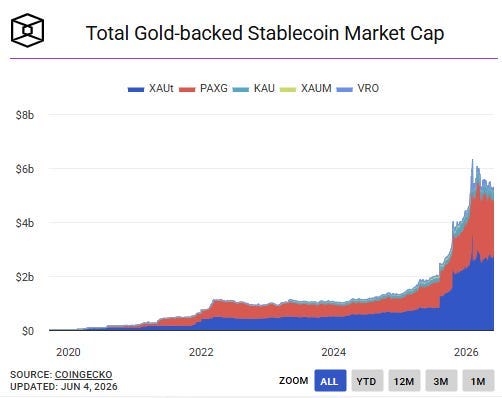

On Wednesday, Tether announced the launch of a card that would allow holders to spend their tokenized gold.

Let’s back up a bit. Tether launched XAUt back in 2020. It was not the ecosystem’s first gold token, but it quickly became the leader in terms of market share and trading volumes, and you can see from the below chart just how much these have grown.

(chart via The Block)

Demand has been helped over the years by steady improvements in wallets, custody and market making services, which together streamline onboarding, improve utility and deepen liquidity of gold-backed tokens. The concept gets especially interesting when you picture tokenized gold nestled next to tokenized dollars – in April, Tether launched a self-custodial wallet that enables anyone to hold XAUt, USDT, USAT (its GENIUS-compliant dollar stablecoin) and BTC, using the same interface.

Now, per this week’s announcement, users will be able to get a Visa card that links to their XAUt wallet, enabling holders to “spend” gold.

Ok, technically the XAUt token is converted into USDT which is then converted into USD for distribution to the merchant. But in the minds of users, they’re spending gold.

You can see how this could further blur definitional boundaries. Gold, as we saw above, is increasingly becoming a reserve asset, but it’s not a currency.

Only, if you can spend a gold-backed token, does the distinction matter that much?

Of course, peel back the layers and users are actually spending USD – merchants don’t want to accept gold. But the reason for holding gold is changing.

To circle this back around to the question of reserves, above I shared a chart from an FT article published a couple of weeks ago that shows the surge in payment volumes on China’s CIPS system. The article was discussing the internationalization of the yuan, a key goal of the current Five Year Plan. It mentions the recent expansion of the Shanghai Gold Exchange, and suggests that this could pave the way for greater acceptance of the renminbi in trade settlement – receivers of the Chinese currency can convert into gold until conversion back into renminbi is needed, without touching dollars. Gold as a “safe” reserve asset, and as a currency placeholder?

So, combine shifting reserve balances with the evolving utility of new technologies, and you can start to glimpse a new landscape that blurs definitions while reshaping power structures. Interesting times.

See also:

A CBDC alternative to SWIFT? (Nov 2023)

China’s digital yuan changes shape (Jan 2026)

🌿 If you’re not a subscriber to the premium daily Crypto is Macro Now, I hope you’ll consider becoming one! You’ll get ~daily commentary on how crypto is impacting the macro landscape, and vice versa - plus links, charts, and some fun stuff because why not. 🌿

Stablecoins and Treasuries: which affects which?

This week I started skimming an updated BIS paper by Rashad Ahmed and Iñaki Aldasoro that looks at the relationship between stablecoin demand and Treasury yields. I’m not sure why I did this, as I’ve seen so many of these papers before. Yes, we know they’re related, and yes, we know that’s why the US Treasury Secretary is so excited about the potential demand.

I’m glad I did, though, as it turned out to be a lot more interesting than I expected, especially because of the discussion of endogeneity (when factors and variables in an equation affect each other), which has been largely absent from most other papers I’ve skimmed.

(A confession that may sound like a humblebrag but really isn’t: I have a degree from Brown University in Applied Mathematics and Economics, which perhaps goes some way towards explaining why I can be such a pedant at times. Anyway, despite that, I understood very little of the technical side of the paper, which is no doubt more down to my terrible memory and rapidly advancing age than to the education received. I bring this up because I had to look up “endogeneity” and am now fascinated with it – I gave a more detailed explanation earlier this week.)

The BIS paper finds that stablecoin demand influences short-term Treasury yields.

No surprise there, but the authors provide numbers:

A $3.5 billion 5-day inflow into stablecoins lowers 3-month T-bill yields by 0.7 basis points on impact, and up to four basis points within 10 days (deployment lag, some tokens distributed from pre-issued stock).

The effects can be roughly double at times of market stress.

Lifting the lid, the conclusions get more interesting when we compare the updated paper with the initial version, published just over a year ago. I asked Grok to pull the differences for me:

The methodology has been changed to get a more refined flow-through estimate, but I won’t go into more detail here because there’s not much hope of my understanding it in the time I have to write this. It has to do with a more granular exploration of endogeneity.

This has led the authors to almost double the estimated impact.

Also, the original paper highlighted the asymmetry of the stablecoin impact – a jump in demand had a more pronounced impact than a drop in demand (more upside than downside). The new paper downplays this, focusing more on the state of the market – the impact of stablecoin demand is greater when markets are stressed.

So, extrapolating, if the total current market capitalization of fiat-backed stablecoins of around $270 billion goes up by 10% from here, we’re looking at a roughly 30 basis point drop in the 3-month T-bill yield. That… doesn’t feel particularly significant.

And it’s much, much less than other studies I’ve seen.

Here’s where the endogeneity (this can also be understood as formula reflexivity, the formula influences itself) comes in. The authors recognize that:

1) There are factors that affect demand for both stablecoins and Treasury bills that are not directly related to either. For instance, imagine that Fed Chair Kevin Warsh manages to do what President Trump wants and convinces the FOMC committee to lower rates by a full percentage point (I know, a stretch but work with me here). In theory, this would lower short-term Treasury yields. It would also boost demand for stablecoins by ushering in a “risk-on” trading environment (for now the main use case for stablecoins is in crypto trading). In this case, we couldn’t say that the yields were coming down because of a jump in stablecoin demand. I mean, partially, but not really.

2) The influence channel works in both directions. Stablecoin demand influences T-bill demand, but T-bill demand also influences stablecoin demand. Lower yields would normally encourage more demand for stablecoins by stimulating crypto trading (a more “risk on” environment) and by making DeFi yields more attractive in risk-adjusted terms.

So, the conclusions of the paper itself are interesting in that the suggested impact is not as great as other sources have claimed.

But more importantly, the authors give us tools with which to question impact claims that just feel too optimistic.

See also:

Term of the day: endogeneity (June 2026)

The overlooked stablecoin pushback (May 2026)

Overlooked stablecoin risks (March 2026)

✨ If you find this newsletter interesting, or even if you just like my excellent taste in music and gifs, would you mind sharing it with friends and colleagues, and nudging them to subscribe? I’d appreciate it! ✨

ASSORTED LINKS

(A selection of reads I came across this week that I think are worth sharing, not about crypto nor macro. I try to choose links without a paywall, but when I feel it’s worth making an exception, I specify.)

An encouraging piece by Jasmine Sun on how to get by as a writer in the age of AI. It’s about telling secrets, delegating where possible, meeting people and enjoying the glorious freedom of independence. (The independent writer’s advantage in the age of AI, On Substack)

Whether you’re Catholic or not, Pope Leo XIV’s encyclical on the new technological age is a meaningful document for millions around the world who fear humanity’s essential spirit is hanging by a thread. I confess I haven’t read it, but even though I’m not Catholic, I plan to, as perspective is often elusive in the fire-hose of snippets and narrow views. This review by Bloomberg’s Flavia Krause-Jackson was both thoughtful and moving. (The Pope’s AI Encyclical Made Me Feel Like a Catholic Again, Bloomberg – paywall)

Sinéad O’Sullivan deftly diagnoses the stagnation of politics and economies using Ireland as an example. (Kaleidoscopes, But This Time It’s Different)

How’s this for a job? Reading books and then recommending whether they should be made into a movie or series. Many of us would happily do this for free, but it turns out it requires special skills. Julien Levy profiles one of the best in the industry at this particular task, and gives us a glimpse of where what we watch on the screen is born. (The Man Who Reads Books For a Living (One Every Two Days), Literary Hub)

Not kidding, I’ve often wondered how corporate kitchens are run. Do people working there enjoy it? Do they feel company loyalty? Do they hear inside scoops while restocking the salad bar or ladling out soup? What do they think of the people they are feeding? This is a fun, deep and yet also sobering post by a former pastry chef for Meta that sheds light on some of the above questions. (I Fed the People Building the Metaverse, Titty Boobowitz)

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

It feels like it’s been ages since I shared some stunning images from a photography competition, so I’m going to make up for that today with my favourites from this year’s GDT Nature Photographer of the Year 2026 – too many breathtaking photos to choose from, so do check them all out for a welcome reminder that this planet and its wildlife are endlessly fascinating.

photo by Christian Kosanetzky

photo by Marte Engelbrecht

photo by Preeti John

photo by Christoph Kaula

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.