WEEKLY – stablecoins, central banks, prediction markets

plus, assorted links, a music video and more

Hello everyone, I hope you’re all doing well! Where did May go, seriously…

You’re reading the free weekly send of the premium daily Crypto is Macro Now, where I re-share a couple of the week’s posts and add some non-crypto and non-macro links since it’s the weekend. 🌼

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

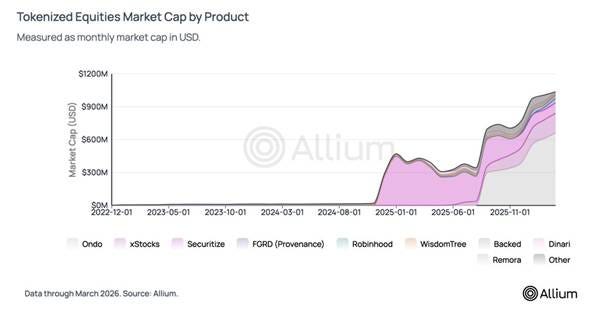

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

In this newsletter:

Stablecoins and mission creep

What prediction markets and crypto have in common

Assorted links: AI on jobs, the theatre of money laundering, attention sovereignty, maritime chokepoints, heavy metal

Weekend: the last hope

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

Some of the topics discussed in this week’s premium dailies:

Coming up this week: PCE, defence

Stablecoins and mission creep

Macro: US consumer sentiment

Term of the day: Shangri-La Dialogue

Big moves in tokenized MMFs

Markets: BTC blues

Term of the day: enrichment

The race for tokenized money utility

Markets: chips ahoy

Term of the day: BIS

What prediction markets and crypto have in common

Macro: US inflation and GDP

Term of the day: Hobson’s Choice

Stablecoins and mission creep

They’re not even pretending anymore: the European Central Bank (ECB) doesn’t like the idea of stablecoins.

There has been some lip service to the concept over the years, some mumbling about supporting commercial bank initiatives to modernize payment rails. Even the central bank’s digital euro project was initially presented as a reluctant alternative to ineffective private solutions – the implication is that a euro stablecoin would be great if only it were possible, but since it looks like it isn’t (so we’re told), here is the helpful central bank with a beautifully centralized alternative.

But innovation is a natural force (yes, even sometimes in Europe), and last week produced a handful of headlines that must have ruffled many ECB feathers.

First, there’s the surge in the number of commercial banks joining the Amsterdam-based Qivalis stablecoin consortium, with 25 new entrants pushing the total up to 37. I’ve never seen a consortium in any industry, but especially not in finance, grow so fast.

Also, last week the European Commission (EC) published two public comment consultations on the MiCA crypto framework, including questions such as whether users should be able to earn interest on stablecoin balances, whether redemptions should be charged fees, whether tokenized securities should be brought into the framework, and so on. The vibe is one of wanting to adapt to the US GENIUS Act by giving private euro stablecoins some breathing room in order to lift their volumes from insignificant levels in the face of continued global growth of stablecoin adoption.

And on Tuesday, President Trump signed an Executive Order requesting that US financial regulators look into how to give stablecoin issuers (and other fintechs) access to central bank liquidity.

That idea is rearing its head in Europe, too. Last week, Brussels-based think tank Bruegel put out a policy brief advocating for stronger euro stablecoin support as, rather than protect the euro-area financial system from digital asset risks, the EU’s restrictive approach is likely to do the opposite. Tokenization is picking up in global markets, the authors argue, and the absence of a liquid euro stablecoin ecosystem means more users will choose dollar-based alternatives.

One of the brief’s proposals is that policy makers allow regulated issuers access to central bank reserves, effectively making euro stablecoins fully-backed programmable central bank money – this would remove the risk of banking sector stress spilling over into stablecoins.

The ECB immediately pushed back with the usual nonsensical rhetoric about stablecoins weakening bank lending and introducing structural risk. That the US is heading in that direction won’t be enough to sway ECB chief Christine Lagarde, who earlier this month said:

“Our task is not to replicate instruments developed elsewhere, but to build the foundations and the infrastructure that serve our own objectives.”

In that same speech, she also said:

“…the case for promoting euro-denominated stablecoins is far weaker than it appears”.

What no one is asking is why she is giving speeches on new technology applications in the first place? Sure, the way value moves around an economy can have an impact on the smooth functioning of payment systems – but it’s not clear that would matter much for price stability, the ECB’s main mandate.

It’s also not clear how introducing a digital euro to compete with the digital appeal of stablecoins has anything to do with price stability. The stated aim is to prevent mass adoption of dollar stablecoins – but it’s not clear why a central bank solution is essential, nor why the central bank itself should be trusted to make that call.

Come to think of it, a lot of what Lagarde herself has been promoting over the past few years does not have much to do with her institution’s mandate. From belittling some new technologies while promoting others, to pushing a certain climate agenda and meddling in fiscal matters, we are looking at a clear example of mission creep, and no influential European leader is daring to question her power grab.

The blatant mission creep started almost immediately after Lagarde took office in 2019.

In May 2020, the ECB published a guide on environmental risks – why?

Oh, right:

“The ECB is of the view that institutions should take a strategic, forward-looking and comprehensive approach to considering climate-related and environmental risks.”

In 2021, the ECB announced that it would take a corporation’s ESG footprint into consideration when deciding which bonds to buy (this was at a time when the central bank was resorting to corporate bond purchases in an attempt to stimulate economic activity as its government bond purchase capacity had reached its practical limit). Essentially, the central bank was choosing to favour some companies over others within the same credit quality for ideological reasons.

In 2022, the ECB started requiring banks to assess and disclose climate-related risks in their lending portfolios, a direct attempt to influence private company decisions by linking capital requirements to environmental considerations – for instance, banks with a high exposure to the oil and gas industry would face a higher capital requirement than banks with a similar exposure to risky startups or private equity funds.

And despite supposed central bank independence, Lagarde has frequently meddled in fiscal policy, giving several speeches over the past few years advocating for certain government spending strategies.

Now, the ECB wants a direct line into consumer activity by managing digital wallets. If the “activist” mentality continues even after Lagarde steps down next year, it’s not a stretch to imagine the digital euro wallet disincentivizing certain types of purchases for being not environmentally friendly enough, or for weakening certain policy objectives.

All of the above seems to forget that the ECB’s principal mandate is price stability. Supporting the economy is relevant but secondary. It is arguably not the ECB’s job to recommend certain non-monetary policies, nor is it the ECB’s job to favour one type of technology application over another based on risk assumptions that reveal a limited understanding of what the technology does.

The digital euro project has been painted by many (myself included) as an inappropriate power grab from an institution that wants to expand its relevance at the expense of greater opportunity for financial institutions and greater convenience for consumers.

What many of us are missing is that it is just one symptom of the mission creep that seems to have accelerated under Lagarde’s leadership. That makes it harder to push back on, as even if the current plan does not go through in the form she wants, we can expect other similar initiatives.

Or, perhaps the overreach of the digital euro could, finally, trigger stronger questions about the ECB’s role in the European economy.

Then again, if there is only muted pushback and the European Parliament passes the draft law at the hearing tentatively scheduled for next month, we could see an emboldened ECB continue to march into new policy areas, further enhancing the economic and social power of an unelected institution.

Put differently, the digital euro fight is not just about CBDCs or stablecoins. No, it’s really about checks and balances on centralized power that always, instinctively, reaches for more.

See also:

ECB: stablecoins bad, CBDCs good (May 2026)

EU tokenization and wholesale CBDC (March 2026)

Digital euro politics (Feb 2026)

🌿 If you’re not a subscriber to the premium daily Crypto is Macro Now, I hope you’ll consider becoming one! You’ll get ~daily commentary on how crypto is impacting the macro landscape, and vice versa - plus links, charts, and some fun stuff because why not. 🌿

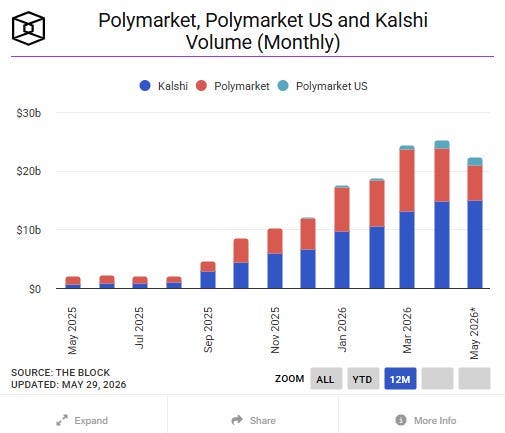

What prediction markets and crypto have in common

Regular readers will have noticed that I hardly ever talk about prediction markets, other than to share the occasional chart. In fact, I don’t think I’ve ever written about them as a concept, and given the firehose of headlines, it’s time to 1) explain why and 2) change that.

The main reason I’ve been ignoring them is that there’s not much that is “crypto” about them. Blockchain has not been their interesting feature. Kalshi doesn’t even really use it (there are now tokenized versions of its markets on Solana, but they are not core to its model). Polymarket does – its engine operates via smart contracts on Polygon, bets are placed in USDC – but that is rarely mentioned as a key operational advantage. While Kalshi and Polymarket run on different systems, they are usually lumped together in the term “prediction markets” with the blockchain part hardly ever mentioned – because, it turns out, for now most users don’t care.

(chart via The Block Data)

Both platforms have strong volumes, with Polymarket dominating the international markets while Kalshi wins overall in the US – Polymarket has only recently been allowed to resume operations there after a 2022 CFTC settlement pushed its operations offshore.

But the relative volumes of each are not the point here. What is more interesting is why prediction markets feature regularly in crypto media and in crypto sections of mainstream media. Why are they considered “crypto”?

There are two threads to pull on:

1) Prediction markets “feel” crypto because they are mainly speculation. And, for mainstream media, crypto is about speculation. So, intuitively, it feels right that even offchain betting platforms be considered a crypto platform.

2) Plus, we’re still trying to figure out what prediction markets are. This is something that those of us attempting to explain crypto to traditional finance are well familiar with (what kind of an asset is BTC? no simple answer), and so for this reason it feels like prediction markets belong over here in the crypto space where the clash of innovation with markets is forcing a reassessment of long-standing definitions.

This is worth pulling on a bit more, as it explains many of the prediction market headlines we’ve seen over the past few months.

A battle is currently waging in the US between states and the federal government on who gets to regulate prediction markets: roughly 16 states are involved in legal proceedings against Kalshi and/or Polymarket, and the CFTC has sued six of them to block their enforcement actions.

Here it very much matters what prediction markets are.

The US founding fathers felt that states should have the right to influence public behaviour and morals within their territory, so anything to do with gambling is regulated at the state level. When you bet yes/no on whether the Knicks will win the playoffs, it can be argued you are gambling. So, sports and other event contracts are supposed to fall under state oversight, and many states don’t approve.

Derivatives, on the other hand are regulated by the CFTC at the federal level – after all, capital markets need to be equal and accessible for all Americans. And event contracts can be used as a capital markets tool. When you bet on whether it will rain in Idaho next week, you could be gambling or you could be hedging your wheat crop. My wager on who wins the Chilean election could be a coin toss, or a hedge against a negative impact on my investment in certain Andean electric utilities. And no-one can say with a straight face today that there is no “gambling” in stock and derivative markets.

Who’s right? Are prediction markets gambling, or are they part of capital markets?

It gets even more complicated when you throw in some moralizing overreach. In 2023, the previous CFTC blocked Kalshi’s political contracts for two cited reasons: they are “gaming” which is contrary to some state laws, and they are “contrary to the public interest” – election bets were seen as a conduit to political manipulation, and would “reduce key facets of the democratic process to a source of revenue for some, fascination and entertainment for others, and, critically, an unmandated duty for the CFTC.” Kalshi sued the CFTC, won, but the CFTC appealed and proposed a ban on sports and political contracts (although this was never finalized and was formally closed this past February). Does the CFTC have the right to decide what is good for American morals?

Plus, it can be argued that use of prediction platforms should be considered an exercise of free speech, and participation in electoral contracts a form of political expression. If I firmly believe that Dwayne Johnson should be the next Speaker of the House, I can charge people an event fee to hear my eloquent argument, but some states want to block me from expressing my view on a public betting platform. I know, this is a bit of a stretch, and commercial speech is not the same as political speech – but it highlights how blurry the definitional boundaries are becoming.

The battle is not limited to the US. Just this week, Indonesia and Spain banned prediction markets. (I can confirm, when I try and access either Kalshi or Polymarket outside my VPN, I get a “This site can’t be reached” page). In both cases, the official reason was they were unlicensed gambling platforms. It’s quite possibly pure coincidence that in each case the bans came shortly after contracts betting on premature ends to the terms of the two countries’ leaders started getting more attention.

Like crypto, prediction markets are forcing a rethink of how we understand markets. It’s not just what an event contract is – a derivative? a random bet? a personal expression? It’s also that regulation still runs on the assumption of hard definitions: before we can figure out how to create a legal framework for something, we need to decide what it is so we know which regulator will be in charge. Crypto has taken so long to crawl through the halls of power because there is still open debate about whether onchain assets are gambling, equity, utility tokens like laundromat coins, or an anti-system political expression. Awareness seems to finally be sinking in that the answer is either “it depends” or “all of the above”. The evolving framework in the US is doing its best to take that into account.

Prediction markets are heading into that rarefied territory also. The courts in the various legal cases will no doubt produce a range of outcomes – such is the nature of the system. The issue could even end up at the Supreme Court, but hopefully before then there will be a greater understanding that prediction markets represent a lot of different concepts rolled into one, and that rather than trying to fit them into existing buckets, new buckets are needed.

Bottom line, technically prediction markets have little to do with “crypto” – but, spiritually, we are kin. And together, we can bring enough consumer demand to convince regulators that the old buckets need flattening, and that new regulation is needed for a new generation of marketplaces.

✨ If you find this newsletter interesting, or even if you just like my excellent taste in music and gifs, would you mind sharing it with friends and colleagues, and nudging them to subscribe? I’d appreciate it! ✨

ASSORTED LINKS

(A selection of reads I came across this week that I think are worth sharing, not about crypto nor macro. I try to choose links without a paywall, but when I feel it’s worth making an exception, I specify.)

Kyla Scanlon distils the simmering concern over the impact of AI on jobs into a deeper understanding of what a job even IS, what we are optimising for, why we get that wrong – an easy yet also deep read that will change how you understand the coming employment problem. (Is AI Going to Destroy Our Lives or Not?, Kyla’s Newsletter)

John Lanchester writes about the massive business of money laundering and the “theatre” of measures to fight it – measures that are not only ineffective, they are destructive and repressive. (Squillions, London Review of Books)

Jon Haidt spoke to the graduating NYU Class of 2026 about how to navigate adulthood amidst an empty clamour for our attention. Recovering some agency in our focus, he argues, is not just possible, it’s essential for a full life. (Treasure Your Attention, After Babel)

“Because what you pay attention to shapes what you care about. And what you care about shapes who you become.”

A fascinating report from the Financial Times on maritime chokepoints, their impact, security and alternatives – a lot of detail and cool graphics including an interactive one that shows which countries rely on which chokepoints. (The power struggle in the world’s narrow seas, Financial Times – paywall)

Fans of heavy metal music will enjoy this interactive map of different variations of the genre. (Map of Metal)

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

If you haven’t seen Project Hail Mary, well, what are you waiting for? This is one of my favourite scenes of the film, and one of the most controversial – it’s not in the book, which has upset purists like my daughter. But I think it adds to the story by encapsulating a moment that could not be conveyed in print.

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.